在觀察了TD過去20十年的價格波動之後,我想用同樣的方法來觀察美股市場中的藍籌股PH,PH和TD是不同國家市場中的股票,從事的行業也是完全不同,沒有任何相關。

參考過去20年的股價波動,在每年的價格底部區域買入,持有二年到價格頂部區域時,

2000 77%

2001 52%

2002 127%

2003 113%

2004 70%

2005 129%

2006 101%

2007 18%

2008 179%

2009 259%

2010 71%

2011 119%

2012 89%

2013 54%

2014 45%

2015 115%

2016 156%

2017 ?

2000-2016年的均值是 104.35%,加二年分紅和紅利再投入大約是4-5%,綜合回報均值是108%左右。

2017年的最低價格是140 x (1+2010-2016年的均值92.71%)= 92.07,2019的最高價可能會是269,目前的價格是170。

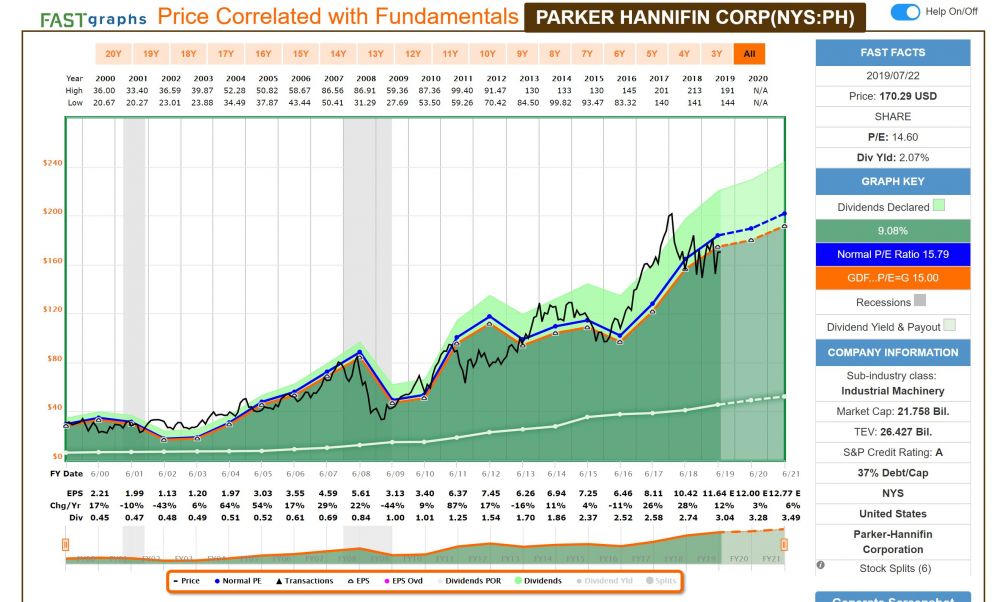

目前PH估值水平明顯低於五年均值,所以下半年如果能回到均值水平,價格升幅會很大。

PH的長期投資回報率大致和TD相當,但是價格波動幅度要大得多。

巴菲特曾經說過如果自己管理小金額資金,可以做到一年50%的投資回報,從PH的價格波動,可以看到市場確實存在這樣的機會。

2011年,老巴印度之行的談話

“If you look at the typical stock on the New York Stock Exchange, its high will be, perhaps, for the last 12 months will be 150 percent of its low so they’re bobbing all over the place. All you have to do is sit there and wait until something is really attractive that you understand.”

“There’s almost nothing where the game is stacked more in your favor like the stock market”

“What happens is people start listening to everybody talk on television or whatever it may be or read the paper, and they take what is a fundamental advantage and turn it into a disadvantage. There’s no easier game than stocks. You have to be sure you don’t play it too often”

但是大幅度的價格波動除了帶來機會以外,也帶來了另一個問題,

The very liquidity of stock markets causes people to focus on price action. If you buy an apartment house, if you buy a farm, if you buy a McDonald's franchise you don't think about what it's going sell for tomorrow or next week, or next month, you think about how is this business going to do. But stocks with this huge liquidity suck people in and they turn what should be an advantage into a disadvantage." - 芒格

從實戰結果看,少數人會像巴菲特說的那樣從股市波動中獲益,

“There is almost nothing where the game is stacked more in your favor like the stock market”

大多數人會像芒格說的那樣,

But stocks with this huge liquidity suck people in and they turn what should be an advantage into a disadvantage.

談談美股Parker-Hannifin Corporation (PH)

(2019-01-06 09:31:28)

目前美國市場長期優秀藍籌股市場估值性價比較高的股票有一大把,Parker-Hannifin Corporation (PH)是其中之一。

之所以想談談PH,因為幾年以前就多次談論過,而且有一位大千的網友在我的建議下寫過一篇完整的投資分析,我曾經多次轉貼過該篇投資分析。因為這是我們大千的網友寫的,所以我們有一個更好的理由來探討。

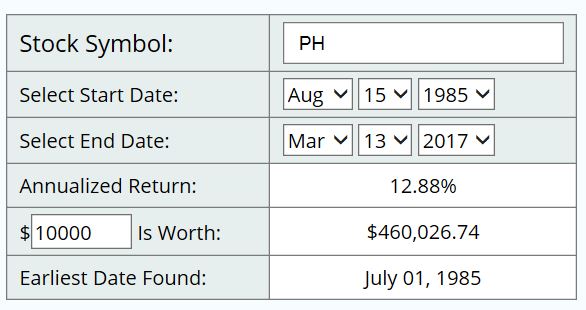

首先,過去5年,10年,20年,30年投資PH,都可以取得非常好的投資回報。參考老朽開始投資房產的時間,10萬本金到今天大約是250萬,要是每次金融危機時加一倍金融杠杆,現在也可以有1000萬,理論上這個機會是存在的,在市場低迷時使用一倍金融杠杆的風險要小於出租房平均財務杠杆的風險。

Monday, April 6, 2015

大千網友的投資分析文章是寫在2015年4月6號,在之後的2016年1月市場波動中(石油價格波動),PH與整體市場都出現了一個投資機會,在市場上漲過程中,PH的漲幅超過了100%,即使是到今天也有70%的漲幅。

目前PH的估值比長期均值水平低許多,已經顯示了相當不錯的性價比,在未來的市場波動中,很有可能再次出現入2016年1月這樣級別的投資機會。

2011年,老巴印度之行的談話

“If you look at the typical stock on the New York Stock Exchange, its high will be, perhaps, for the last 12 months will be 150 percent of its low so they’re bobbing all over the place. All you have to do is sit there and wait until something is really attractive that you understand.”

“There’s almost nothing where the game is stacked more in your favor like the stock market”

“What happens is people start listening to everybody talk on television or whatever it may be or read the paper, and they take what is a fundamental advantage and turn it into a disadvantage. There’s no easier game than stocks. You have to be sure you don’t play it too often”

在大千網友發表PH的投資文章之後,這是第2次市場出現投資機會,所以平均是1.5年一次重大投資機會,如果查看過去20年的股價波動,可以看出平均每二年有一次重大機會。房地產投資能夠每二年出現一次重大投資機會嗎?(至少50%的漲幅。),在今後二十年裏,大致依然是每2年一次重大投資機會,房地產的投資機會能夠達到相同的頻率嗎?PH有未來20年上漲10-20倍的潛質,房價從今天的價格上漲10-20倍的可能性有多大。

“There’s almost nothing where the game is stacked more in your favor like the stock market”

在現實中,有許多人更適合做房地產投資,但是一個合格的股市投資者是沒有任何理由去羨慕出租房生意的。

我要再強調一次,有許多人更適合做房地產投資,這是客觀事實,不要浪費精力探究股市房產哪個更好,對個人而言,最適合的隻有一個。

PH在過去二十年出現了多次的好的投資機會,在今後二十年也將出現多次的投資機會,但是我們隻可能在實戰中把握其中的2,3機會,但是已經足夠了,這是查理芒格的投資經驗總結。

It's not given to human beings to have such talent that they can just know everything about everything all the time. But it is given to human beings who work hard at it ? who look and sift the world for a mispriced be that they can occasionally find one. And the wise ones bet heavily when the world offers them that opportunity. They bet big when they have the odds. And the rest of the time, they don't. It's just that simple.

That is a very simple concept. And to me it's obviously right based on experience not only from the pari-mutuel system, but everywhere else. And yet, in investment management, practically nobody operates that way. We operate that way ? I'm talking about Buffett and Munger. And we're not alone in the world. But a huge majority of people have some other crazy construct in their heads And instead of waiting for a near cinch and loading up, they apparently ascribe to the theory that if they work a little harder or hire more business school students, they'll come to know everything about everything all the time. To me, that's totally insane.

The way to win is to work, work, work, work and hope to have a few insights.

How many insights do you need? Well, I'd argue: that you don't need many in a lifetime. If you look at Berkshire Hathaway and all of its accumulated billions, the top ten insights account for most of it. And that's with a very brilliant man Warren's a lot more able than I am and very disciplined devoting his lifetime to it. I don't mean to say that he's only had ten insights. I'm just saying, that most of the money came from ten insights. So you can get very remarkable investment results if you think more like a winning pari-mutuel player. Just think of it as a heavy odds against game full of craziness with an occasional mispriced something or other. And you're probably not going to be smart enough to find thousands in a lifetime. And when you get a few, you really load up. It's just that simple.

這裏我使用了投資TD銀行一樣的投資思想和策略,所以我投資加國市場可以成功,如果我投資美國市場也可以用同樣的方法取得同樣的成功,就是到了A股市場,也是一樣的結果。

因為“There’s almost nothing where the game is stacked more in your favor like the stock market”

Parker-Hannifin Corporation是美國的著名長期紅利藍籌股,從1985年至今,年均回報是12.88%。如果隻是單獨的看12.88%的回報,是非常普通的,大約是每個月1%, 這比起不少人一天或幾分鍾的百分之幾十的回報,實在是微不足道,但是一個普通的投資者如果能有機會堅持長期的投資於這樣一個投資回報微不足道的股票,卻可以得到非常理想的結果,這裏就體現了複利在長期投資中的威力。老巴的長期投資成績是年均20%多一些,這個成績已經可以使他問鼎世界首富了。

像PH這樣成功的長期紅利藍籌股在美國市場是很多。

這裏的網友bigcatwx曾經在二年前在我的提議寫過一篇關於PH的分析文章,當時他提出的投資價位是105-110之間。

Monday, April 6, 2015

http://moneyunbinding.blogspot.ca/2015/04/stock-analysis-parker-hannifin.html