風蕭蕭_Frank

以文會友

雪上加霜:加拿大生產力放緩,人人有責

https://economics.td.com/ca-productivity-bad-to-worse

Beata Caranci,高級副總裁兼首席經濟學家 | 416-982-8067

James Marple,助理副總裁兼高級經濟學家 | 416-982-2557

2024年9月12日

要點

如果加拿大不努力提高勞動生產率,就可能麵臨生活水平持續下降、工資停滯加劇以及公共服務嚴重惡化的風險。

自疫情爆發以來,大多數行業的勞動生產率都出現了顯著下降。

商品生產部門占了絕大部分。令人惋惜的是,該部門過去十年的生產力優異表現如今卻因自2019年以來平均每年下降1.2%而黯然失色。為了生產出相同水平的產出,商品生產部門需要更多的工人。

在各行業中,建築業表現最差,勞動生產率接近30年來的最低水平。

如果不能加大創新力度並進行行業重組,建築業日益增長的影響力將使加拿大在與其他國家競爭中處於劣勢。

加拿大的服務業增速也有所放緩,但程度較輕。與美國相比,大多數主要行業都嚴重落後。

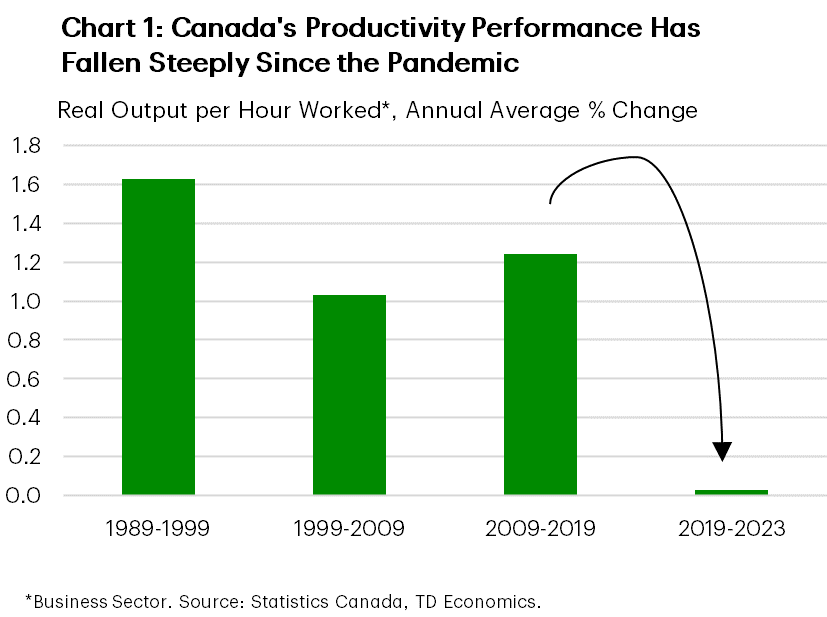

圖1是一張柱狀圖,顯示了加拿大在四個時間段(1989年至1999年、1999年至2009年、2009年至2019年以及2019年至2023年)內每小時實際產出(勞動生產率)的年均增長率。1989年至1999年這十年間,加拿大的勞動生產率年均增長率為1.6%;1999年至2009年為1.0%;2009年至2019年為1.2%。自疫情爆發以來的四年間,增長率已降至0.0%,圖中快速下降的箭頭突顯了這一事實。

一提到“生產率”,人們往往會聯想到用更少的人完成更多的工作這種負麵形象。對於政策製定者來說,要讓加拿大人對這個概念產生熱情並非易事,更不用說讓他們為了解決問題而做出必要的財政犧牲和政策調整了。然而,生產力的健康增長是構建充滿活力、繁榮昌盛且具有韌性的社會的關鍵。生產力的提升能夠推動實際工資增長,並且對於維持高質量的公共服務至關重要。

因此,自疫情爆發以來,加拿大經濟表現的顯著惡化應該引起所有加拿大人,尤其是年輕一代的嚴重關切。以人均實際GDP衡量,加拿大2023年的生活水平低於2014年。如果生產力增長停滯不前,工人的工資將無法增長,政府收入也將無法滿足支出需求,這將迫使政府提高稅收或削減公共服務。

那麽,加拿大究竟出了什麽問題?

在疫情爆發前的十年裏,加拿大商業部門的生產力以每年1.2%的可觀速度增長(圖表1)。但自2019年以來,生產力增長已完全停止,這使得加拿大成為發達經濟體中表現最差的經濟體之一,更不用說與美國形成了鮮明對比(參見之前的報告)。

我們多麽希望能夠告訴大家,隻有少數幾個行業是罪魁禍首。然而,問題卻十分普遍。與疫情前十年的增長相比,隻有少數服務業的業績有所改善。商品行業的從業者受到的影響最大,自疫情爆發以來,他們的生產率出現了倒退。這意味著什麽?如今,要獲得同樣的產出,工人需要投入更多的時間。這在數字化時代簡直難以置信。

在加拿大,有一個行業比其他行業更顯突出:建築業。由於其在經濟中的占比不斷擴大,生產率的下降已成為整體經濟疲軟的重要根源。

在服務業中,大多數行業自疫情爆發以來生產率都有所下降,但程度不及建築業嚴重。盡管如此,與美國相比,關鍵服務業仍然存在顯著差異。

由於生產率低下問題已十分普遍,因此沒有靈丹妙藥可以解決加拿大的生產力困境。人們常說的解決方案看似直觀,但對加拿大而言卻難以實現:促進競爭、留住技術工人、減少貿易和投資壁壘(包括國內和國際壁壘),以及改善技術采納的激勵機製。這是避免加拿大淪為七國集團(G7)“窮親戚”的最低要求。

然而,重點需要放在建築業,尤其是住宅建築。該行業主要由小型企業組成,而這些企業采用新技術的速度較慢。建築業的生產力一直最弱,而該行業小型企業占比最高。針對增長瓶頸製定有針對性的策略可能大有裨益。協調各省的建築規範和許可要求有助於增強競爭,同時提高整個行業的規模效益。

對於服務業而言,對非永久居民的過度依賴似乎導致了產品價格的下跌。

自疫情爆發以來,生產力持續下降。這在勞動力老齡化的大背景下似乎有悖常理,但大量非永久居民集中在低收入工作崗位上,確實加劇了加拿大生產力的下滑。<sup>1</sup> 提高服務業生產力增長需要支持性的稅收和監管政策,以鼓勵更多投資並加速技術應用。

自疫情爆發以來,商品行業的生產力有所下降。

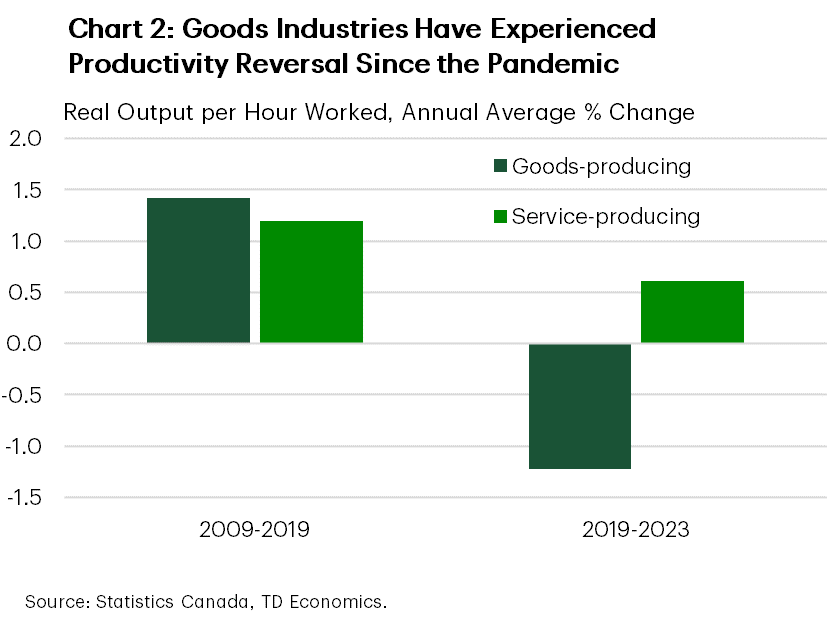

圖2為柱狀圖,顯示了商品生產和服務生產部門在兩個時間段(2009-2019年和2019-2023年)內每小時實際產出(勞動生產率)的年均增長率。在疫情爆發前的十年(2009-2019年),商品生產行業的年均勞動生產率為1.4%,但在疫情爆發後的十年(2019-2023年)下降了1.2%。服務生產行業的年均勞動生產率增長率也從疫情爆發前的十年的1.2%放緩至疫情爆發後的0.6%。

加拿大的經濟主要以服務業為主。這並非什麽新鮮事,而是穩步發展的趨勢。但另一方麵,過去二十年間,商品部門(包括農業、公用事業、製造業和建築業)的總活動占比已從占加拿大經濟的三分之一下降到四分之一。

然而,就生產率而言,商品部門的表現卻遠超其規模。其勞動生產率比服務業高出30%以上。其中,資本密集型的??采礦業、石油和天然氣開采業以及公用事業部門尤為突出。相比之下,製造業、建築業和農業的生產率則低得多。

不幸的是,自疫情爆發以來,除農業、林業、狩獵和漁業外,商品生產行業的生產率增長不僅放緩,而且出現了倒退(圖表2)。在疫情爆發前的十年裏,這些行業的年均增長率為1.4%,而疫情爆發後,年均增長率卻下降了1.2%。

因此,自疫情爆發以來,商品部門每年平均拖累加拿大整體生產率增長0.4個百分點。如果該部門保持平穩,加拿大的生產率年增長率本應達到0.5%。盡管這一表現仍遠遜於五年前的水平,但足以超越歐元區。

建築業生產率已持續下降數十年。

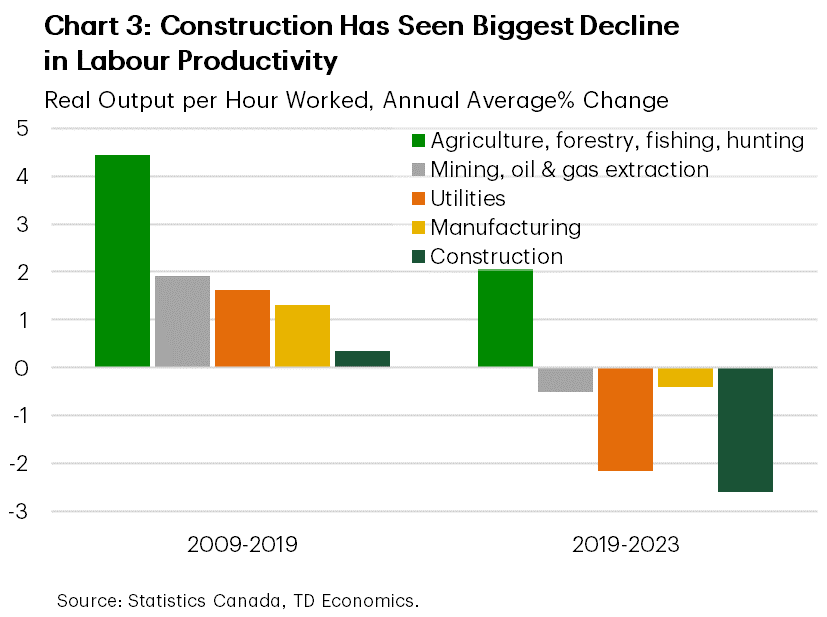

圖表3以柱狀圖的形式展示了五個商品生產部門——農業、林業、漁業和狩獵業、采礦和油氣開采業、公用事業、製造業以及建築業——在兩個時間段(2009-2019年和2019-2023年)內每小時實際產出(勞動生產率)的年均增長率。在疫情爆發前的十年(2009-2019年),農業生產率的年均增長率為4.4%,但此後已放緩至2.1%。在疫情爆發前的十年裏,采礦、石油和天然氣開采業增長了1.9%,但疫情爆發後的幾年裏,該行業每年萎縮0.5%。公用事業在疫情爆發前的十年裏增長了1.6%,但疫情爆發後的幾年裏,該行業每年萎縮2.2%。製造業在疫情爆發前的十年裏增長了1.3%,但疫情爆發後的幾年裏,該行業每年萎縮0.4%。最後,建築業在疫情爆發前的十年裏僅增長了0.4%,但疫情爆發後的幾年裏,該行業每年萎縮2.6%。

圖表3詳細分析了這個問題。自疫情爆發以來,公用事業部門經曆了顯著惡化,但這並非主要擔憂領域,因為其主要原因是創紀錄的高溫導致2023年水力發電量下降。<sup>2</sup>

令人擔憂的行業首先是采礦和油氣開采,這兩個行業在疫情爆發前的十年中生產率穩步增長,但此後每年下降0.5%。盡管衡量該行業的生產率頗具挑戰性(見下方文本框),但加拿大的情況也存在一些獨特之處。該行業的投資下降部分原因是關鍵基礎設施項目(例如Keystone XL輸油管道)被取消,部分原因是碳定價和能源轉型導致投資減少。<sup>3</sup> 雖然能源轉型是必要的,但脫碳可能會進一步抑製該行業的投資。鑒於該行業相對較高的勞動生產率,這無疑將在未來幾年給加拿大帶來生產率方麵的挑戰。

製造業相對於疫情前的平均水平而言,降幅最小,但該行業的生產率也經曆了由增長轉為下降的轉變,尤其是在過去一年中出現了急劇下降。此外,建築業的生產力在所有商品行業中墊底。這種長期存在的趨勢愈演愈烈,由於其在經濟活動中占比不斷上升,給加拿大帶來了更大的痛??苦。

建築業的生產力在過去一段時間裏沒有實現任何增長。

From Bad to Worse: Canada's Productivity Slowdown is Everyone's Problem

https://economics.td.com/ca-productivity-bad-to-worse

Beata Caranci, SVP & Chief Economist | 416-982-8067

James Marple, AVP & Senior Economist | 416-982-2557

September 12, 2024

Highlights

- If Canada does not play to win on labour productivity, it risks a continued drop in living standards, worsening wage stagnation and a dangerous deterioration in public services.

- The pronounced downshift in labour productivity since the pandemic has manifested in most industries.

- The goods-producing sector accounts for the lion’s share. In a turn of fortune, a decade-long outperformance in productivity is now marred by a 1.2% average annual decline since 2019. More goods sector workers are required just to produce the same level of output.

- Among industries, construction is the worst of the lot with labour productivity at a near 30-year low.

- Construction’s deepening presence will keep Canada on its backfoot relative to peers in the absence of greater innovation adoption and a reshaping of the industry.

- Canada’s service sector has also slowed, but to a lesser degree. Compared to the U.S., most major industries severely lag.

Hearing the word, productivity, often brings to mind a negative image of accomplishing more work with less people. It’s a hard sell for policymakers to get Canadians fired up on the concept, let alone to make the necessary financial sacrifices and policy adjustments toward solutions. Yet, healthy growth in productivity is key to a dynamic, prosperous, and resilient society. Productivity improvements drive real wage growth and are essential to maintaining quality public services.

So the fact that Canada’s performance has deteriorated so materially since the pandemic should be of grave concern to all Canadians, particularly younger generations. Canadian’s standard of living, as measured by real GDP per person, was lower in 2023 than in 2014. Without improved productivity growth, workers will face stagnating wages and government revenues will not keep pace with spending commitments, requiring higher taxes or reduced public services.

So what ails Canada?

Over the decade prior to the pandemic, business sector productivity grew by a respectable rate of 1.2% annually (Chart 1). Since 2019, it has ceased to expand at all, setting Canada apart as one of the worst performing advanced economies, not to mention in stark contrast to the United States (see earlier report).

We wish we could tell you that only a single or handful of industries are the culprit. However, the woes are widespread. Relative to growth in the decade prior the pandemic, only a few service industries have managed to improve their performance. Those working in the goods sectors have felt the downshift the most, where productivity has gone in reverse in the years since the pandemic. What does that mean? To get the same output, it now requires more hours from workers. Hard to believe this could occur in a digital age.

There is one sector in Canada that wears the Scarlet Letter more prominently than the others: construction. Due to its increasing size within the economy, its declining productivity has been an increasingly important source of overall weakness.

Among service-producing industries, most have experienced a productivity slowdown since the pandemic, but not as severe. Still, when compared to the U.S., stark differences occur in key service industries.

There is no silver bullet to fixing Canada’s productivity woes because the underperformance has become so pervasive. The often-cited solutions are intuitive but elusive for Canada: fostering competition, retaining skilled workers, reducing barriers to trade and investment (both internally and externally), and improving incentives for technology adoption. This is the minimum needed to keep Canadians from being the poor cousins of the G7.

However, a focus needs to be on the construction sector, especially residential building. It is composed mainly of small firms, which are slower to adopt new technologies. Productivity has been weakest in building construction, which has the largest share of small firms. Targeted strategies to address constraints to growth could be beneficial. Harmonizing building codes and licensing requirements across provinces could help increase competition while allowing for greater returns to scale across the industry.

For service industries, greater reliance on non-permanent residents appears to have contributed to the productivity deterioration since the pandemic. This may seem counterintuitive amidst an aging labour force, but the concentration of non-permanent residents in low paid work has worsened Canada’s productivity performance.1 Raising productivity growth in services will require supportive tax and regulatory policy that encourage greater investment and accelerate technology adoption.

Goods sector productivity has contracted since the pandemic

Canada’s economy is primarily one of services. This is not a new development, but one that is steadily marching forward. The flip side of that coin is that over the past two decades, the combined activity of goods sectors — agriculture, utilities, manufacturing, and construction — has fallen from one-third to a quarter of the Canadian economy.

In terms of productivity, however, the goods sector punches above its weight. Labour productivity is over 30% higher than in the service sector. Bragging rights go to the relatively capital intensive mining, oil and gas extraction, and utilities sectors. Manufacturing, construction and agriculture have much lower levels of productivity by comparison.

Unfortunately, since the pandemic, with the exception of agriculture, forestry, hunting and fishing, productivity growth within goods-producing industries has not only slowed but has outright reversed (Chart 2). From an annual increase of 1.4% in the decade prior to the pandemic, it has declined by 1.2% annually since.

As a result, the goods sector has subtracted an average of 0.4 percentage points from Canada’s overall productivity growth every year since the pandemic. Had the sector just stayed flat, Canada’s pace would have risen 0.5% annually. Although this performance still pales to that of five years prior, it would have been sufficient to outpace the Euro Area.

Construction productivity has been in decline for decades

Chart 3 breaks down the problem. The utilities sector experienced a signficant deterioration since the pandemic, but this is not a primary area of concern as it was largely due to record-high temperatures that led to a decline in the production of hydroelectricity in 2023.2

The sectors of concern start with mining and oil and gas extraction, which experienced healthy productivity gains in the decade prior to the pandemic but has since fallen 0.5% annually. While measuring productivity in the sector is challenging (see text box below), there are some attributes unique to Canada. Investment in the sector has fallen in part as key infrastructure such as the Keystone XL pipeline was cancelled, but also as a result of reduced investment in the wake of carbon pricing and the energy transition.3 Although this is a necessary transition, decarbonization is likely to further weigh on investment in the sector. Given its relatively high level of labour productivity, this automatically presents a productivity challenge for Canada over the next several years.

Manufacturing is experiencing the smallest decline relative to its pre-pandemic average, but here too productivity has swung from gains to losses, with a particularly sharp drop over the past year.

And then there’s the construction sector, which has experienced the worst productivity of any goods sector. This is a longstanding pattern that has worsened, injecting more pain into Canada due to its rising share of economic activity.

Construction has generated no productivity growth over the past forty years! It’s not a uniquely Canadian problem, but rather global in nature. For instance, U.S. productivity growth in construction has been worse relative to Canada over the last 30 years and only slightly better since the pandemic. Studies in the U.S. have shown resources moving from higher productivity regions to lower – the opposite of allocative efficiency. The decline in productivity has coincided with an increase in land-use regulations, suggesting that non-economic factors have played a central role.4,5

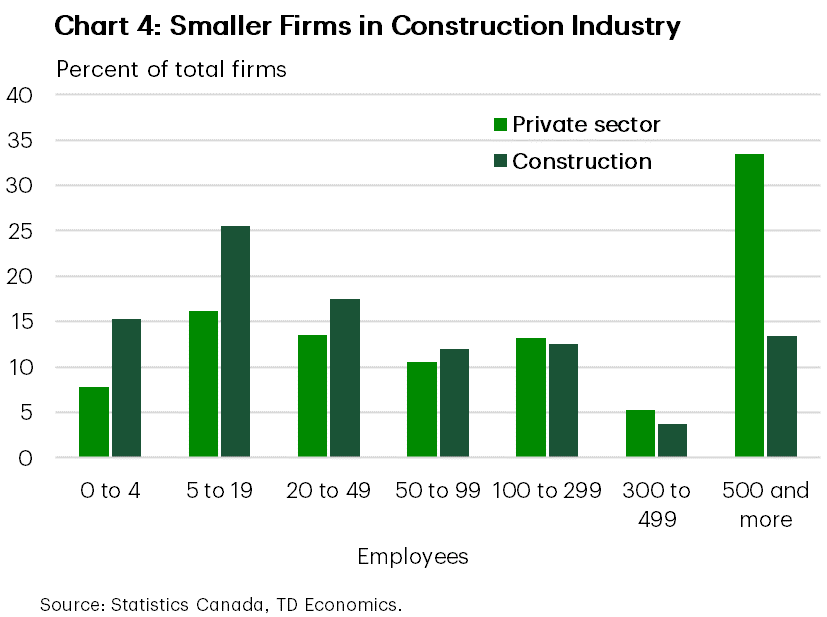

The same appears to be true in Canada. For example, as documented by CMHC, there are considerable differences in residential construction productivity across the country, suggesting that differences in regulations and permitting play a role in productivity performance.6 More than other sectors, construction is characterized by very small firms – 40% have fewer than 20 employees (Chart 4). Smaller firms have been shown to have lower levels of productivity and are slower to adopt new technologies than larger firms.7 They also face larger regulatory burdens relative to their size than larger businesses, which materially weighs on productivity.8 There are a number of ‘low-hanging fruit’ barriers to growth in construction such as building codes, permitting and licensing requirements that differ across provinces and make it difficult for firms to operate across jurisdictions. A lack of standardization is another challenge that makes innovation harder to scale up across the industry.

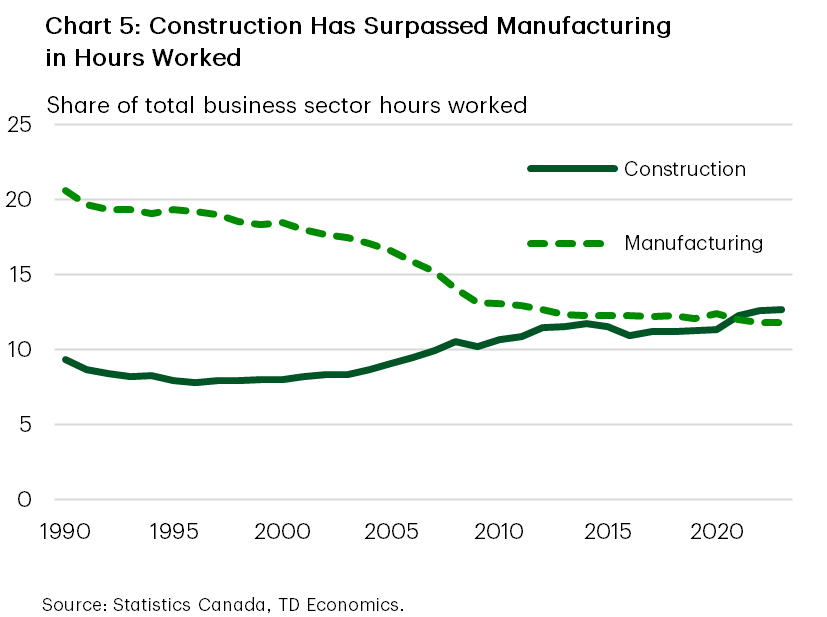

Construction is growing in importance

Unfortunately, the poor performance of the construction sector is an increasingly important driver of Canada’s overall productivity story because it is growing as a share of the economy more than other countries (Chart 5). In 2023, the construction sector represented 12.6% of all labour hours worked in Canada, up from 8% in 1997. Isolating to just the goods-producing sector, construction hours worked now exceed those in manufacturing, nearly doubling from 23% in 1997 to 42% of today.

Now consider the increasing shift of resources into construction activity rather than other areas, and the impact on total Canadian productivity intensifies. Adding this “reallocation effect” to the “within-sector effect” described above reveals a construction sector that has subtracted 0.5 percentage points from annual productivity growth since the pandemic. It has accounted for the vast majority of the decline in overall Canadian productivity relative to the pre-pandemic period.

And the problem deepens when we cast an eye forward. Construction is unlikely to become less important over the next five years, or more. Canada suffers from a housing deficit, suggesting a need for more resources to be sucked into the sector. The Bank of Canada’s recent Monetary Policy Report reduced their forecast for overall Canadian productivity over the next two years citing “constraints on housing construction coming from structural factors, such as the availability of land, zoning restrictions and a lack of skilled labour.”9

The rising importance of construction increases the urgency to improve productivity in the sector. But this requires more outside-the-box thinking, including moving to more prefabricated or modular building, developing a reskilled workforce around it, and rethinking the building code to allow for more flexibility in the sources of materials used that maintain the same results in terms of safety and durability. There are examples of this in other countries, such as Sweden, where modular building has a significant presence.10

The Curious Case of Productivity in Canada’s Oil & Gas Sector

Canada’s oil and gas sector has one of the highest productivity levels in the Canadian economy as well as some of the highest wages. Due to the size of its productivity outperformance relative to the rest of the economy, the sector has played an outsized role in driving Canadian productivity. Although the sector has seen labour productivity growth ebb and flow over several decades, it was on an encouraging upswing in the years leading up to the pandemic.11 Nonetheless, a decline in labour hours in the sector weighed materially on aggregate labour productivity growth.

Underneath the surface, things get even more complicated. Labour productivity can be broken down into the amount of capital per worker, the skills of those workers, and the technology that determines how inputs (capital and labour) are turned into outputs (termed multifactor productivity or MFP). In the textbook case, lifting productivity growth is simply a matter of increasing the capital and skills of workers and/or spurring innovation (MFP growth).

But in the real world, the oil and gas sector appears to have a counterintuitive relationship between the amount of capital it adds and growth in innovation. While the sector has consistently increased capital per worker, MFP has generally declined over the past 50 years. How could this be for a sector that has seen a steady stream of innovation from the early-days of steam-assisted gravity drainage in oilsands development to digital oil field technologies recently.

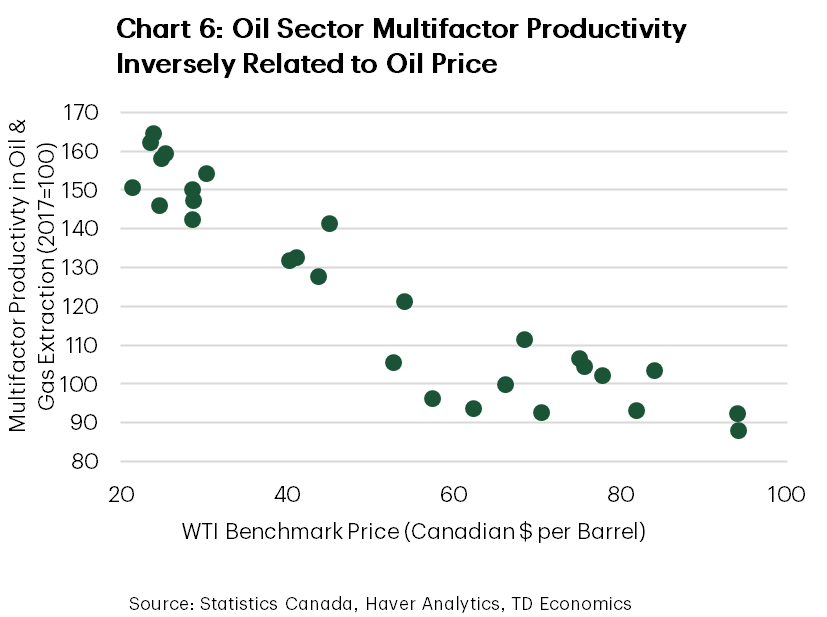

One reason is that the productivity statistics do not account for the price of the non-renewable resource. As oil prices have risen, companies have been induced to invest more into difficult deposits that take more labour and capital to extract. This shows up in an inverse relationship between oil prices and MFP (Chart 6).

A second reason is that productivity statistics do not account for the non-renewable nature of the resource. Even without the price effect, more labour and capital must necessarily be expended as easier geology deposits are exhausted. This contributes to the statistical underestimation of MFP growth.12

Finally, the sector must increasingly contend with the necessity of reducing its carbon footprint. This requires both investment and innovation – carbon capture and storage as an example – that does not necessarily raise output in the sector.

All of this suggests caution in interpreting weak MFP in the oil and gas sector and its negative effects on Canadian productivity growth. Labour productivity should be the focus.

A select few service industries have seen faster productivity growth since pandemic

It’s not all downbeat news. A few sectors stand out with improved productivity growth since the pandemic. Among them are wholesale and retail trade, information and cultural industries, accommodation and food services, and real estate, rental, and leasing. Many of these industries were hit hardest by the pandemic with greater employment disruptions, reinforcing the belief that productivity growth is about fewer people. As of 2023, hours worked in retail trade and real estate, rental and leasing was still lower than in 2019.

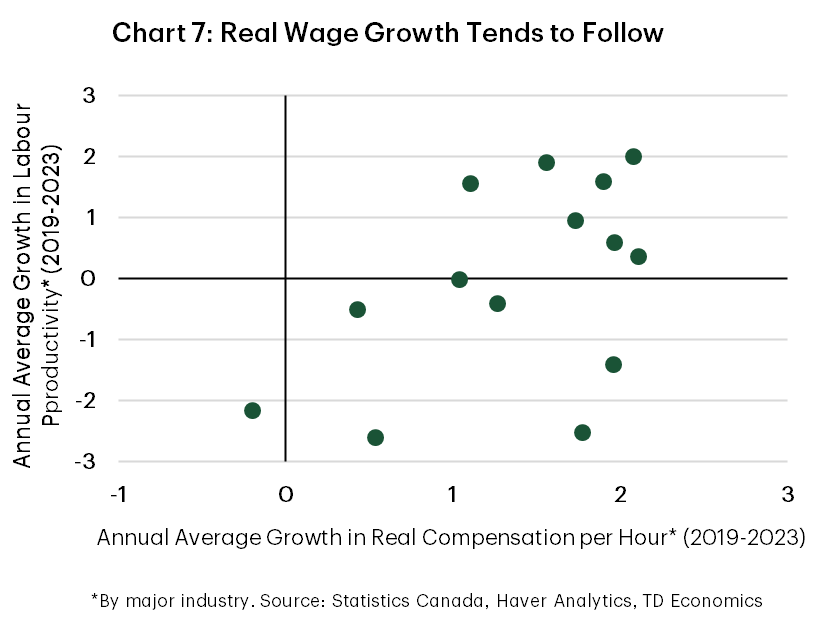

However, as in the past, gains from productivity are showing up in rising compensation for these workers. Since the pandemic, real (inflation adjusted) compensation per hour has grown faster in sectors with greater productivity growth. Service industries have experienced annual average growth in real compensation of 1.8% compared to 1.0% in goods sectors. The strongest productivity sectors have seen the strongest wage growth (Chart 7). Information and cultural industries have experienced real wage growth of 2.1% annually and accommodation and food services are not far behind at 2%.13

It is too early to say whether the pandemic shock has caused more permanent changes to these industries. Some of the productivity improvement may reflect trends in automation and digitization since the pandemic. This offers hope that as digital technologies and artificial intelligence (AI) are more widely adopted, productivity growth could accelerate. As we have argued (see report), Canada has a significant share of high-skilled occupations that could benefit from considerable improvements in productivity through AI.

Canada lags the U.S. across most industries, especially services

And this is where the big push must ultimately come from. Canada has lagged U.S. productivity growth for the past several decades, but the deterioration has worsened since the pandemic. Since then, the U.S. has seen business sector productivity growth of 1.6% annually, while Canada has failed to produce any advancement. From 2019 through 2022 (the latest detailed industry data available for the U.S), the U.S has outperformed Canada across most major industries.

U.S. productivity has been particularly strong within retail trade, information, and cultural industries (including telecommunications), professional, scientific, and technical services, and accommodation and food services. Although many of these same industries have led productivity growth for Canada more recently, they have consistently and significantly lagged the U.S. over the past two decades.

The greatest cross-country wedge has occurred within the professional, scientific, and technical services and accommodation and food services. The U.S. experienced accelerated and robust growth of 3.8% for the former and 3.9% for the latter from 2019 to 2022. By contrast, productivity growth in Canada’s professional services sector slowed from its pre-pandemic average. Productivity growth improved in the retail sector, but to a much smaller degree than in the United States.

Some of the challenges are longstanding. Canada has been a laggard in adopting information and communication technology (ICT) and meaningfully slower growth within this area explains much of the growing U.S.-Canada productivity gap in the two decades prior to the pandemic.

In fact, there’s only one sector that has consistently outperformed its American counterparts over the past decade and through the pandemic: finance, insurance, real estate, rental and leasing (FIRE). In the decade prior to the pandemic, labour productivity in the sector grew by 2.2% annually in Canada compared to 1.0% in the U.S. Since the pandemic, the gap has increased, with growth of 3.2% in Canada and just 0.4% in the United States. Output of the financial sector in the U.S. was impacted to a much higher degree by the Global Financial Crisis, but that does not explain Canada’s more recent outperformance. Some of it may reflect catch up growth, as the U.S. sector exhibits higher levels of labour productivity than Canada. While comparable data on the details between the two countries is only available to 2020, in the five years prior to the pandemic, the sectors in both countries saw similar contribution from investment-driven growth in capital per worker, but Canada’s industry saw relatively faster MFP growth.

An internationally competitive tax system is an important contributor to investment and productivity. Canada made a concerted effort to lower its corporate income taxes in the early 2000s and had lower corporate income tax rates than international peers through the decade that preceded the pandemic. However, this advantage has eroded considerably in recent years as other countries have lowered tax rates. The Tax Cuts and Jobs Act of 2018 for example lowered the U.S. corporate income tax rate by fourteen percentage points from 35% to 21%. Several European countries also reduced their tax rates over this period. With these changes abroad, Canada’s average tax rate is now roughly in line with the U.S. and OECD average, but higher than Europe. A tax rate just in line with the U.S. is probably not sufficient to counteract the country’s inherent strengths in drawing in investment and talent. Canada must aim to do better in order to level the playing field.

The profitability of new investments is also influenced by a host of other measures that interact with the tax system, including interest, depreciation, inventory cost, fees, and other deductions. A measure that includes these factors is the marginal effective tax rate (METR).14 Canada’s METR was temporarily reduced below peers by accelerated depreciation measures in 2019, which allowed investment in manufacturing and processing machinery and equipment to be fully deducted from taxes. The deduction was, however, temporary, and is set to be fully phased out by 2028. As this temporary measure expires, Canada’s METR will rise considerably, raising the cost of new investment and weighing on productivity growth.15

Some might wonder if these tax credits have been effective, considering Canada’s deteriorated investment and productivity backdrop over the last several years. The flip side of the lens is to consider how much worse the investment impulse would be in Canada in their absence. Unwinding it would fly in the face of “do no harm” principle, reducing Canada’s competitiveness during a period when the struggle runs so deep. In addition, measurements like the METR do not include regulations or provisions in the tax code that favour certain industries over others. These have also been shown to impede markets signals, weigh on productivity and reduce competitiveness.16

Bottom Line

Canada has seen its productivity go from bad to worse since the pandemic. Labour productivity was temporarily and artificially lifted by pandemic lockdowns in early 2020 when hours were cut more than overall economic activity. But in the three years since productivity has declined every single year, with the decline worsening in 2023 relative to 2022. An outright decline in productivity in the goods sector explains much of Canada’s moribund productivity growth. While the service sector slowed more modestly, this is nothing to crow about. It stands in sharp contrast to the improved performance stateside.

Addressing Canada’s productivity issues requires comprehensive strategies, including promoting competition, incentivizing technology adoption, reducing barriers to growth across jurisdictions, and implementing smarter regulations. At a minimum, government should focus on doing no harm, maintaining incentives for capital investment. The expiry of the accelerated depreciation allowance (discussed in textbox above) is a move in the wrong direction, raising the cost of new investment. Reforming the tax code more broadly to reduce the cost of new investment should be a policy priority. Focusing on improving productivity in construction sector is particularly urgent due to its growing economic importance. If Canada does not play to win on labour productivity, it risks a continued drop in living standards, worsening wage stagnation and a dangerous deterioration in public services.

End Notes

- Smith, Philip. Accounting for the Decline of Canada’s Real GDP per Capita Since Mid-2022. International Productivity Monitor, Centre for the Study of Living Standards, Spring 2024. Available at: http://www.csls.ca/ipm/46/IPM_46_Smith.pdf

- Statistics Canada. “Hydroelectricity generation dries up amid low precipitation and record high temperatures: Electricity year in review 2023.” March 5, 2024. Available at: https://www.statcan.gc.ca/o1/en/plus/5776-hydroelectricity-generation-dries-amid-low-precipitation-and-record-high-temperatures

- Wang, W., “The Oil and Gas Sector in Canada: A Year After the Start of the Pandemic.” Economic and Social Reports. Vol. 1, no.7. Statistics Canada. July 28, 2021. Available at: https://www150.statcan.gc.ca/n1/pub/36-28-0001/2021007/article/00003-eng.pdf

- Goolsbee Austan and Syverson, Chad., “The Strange and Awful Path of Productivity in the U.S. Construction Sector.” NBER Working Paper 30845, National Bureau of Economic Research, January 2023. Available at: https://www.nber.org/system/files/chapters/c14735/c14735.pdf

- D’Amico, Leonardo and Glaeser, Edward L. and Gyourko, Joseph and Kerr, William R. and Ponzetto, Giacomo A. M., “Why Has Construction Productivity Stagnated? The Role of Land-Use Regulation.” December 30, 2023. Available at: https://ssrn.com/abstract=4679195 or http://dx.doi.org/10.2139/ssrn.4679195

- Laberge, Mathiue. “What is Canada’s Potential Capacity for Housing Construction?” Web log. The Housing Observer (blog) (May 16, 2024). Available at: https://www.cmhc-schl.gc.ca/blog/2024/what-canada-potential-capacity-housing-construction#:~:text=Even%20with%20a%20record%2Dhigh,over%20400%2C000%20homes%20per%20year

- Baldwin, John R, Leung, Danny, and Rispoli, Luke. “Canada-United States Labour Productivity Gap Across Firm Class Sizes.” The Canadian Productivity Review. Catalogue no. 15-206-X, no 0.33. March 10, 2014. Available at: https://www150.statcan.gc.ca/n1/en/pub/15-206-x/15-206-x2014033-eng.pdf?st=WuWeixPT

- Tu, Jiong. “The Impact of Regulatory Compliance Costs on Business Performance.” Innovation, Science and Economic Development Canada. 2020. Available at: https://ised-isde.canada.ca/site/paperwork-burden-reduction-initiative/en/survey-regulatory-compliance-costs/impact-regulatory-compliance-costs-business-performance-october-2020

- Bank of Canada. Monetary Policy Report - July 2024. Bank of Canada, July 24, 2024. Available at: https://www.bankofcanada.ca/wp-content/uploads/2024/07/mpr-2024-07-24.pdf

- Anderson, Christina. “How and American Dream of Housing Became a Reality in Sweden.” New York Times, June 8, 2024. Available at: https://www.nytimes.com/2024/06/08/headway/how-an-american-dream-of-housing-became-a-reality-in-sweden.html

- Due to the size of its productivity outperformance relative to the rest of the economy, movements in resources in and out of the sector can play an outsized role in driving Canadian productivity. In the five years prior to the pandemic one of the key drags on Canada’s productivity was the decline in production and hours in the oil and gas sector.

- Gordon, Stephen. “What Explains the Weak Growth in Total Factor Productivity in Non-Renewable Resource Extraction Industries?” Web log. Worthwhile Canadian Initiative (blog) (June 26, 2024). Available at: https://worthwhile.typepad.com/worthwhile_canadian_initi/2024/06/tfp.html

- Without productivity growth, increases in wages imply a decrease in relative competitiveness. This is a particular challenge for export-facing industries. As a result of poor productivity growth, the cost of labour relative to output has risen faster in Canada than in the United States, making it harder for Canadian companies to compete at the going exchange rate.

- Bazel, Philip and Mintz, Jack. 2020 Tax Competiveness Report: Canada’s Investment and Growth Challenge. The School of Public Policy, University of Calgary, September 2021. Available at: https://www.policyschool.ca/wp-content/uploads/2021/09/FMK2_2020-Tax-Competitiveness_Bazel_Mintz.pdf

- Ibid.

- Farhi, Emmanuel and Baqauee, David. The Impact of Firm Misallocation on Aggregate Productivity: A Quantitative Analysis. Harvard University, 2020. Available at: https://scholar.harvard.edu/files/farhi/files/misallocation_main.pdf