我心悠悠

隨筆

應避免 TLT [大千股壇] -2022-04-11

持有美國國債最保守的方式是持有至到期,保證還本付息,靈活的是它可以在任何時候以市場價格出售,基本上,買債券是把它當作資金庫房,獲得小紅利, 作為跳台,市場時機條件有利於重新做多,賣出債券,買入股票.

每隻債券都有到期日,當10年期債券剩餘到期日僅剩3年時,也視為3年期債券, 每隻債券都有固定的收益率coupon rate, 這個利率是您將獲得的股息金額的計算依據. 它不會改變. 所以您會發現你買了不同的3年期債券,實際股息是不同的,那是因為債券票麵收益率是固定的, 您購買不同的3年期債券,市場價格將進行調整,因此為什麽不同的3年期債券都有大致相同的實際股息率. 每個國債都有一個代碼 CUSIP, 國債是在二級市場買/賣,通常經紀人有一個交易屏幕做這個交易

第一部分

(1) 債券的基本概念

以高於賬麵價值買入的債券叫溢價購買

以低於賬麵價值買入的債券叫貼現購買

(2) 持有至 到期日 (排除收到的定期股息)

票麵價格1000, 財政部將支付 1000.

購買價格 1100, 溢價 100. 資本損失 100

購買價格 900, 貼現 100. 資本利得 100

(3) 在到期日之前賣出 (排除收到的定期股息)

賣出價格扣除購買價格, 交資本利得稅或申報資本損失

- 稅務後果請與您的稅務會計谘詢

- 財政部國債豁免州和地方所得稅。

- 債券溢價產生的資本損失可以扣除資本利得嗎?

- 貼現債券產生的利潤需要支付資本利得稅嗎?

Do Bonds Bought at a Premium Produce Capital Losses?

Taxable bonds do, but municipals don't. We'll walk you through it.

https://www.thestreet.com/story/906504/1/do-bonds-bought-at-a-premium-produce-capital-losses.html

債券 示例

第二部分

購買中期國債(2-3年到期)[**不是債券基金**] - 這是一個話題,需要一些時間來了解, 還沒有成為計劃。 當市場處於下跌趨勢,債券能夠充當臨時存放處與跳板. 現在三年期國債 (Treasury Note)市場利率約為2.69%,.

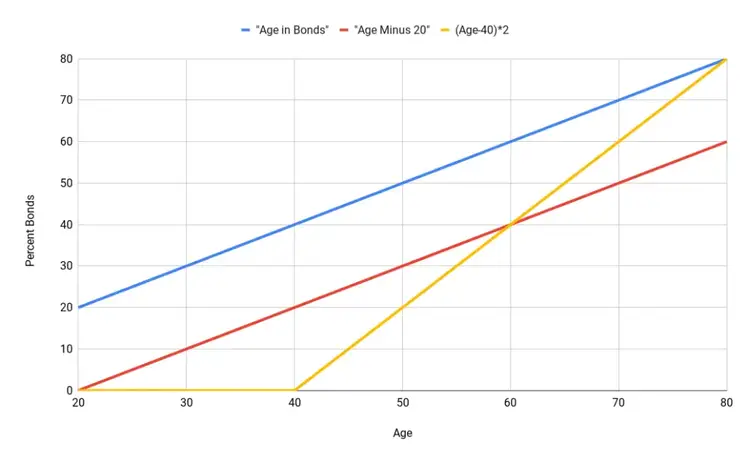

There are several quick, oft-cited model calculations used for dynamic asset allocation of a portfolio of stocks and bonds by age, moving more into bonds as time passes because they’re safer. For the sake of clarity and consistency of discussion, we’re going to assume a retirement age of 60.

- The first and simplest adage is “age in bonds.” A 40-year-old would have 40% in bonds. This may indeed be fitting for an investor with a low tolerance for risk, but is too conservative in my opinion. In fact, this conventional wisdom that has been repeated ad nauseam goes against the recommended asset allocations of all the top target date fund managers. This calculation would mean a beginner investor at 20 years old would already have 20% bonds right out of the gate. This would very likely stifle early growth when accumulation is more important at the beginning of the investing horizon.

- Another general rule of thumb is a more aggressive [age minus 20] for bond allocation. This calculation is much more in line with expert recommendations. This means the 40-year-old has 20% in bonds and the young investor has a portfolio of 100% stocks and no bonds at age 20. This also yields the stalwart 60/40 portfolio for a retiree at age 60.

- A more optimal, albeit slightly more complex formula may be something like [(age-40)*2]. This means bonds don’t show up in the portfolio until age 40, allowing for maximum growth while early accumulation is more important, then accelerating the shift to prioritizing capital preservation nearing retirement age. This calculation seems to most closely follow the glide paths of the top target date funds.

Generally speaking, it could be said that these 3 formulas coincide with low, moderate, and high risk tolerances, respectively.

illustrates the 3 formulas above in the chart below: