笨狼發牢騷

發發牢騷,解解悶,消消愁

上周中國公布本年一季總產值及相關經濟數據,這是中外的報道、評論集。雖然隻是堆積在此,但資料足夠對一季中國經濟有個概況,查起來也集中,瀏覽一下也有價值。

難以覺得大家會有耐心過目,細嚼就更無從談起了,尤其是文學城。

我會在以後說說想法和判斷。

《一財》

【1】一季度GDP增速定格6.7% 統計局稱階段性築底

第一產業增加值8803億元,同比增長2.9%;第二產業增加值59510億元,增長5.8%;第三產業增加值90214億元,增長7.6%

固定資產投資增速穩中有升,一季度,固定資產投資85843億元,同比名義增長10.7%,扣除價格因素實際增長13.8%

全國商品房銷售麵積24299萬平方米,同比增長33.1%,其中住宅銷售麵積增長35.6%

全國商品房銷售額18524億元,同比增長54.1%,其中住宅銷售額增長60.3%

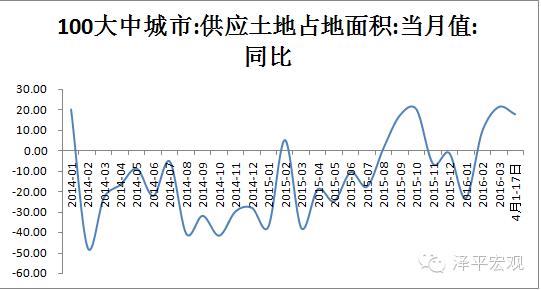

房地產開發企業土地購置麵積3577萬平方米,同比下降11.7%

【2】統計局新聞發布會,報道匯集

【3】一季度全國財收逼近4萬億 3月地方賣地收入猛增

- 公共預算支出16788億元,同比增長20.1%

- 公共預算收入11511億元,同比增長7.1%

- 財政收入增幅(6.5%)比去年全年增幅提高0.7個百分點

- 個人所得稅3150億元,同比增長18.2%,其中財產轉讓所得稅增長28.2%

- 城鄉社區支出3813億元,增長33.5%

- 資源勘探信息等支出1059億元,增長21.5%

- 住房保障支出921億元,增長24.5%

- 今年1~2月,地方政府國有土地使用權出讓收入(俗稱賣地收入)4553億元,與去年同期持平。但3月份,地方賣地收入同比增速高達16.9%

【4】一季度社會融資規模增量6.59萬億 同比多增1.93萬億

【5】3月出口由負轉正 春季廣交會或有較大改善

《財新》

【6】一季度中國出口增速逐月回穩

3月當月,中國進出口總值1.91萬億元人民幣,增長8.6%。其中,出口1.05萬億元,增長18.7%;進口8555億元,下降1.7%;貿易順差1946億元,去年同期順差為146億元

今年一季度,中國貨物貿易進出口總值5.2萬億元人民幣,比去年同期下降5.9%。其中,出口3萬億元,下降4.2%;進口2.2萬億元,下降8.2%;貿易順差8102億元,擴大8.5%

【7】海關總署:外貿形勢依然嚴峻複雜

【8】一季度GDP同比增長6.7% 符合預期

一、農業生產形勢平穩

二、工業生產緩中趨穩

三、固定資產投資增速穩中有升

四、市場銷售穩定增長

五、進出口總額下降

六、居民消費價格溫和上漲

七、居民收入增長平穩

八、結構調整步伐加快

【9】一季度固定投資增10.7% 大幅超出預期

1-3月,全國固定資產投資(不含農戶)85843億元,同比名義增長10.7%(扣除價格因素,實際增長13.8%),增速比1-2月加快0.5個百分點。

【10】3月工業增加值增速超預期升至6.8%

【11】3月CPI同比增速持平於2.3%

《新華社金融信息網》

【12】消費者價格指數

【13】生產者物價指數

2016年3月份我國CPI同比上漲2.3%,2016年3月份PPI同比下降4.3%

《財經》

【14】沈建光:中國經濟回暖背後的喜與憂

【15】俞平康:數據大增難掩隱憂 經濟還處L型拐點起始階段

【16】匯豐:中國經濟顯示複蘇跡象 但政府仍需繼續支撐增長

【17】彭博經濟學家歐樂鷹:中國一季度增速保持穩定 加碼刺激必要性削弱

【18】盛來運:將來GDP增長不是看工業臉色行事

“中國經濟不光要看速度,更要看結構,看增長的質量”;2015年消費對經濟增長的貢獻率超過60%,今年一季度仍然是這樣的狀況。“中國將來GDP的增長不是看工業的臉色行事,而是看服務業的臉色行事,這就是產業的升級”

【19】一季度全國居民人均可支配收入同比增8.7% 跑贏GDP

【20】一季度全國財政收入同比增長6.5% 財政支出增長15.4%

【21】盛鬆成:M1增速22.1%符合調控目標 反映經濟企穩趨勢

【22】統計局:農村外出務工勞動力1.68億人 同比增長2.9%

【23】中國一季度進出口同比下降5.9% 3月出口轉正增長0.9%

【24】2016年3月規模以上工業增加值增長6.8% 增速環比加快(圖)

【25】《和訊》2016年首季中國經濟數據十大解讀

【26】《中金在線》海通證券:2季度GDP或回至6.8% 貨幣政策回歸穩健

【27】《每日經濟新聞》一季度新增信貸達4.6萬億 未來能否持續?

金融數據恍若3年前;天量信貸能否持續?

【28】《經濟觀察報》6.7%增速背後的春意

【29】《中青在線》青平:十大數據亮點,傳遞中國經濟自信

【30】《鳳凰財經》國泰君安周報(2016年04月17日):春季攻勢 勢如破竹

【31】《中國財經》3月外貿數據點評:一季環比走低,二季或有改善

【32】《台灣中財網》中國一季GDP低於預期 引發黑風暴 解讀

《路透社》

【33】Chinese economy shows signs of debt-fueled recovery

【34】《RUSSELL專欄》中國取消鋼鐵出口補貼 實際影響有限但象征意義重大

【35】分析師看中國第一季GDP數據

中國一季度GDP同比增6.7%(路透調查中值為6.7%)

中國3月社會消費品零售總額同比增長10.5%, 路透調查中值為10.4%

華寶信托宏觀分析師聶文:

3月數據全麵大幅反彈,顯示經濟在一季度開始企穩回升,這主要由於房地產銷售火熱,帶動投資觸底回升,以及政府持續大力度的保增長,債務置換使得地方投資項目資金瓶頸緩解。

從目前來看,這種向好態勢有較強持續性,約能持續半年的時間,二季度經濟可能在6.8-6.9%。

房地產銷售火熱,已擴大至二線城市,不過鑒於高庫存還難以消化,市場反彈高度有限,投資向好持續時間不會太長久,1-2個季度。工業3月大幅改善一是由於補庫存,二是投資需求回升,一旦投資動能下降,工業增速也會下行。

【36】《中國2016年3月宏觀數據路透調查中值一覽表》--4月12日

【37】《中國2016年3月宏觀數據路透調查中值一覽表》--4月15日

【38】《英國廣播公司》China's transition: What transition?

“China's economic figures show an economy that's still addicted to stimulus for growth"

【39】《南華早報》Back to 1997? Why Chinese yuan and Hong Kong property prices may go down by a fifth next year

裏昂證券●中信裏昂證券有限公司(CLSA Group):“人民幣明年將於美元脫鉤”,不過信這的人沒幾個。

《華爾街日報》的一些評論

【40】5 Things to Know About China’s First Quarter GDP Growth

【41】Economists React: China Q1 Growth Slows, But March Data Offer Hope

摩根大通中國首席經濟學家和大中華區經濟研究主管朱海斌

When the government talks about stability, infrastructure investment and real estate investment are quite important. In the first and second quarters, growth momentum will continue. But we don’t expect the improvement to last for the remainder of the year. Expanded fiscal and monetary policy will probably come to a half toward the middle of this year. The government will be comfortable they can achieve this year’s growth target. Deleveraging has obviously become secondary. The government still talks about deleveraging, but it’s now on paper rather than actually being implemented. Debt will continue to pile up. We echo concerns from the International Monetary Fund over China’s corporate debt issue. The latest credit growth adds to the risk. China needs to do some more serious work cleaning up balance sheets, not only through mergers and acquisitions but also through bankruptcies. That helps banks write off bad loans and supports growth in new sectors

【42】More Property, Less Pork: What’s Behind China’s Robust Economic Figures

Pork: Prices for pork, China’s staple meat, are surging, but the increase isn’t showing up in consumer-price inflation. March’s consumer price index came in unchanged from February’s level

《華爾街見聞》

【43】中國一季度GDP增速6.7%!統計局:經濟短期可能呈現U型、W型

央行副行長易綱隔夜在華盛頓參加IMF春季會議間隙表示,他對今年中國經濟增長6.5%-7%很有信心。從第一季度數據、用電量等指標來看,中國經濟“相當強勁”。

3月製造業PMI為50.2,自2015年8月以來首次回到榮枯線以上;3月PPI環比上漲0.5%,是2014年1月以來首次轉正;

2、3月CPI同比均上漲2.3%,其中3月通脹水平低於預期,滯脹短期證偽;

前2個月規模以上工業企業利潤總額增長4.8%,為去年6月以來首次月度正增長;

3月出口暴增逾10%,進口降幅大幅縮窄。

1-3月城鎮固定資產投資同比10.7%,預期10.4%,1-2月10.2%。

3月社會消費品零售總額同比10.5%,預期10.4%。1-3月社會消費品零售總額同比10.3%,預期10.2%,1-2月10.2%。

3月規模以上工業增加值同比6.8%,預期5.9%。 1-3月規模以上工業增加值同比5.8%,預期5.5%,1-2月5.4%。

【44】外貿數據出來後 分析師都“瘋”了

【45】驚天大逆轉:中國3月出口猛增逾10% 進口降幅大幅縮窄

(人民幣結算)

(美元結算)

大多認為人民幣貶值是主要因素,發達國家經濟稍微回轉是個幫助。

【46】5個月以來首次回升!中國3月外儲意外增加103億美元

【47】人民幣企穩了 是否就可以高枕無憂?

【48】終結一年負增長!1-2月工業企業利潤同比增4.8%

【49】海通李迅雷:加杠杆、補庫存 換來開門紅——首季經濟數據解析

融資放巨量,投資加杠杆;民間投資跳水,政府投資挺進;去庫存、補庫存,都是做加法;脫實向虛格局未變,壯士已難斷腕;寬鬆貨幣政策或會遇到挑戰

【50】數據圖表

(以上諸圖見)

《彭博》

【51】China's Economy Stabilized in First Quarter

【52】China Averts a Hard Landing With a Credit-Powered Trampoline

Sugar Buzz●Currencies Rise●Consumers Spend●Debt Mountain

【53】What’s Behind China’s Stabilizing Economy?

【54】China’s Property Sector Helps Spur Economy

【55】China's GDP Data Shows a Very Predictable Pattern

【56】China's Worst Stocks Are Winning(垃圾股鹹魚翻生)

【57】Are Fears of a Hard Landing in China Justified?

【58】How Important Is China's GDP to the U.S.?

【59】PBOC's Yi (央行副行長易綱)Says Indicators Show `Robust' Economy Before GDP Data

【60】China's New Credit Growth Far Exceeds Expectations: Chart

【61】China March Home Sales Surge in Property Investment Rebound

【62】Why China’s Economy Will Be So Hard to Fix

【63】彭博北亞經濟學家歐樂鷹(Tom Orlik)在中國關係多,且彭博數據齊全,常有很多有用的信息。

《21世紀經濟報道》

【64】外貿嚴冬已結束?基數效應促反彈,出口仍難有明顯回升

【65】GDP達6.7%!一季度數據全線回暖

“當前經濟運行正在發生微妙變化。”交通銀行首席經濟學家連平表示,房地產投資超預期回升有利於推動投資企穩反彈,新開工和施工項目計劃總投資大幅反彈,預示 未來基建投資增長上行,信貸增幅加大表明實體經濟需求明顯回升,工業企業利潤恢複正增長,通縮狀況正在改善,經濟正在企穩向好。

管清友認為,二季度經濟是傳統的旺季,今年一季度的錢和去年以來的項目有望在二季度發酵。雖然中國經濟的結構性問題還沒有解決,但二季度經濟可能會出現反彈,至少經濟信心會進一步好轉。雖然一季度經濟運行初顯企穩,但是中國經濟下行壓力依然較大,一些領域的風險不容忽視,穩增長、促改革、調結構還需加碼發力。

【66】一季度GDP漲6.7% 3月拉升顯著企穩還未鞏固

【67】工業企業利潤結束下滑,經濟企穩信號待加強

【68】豬價持續上漲,CPI或超2%

【69】3月M2增13.4%顯示流動性寬裕 產能過剩行業貸款首次下降

“今年一季度末,產能過剩行業中長期貸款餘額同比下降0.2%,首次出現負增長”,就這麽一點點兒?

《金融時報》2016.04.24

China debt load reaches record high as risk to economy mounts

Gabriel Wildau in Shanghai and Don Weinland in Hong Kong

US-style credit crunch or Japan-style grinding malaise seen as increasingly likely

The Guangdong Tower seen in Guangdong Guangzhou, Guangdong Province, China, 18 April 2016. The Canton Fair, officially called the China Import and Export Fair, is the largest trade fair in China.

China’s total debt rose to a record 237 per cent of gross domestic product in the first quarter, far above emerging-market counterparts, raising the risk of a financial crisis or a prolonged slowdown in growth, economists warn.

Beijing has turned to massive lending to boost economic growth, bringing total net debt to Rmb163tn ($25tn) at the end of March, including both domestic and foreign borrowing, according to Financial Times calculations.

Such levels of debt are much higher as a proportion of national income than in other developing economies, although they are comparable to levels in the US and the eurozone.

While the absolute size of China’s debt load is a concern, more worrying is the speed at which it has accumulated — Chinese debt was only 148 per cent of GDP at the end of 2007.

“Every major country with a rapid increase in debt has experienced either a financial crisis or a prolonged slowdown in GDP growth,” Ha Jiming, Goldman Sachs chief investment strategist, wrote in a report this year.

The country’s present level of debt, and its increasing links to global financial markets, partly informed the International Monetary Fund’s recent warning that China poses a growing risk to advanced economies.

Economists say it is difficult for any economy to deploy productively such a large amount of capital within a short period, given the limited number of profitable projects available at any given time. With returns spiralling downwards, more loans are at risk of turning sour.

According to data from the Bank for International Settlements for the third quarter last year, emerging markets as a group have much lower levels of debt, at 175 per cent of GDP.

China debt web cards

The BIS data, which is based on similar methodology to the FT, put Chinese debt at 249 per cent of GDP, which was broadly comparable with the eurozone’s figure of 270 per cent and the US level of 248 per cent.

Beijing is juggling spending to support short-term growth and deleveraging to ward off long-term financial risk. Recently, however, as fears of a hard landing have intensified, it has shifted decisively towards stimulus.

New borrowing increased by Rmb6.2tn in the first three months of 2016, the biggest three-month surge on record and more than 50 per cent ahead of last year’s pace, according to central bank data and FT calculations.

Economists widely agree that the health of the country’s economy is at risk. Where opinion is divided is on how this will play out.

At one end of the spectrum is acute financial crisis — a “Lehman moment” reminiscent of the US in 2008, when banks failed and paralysed credit markets. Other economists predict a chronic, Japan-style malaise in which growth slows for years or even decades.

China debt web cards

Jonathan Anderson, principal at Emerging Advisors Group, belongs to the first camp. He warns that banks driving the huge credit expansion since 2008 rely increasingly on volatile short-term funding through sales of high-yielding wealth management products, rather than stable deposits. As Lehman and Bear Stearns proved in 2008, this kind of funding can quickly evaporate when defaults rise and nerves fray.

“At the current rate of expansion, it is only a matter of time before some banks find themselves unable to fund all their assets safely,” Mr Anderson wrote last month. “And at that point, a financial crisis is likely.”

Others believe the People’s Bank of China will retain its ability to ward off crisis. By flooding the banking system with cash, the PBoC can ensure that banks remain liquid, even if non-performing loans rise sharply. The greater risk from excess debt, they argue, is the Japan scenario: a “lost decade” of slow growth and deflation.

Michael Pettis, professor at Peking University’s Guanghua School of Management, says rising debt inflicts “financial distress costs” on borrowers, which lead to reduced growth long before actual default.

“It is wrong to assume that ‘too much debt’ is bad only if it causes a crisis, and this is a typical assumption made by almost every economist," Prof Pettis wrote in a draft of an forthcoming paper shared with the Financial Times.

“The most obvious example is Japan after 1990. It had too much debt, all of which was domestic, and as a consequence its growth collapsed.”

Distress costs include increased labour churn as employees migrate to financially stronger companies; higher financing costs to compensate for increased default risk; demands for immediate payment from jittery suppliers; and loss of customers who worry a company may not survive to provide aftersales service.

Many are now concerned that China’s debt could lead to a so-called balance-sheet recession — a term coined by Richard Koo of Nomura to describe Japan’s stagnation in the 1990s and 2000s. When corporate debt reaches very high levels, he observed, conventional monetary policy loses its effectiveness because companies focus on paying down debt and refuse to borrow even at rock-bottom interest rates.

“A financial crisis is by no means preordained but in our view, if losses don’t manifest on financial institution balance sheets, they will do so via slowing growth and deflation, à la Japan, a path China arguably already is on,” Charlene Chu, senior partner at Autonomous Research Asia, wrote recently.

Methodology: debt load obscured by complexity

Despite increasing attention to the risk from China’s rising debt, there is surprisingly little consensus over basic facts such as how much China actually owes. The increasing complexity of China’s financial system adds to difficulties in producing an authoritative estimate.

The Financial Times’ estimate of Rmb163tn ($25tn), or 237 per cent of gross domestic product, at the end of March uses data from China’s central bank on so-called “total social financing” (TSF), which covers lending to the non-financial sector by both banks and non-banks. It then adds finance ministry and National Audit Office data on, respectively, central and local government debt. Finally, data from Wind Information, a Chinese financial database, is used for government bonds issued in early 2016 but not yet reflected in NAO and finance ministry figures.

The FT’s methodology is similar to that of the Bank for International Settlements, which in September released a database that tracks total debt in 42 big economies. In addition to drawing on more recent TSF and NAO data, the FT seeks to eliminate possible double-counting in the BIS figures. Double-counting may arise from local governments’ use of special-purpose vehicles to borrow. Such borrowing is counted as corporate debt in TSF data but as government debt by the NAO.

Some analysts estimate that China’s debt load is significantly higher than both the FT and BIS estimates. A widely cited report by McKinsey last year placed China’s debt at 282 per cent of GDP by mid-2014, an estimate that includes debt owed by financial institutions.

Many analysts believe the McKinsey estimate suffers from significant double counting, since the money that banks and other financial institutions borrow is lent on to non-financial borrowers. But some analysts also believe that for China, including at least some financial debt is necessary to capture shadow-bank lending that is not included by TSF.

Rodney Jones, principal of Beijing-based Wigram Capital Advisors, provides Asia macro analysis to billionaire investor George Soros, who last week likened China’s economy to the subprime-saddled US before 2008. Mr Jones says Chinese banks use investments in wealth management products to disguise corporate loans as financial debt. Based on a detailed analysis of financial statements by more than 100 banks, he estimates China’s debt-to-GDP ratio at 280 per cent at the end of 2015.

“The financial engineers have run amok again. They’ve run amok in the US and they’ve run amok here. That’s what George sees," says Mr Jones.