笨狼發牢騷

發發牢騷,解解悶,消消愁

前天說起日本央行是如何嚴懲國際日元炒家的?,提到實際上索羅斯並未做空人民幣,隻是看糟中國經濟,自然覺得人民幣會貶值。不過,做空人民幣的自然大有人在,華爾街日報報道點出四人:Kyle Bass, Stanley Druckenmiller, David Tepper, and David Einhorn。Kyle Bass和David Einhorn都是做空美國次貸危機成名、發的,兩人這幾年對美國經濟一直不報樂觀態度,對多債務(如希臘)常有聳人聽聞的言論,估計一直沒賺錢來著;David Tepper則吃聯儲救市,做多美國股市發了大財;Stanley Druckenmiller是老資格,洗手多年,近年來常常警告美國經濟已陷入死胡同。

Kyle Bass

David Einhorn

Stanley Druckenmiller

David Tepper

比起歐元日元對美元大肆貶值,人民幣實在是為世界做了貢獻:

貶這麽一點點兒,算什麽?但這個世界真殘酷,大家是如狼似虎般的狠,一有點兒不妥,以前的全忘了。

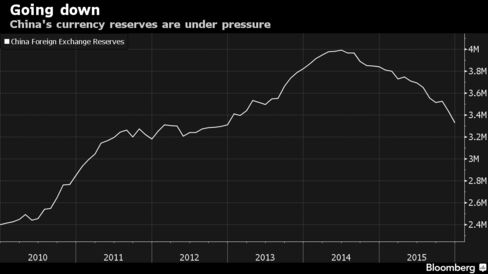

人民幣會大幅貶值嗎?貶值的主要理由是中國產品因貨幣過強而失去競爭力,比起日本歐洲,處境很難。沒有出口,企業倒閉,就業成了問題,進而引起社會動蕩。因為這個壓力很大,去年中國外匯流失不少,彭博的報道:

《彭博》China's $1 Trillion Money Exodus Isn't About Capital Controls

中國外匯儲備

如彭博所言,如果5%的人口擔心,將每年允許的50000美元匯到國外,那中國外匯儲備所剩下的3萬3千億救光了。那是自己人自殺,幾個大鱷,不會成氣候。

那人民幣會真會大幅貶值嗎?已經貶了6-7%(左右)了,出口企業翻不了身,也緩過一口氣來了。中國出口企業缺乏競爭力,貨幣是一個因素,但不是主要的。大部分企業靠吃政府,吃慣了,產能過剩也反映到出口上,大家一擁而上,拚命賤賣,賺的就是政府的補貼,自相殘殺是常事。這種情況,很多企業被淘汰時必然、應該的。但基於中國巨大的產量,這未必會影響出口全局。去年中國混的還可以,說要一千萬個新職位,結果一千兩百萬個,算李克強的。所以,不必擔心就業,要擔心的是,銀行往往因為政府鼓勵、變相擔保、多端要求給這類就業型企業貸款,不少企業目前處於低迷狀態,債務過度,甚至連利息也難以擔負:

2015.11.237.6萬億隻為付利息,以債養債能維持多久?

一旦這些企業倒閉,銀行的貸款怎麽辦,也許沒轍得救銀行。央行擔心人民幣的穩定性遠高於對出口的救濟。

人民幣貶值的另一個因素是美國漲利息。去年年底美國聯儲開始首次漲利息,給人的感覺是過去的日子是一去不複返了。這給全世界資本巨大的心理壓力,不但中國,幾乎所有發展中國家都麵臨這個問題。心理壓力很厲害,即使有頭腦的人也往往不顧現實,不做分析,大家也是一哄而上,形成潮流,結果形勢難以逆轉。其實第一美國利息還是極低,美聯儲三番五次強調不會大幅加息,整個過程會慎重、緩慢。第二,美聯儲跟中國“央媽”沒什麽區別,整天擔心股市動蕩,(有錢人)虧錢了,大家一嚷嚷,聯儲就心軟了,也心慌了,不會采取過多的行動。目前美國利率市場和美國經濟學家的預測也是今年頂多會加兩次息,而不是聯儲暗示的四次。第三,聯儲也擔心美元過高會影響美觀企業的競爭力,這跟中國央行的難題一樣。停止上調利率而避免貨幣升值以暗地支持本國企業在世界上的競爭力,也算“操縱貨幣”,聯儲嘴裏不提,但還是要做的。

我在日本央行是如何嚴懲國際日元炒家的?說起“人民幣貶,不但影響中國和世界對人民幣的信心,給人民幣剛剛加入國際貨幣基金組織特別提款權(SDR)帶來瑕癡,不利建立人民幣國際貿易結算貨幣的地位,也導致中國外匯外流“,人民幣作為中國貿易甚至世界貿易結算貨幣,對中國走向世界很關鍵,故此人民幣也不能輕易貶值。這是一篇學術文章:

China’s ‘hidden’ current account deficit; invoicing decisions and liquidity effects on EMs

它提到一旦貶值,中國的亞洲交易國會要求以美元結算,進一步加劇貶值。

外流這麽厲害,要管製外匯嗎?連日本央行行長黑田東彥(Haruhiko Kuroda)都建議中國管製:

《彭博》2016.01.2 Kuroda Advises China to Impose Capital Controls to Defend Yuan

《彭博商業周刊中文版》2015.03.19 盤點中國富豪轉移資金的9條密道

密道一:螞蟻搬家

密道二:賭場洗錢

密道三:地下錢莊洗錢

密道四:銀行“內存外貸”

密道五:換匯中介操作

密道六:虛開發票金額

密道七:虛假貿易“搭便車” 虛增進口價格外流資金

密道八:設虛假公司

密道九:海外並購“混出去”

政府正在采取的手段:

《彭博》

2016.01.27 Here's What China Is Doing to Tighten Noose on Capital Flows

2016.02.02 China Unleashes New Steps to Control Financial Risks, Outflows【參見:《一財網》離岸人民幣流動性縮緊 做空人民幣不容易】

China to Plan Looser Limits on Foreign Fund Outflows【注:這隻是針對外資,不是國內資金外流】

《路透社》

2016.01.15

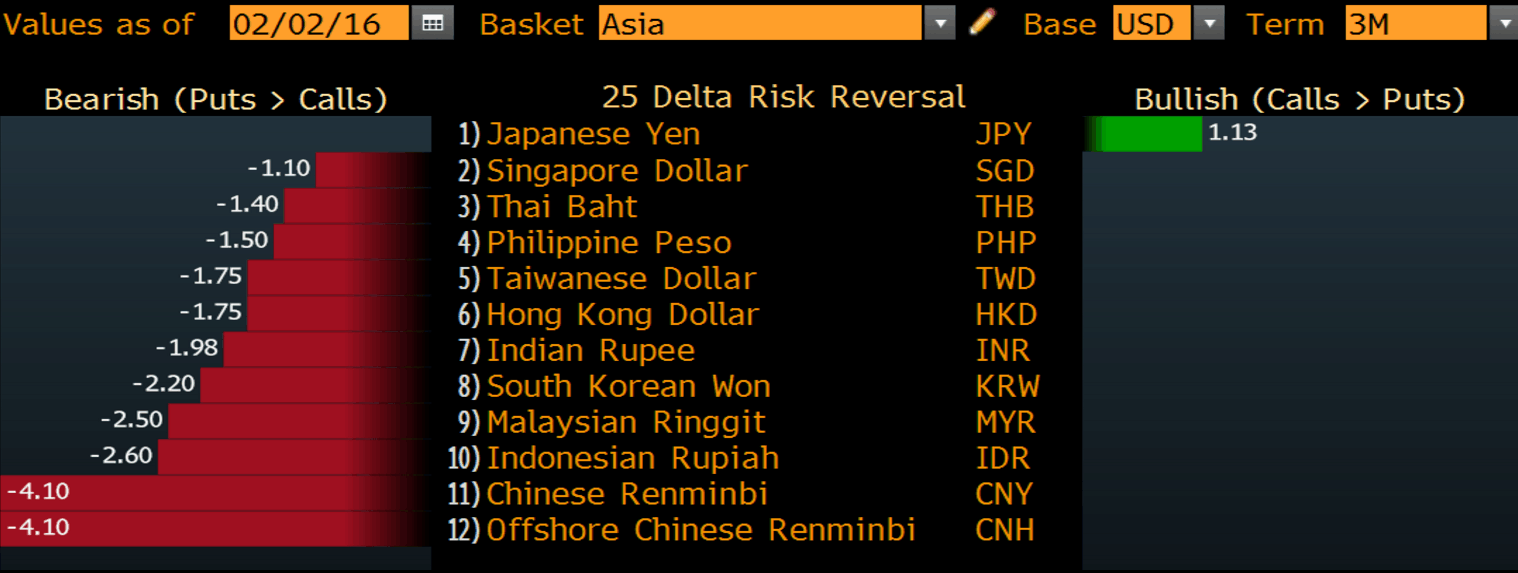

人民幣會貶值多少?對衝基金將目光瞄向15%

2016.01.19

中國央行嚴控跨境人民幣資金池業務 緩解資本外流壓力

2016.01.27

中國試圖讓外界相信人民幣將保持穩定 但投資者存疑

分析:人民幣匯率能走穩多久?

《21世紀經濟報道》2016.01.15

曝光不良資產騰挪術:銀行采用多種方式逃避監管

《財新周刊》2015.11.30

不良貸款騰挪術

2016.012.03 外媒:人民幣空頭卷土重來 上個月曾被中國央行擊退

有些情形拋售人民幣也屬迫不得已,比如中國有些企業在國外借錢,就是在國外發行債券。國外發行,自然是美元債券了。結果現在人民幣貶值,還有進一步貶的可能性,企業們沉不住氣了(彭博:China Has $23 Billion in Debt That Could Be Cut to Junk,中文翻譯降級潮來臨:230億美元中企外債逼近垃圾級),據統計,

2015.12.30 外管局:截至9月末中國外債1.529萬億美元

廣義政府債務餘額為6665億元人民幣(等值1048億美元),占7%;中央銀行債務餘額為2599億元人民幣(等值409億美元),占3%;銀行債務餘額為44758億元人民幣(等值7035億美元),占46%;其他部門債務餘額為30239億元人民幣(等值4754億美元),占31%;直接投資:公司間貸款債務餘額為13057億元人民幣(等值2052億美元),占13%

德國商業銀行中國經濟學家周浩早些在

2015.08.15 理性判斷中國外債風險

說“2015年第一季度末時,中國的外債存量較2014年相比下降了3%,存量規模為8,700億美元左右”。不論如何,美元外債得回贖,那就得用美元還給債主,就得用人民幣買美元,結果跟拋售人民幣搶購美元無異,給人民幣增加了一個壓力。

據此,我相信人民幣不會大幅貶值,也不會比目前掉多少。華爾街的人說“押人民幣大跌(就像賭錢)的(賭)注,已經下了“,中國政府怎麽說都沒用。當然了,不過,中國政府頂著,人民幣不(大)掉,他們能不能賺錢,就說不準了。

《華爾街日報》【中文翻譯】

Currency War: U.S. Hedge Funds Mount New Attacks on China’s Yuan

Bets against the yuan by hedge funds come at a time of enormous sensitivity for Chinese leaders

By Juliet Chung and Carolyn Cui

Jan. 31, 2016

Some of the biggest names in the hedge-fund industry are piling up bets against China’s currency, setting up a showdown between Wall Street and the leaders of the world’s second-largest economy.

Kyle Bass’s Hayman Capital Management has sold off the bulk of its investments in stocks, commodities and bonds so it can focus on shorting Asian currencies, including the yuan and the Hong Kong dollar.

It is the biggest concentrated wager that the Dallas-based firm has made since its profitable bet years ago against the U.S. housing market. About 85% of Hayman Capital’s portfolio is now invested in trades that are expected to pay off if the yuan and Hong Kong dollar depreciate over the next three years—a bet with billions of dollars on the line, including borrowed money.

“When you talk about orders of magnitude, this is much larger than the subprime crisis,” said Mr. Bass, who believes the yuan could fall as much as 40% in that period.

Billionaire trader Stanley Druckenmiller and hedge-fund manager David Tepper have staked out positions of their own against the currency, also known as the renminbi, according to people familiar with the matter. David Einhorn’s Greenlight Capital Inc. holds options on the yuan depreciating.

The funds’ bets come at a time of enormous sensitivity for China’s leaders. The government is struggling on multiple fronts to manage a soft landing for the economy, deal with a heavily indebted banking system and navigate the transition to consumer-led growth.

Expectations for a weaker yuan have led to an exodus of capital by Chinese residents and foreign investors. Though it still boasts the largest holding of foreign reserves at $3.3 trillion, China has experienced huge outflows in recent months. Hedge funds are gambling that China will let its currency weaken further in a bid to halt a flood of money leaving the country and jump-start economic growth.

The effort is a lot riskier, though, than taking on a currency whose value is set by the market. China’s state-run economy gives the government a number of levers to pull and tremendous resources at its disposal. Earlier this year, state institutions bought up so much yuan in the Hong Kong market where foreigners place most of their bets that overnight borrowing costs shot up to 66%, making it difficult to finance short positions and sending the yuan up sharply.

The situation grew more tense after billionaire investor George Soros predicted at the World Economic Forum gathering in Davos, Switzerland, recently that “a hard landing is practically unavoidable” for China’s economy. He said he is betting against commodity-producing countries and Asian currencies as a result.

George Soros, of Soros Fund Management, at the World Economic Forum in Davos, Switzerland, recently. He said he is betting against Asian currencies. ENLARGE

George Soros, of Soros Fund Management, at the World Economic Forum in Davos, Switzerland, recently. He said he is betting against Asian currencies. Photo: Bloomberg News

Days later, a commentary appeared in China’s state-run Xinhua News Agency warning that “radical speculators” trying to short sell, or bet against, the Chinese currency would “suffer huge losses” as the Chinese monetary authority takes “effective measures to stabilize the value of the yuan.”

A spokesman for Soros Fund Management, Mr. Soros’s family office, declined to comment on the firm’s currency positions.

The show of force has scared off some fund managers from adding to their wagers. Some traders have scaled back or even exited from their short bets, saying they have little appetite to go up against the Chinese government. Some say they are looking with new interest at shorting the currencies of other Asian countries that they expect would fall if the yuan keeps depreciating.

The standoff harks back to big battles such as Soros’s bet against the British pound a quarter-century ago. In 1997, Malaysia’s prime minister blamed Mr. Soros for a run on the ringgit during the Asian financial crisis. Mr. Druckenmiller, then chief investment officer for Soros Fund Management, said at the time that while the main Soros hedge fund had earlier shorted the ringgit, it bought the currency during the crisis, cushioning its fall.

Hayman Capital began betting against the yuan last year after studying China’s banking system and being stunned at its rapid expansion of debt. The firm’s analysis suggested that past-due loans, which currently stand at about 2% of the total, would rise sharply and eventually require an injection by the central government of trillions of dollars of yuan to recapitalize the banks. An expansion of the Chinese central bank’s balance sheet would lead its currency to weaken, just as the dollar depreciated when the Federal Reserve bailed out U.S. banks during the financial crisis.

Broader market bets against the yuan began growing last August, when the People’s Bank of China unexpectedly devalued the currency by 2% against the U.S. dollar. The move fueled speculation that Beijing eventually would have to decouple the yuan from the strengthening dollar and follow other countries to weaken its currency as a way to buoy growth.

Mr. Druckenmiller, who now invests his own wealth, and one of his former protégés, Zach Schreiber, who runs the roughly $10 billion hedge-fund firm PointState Capital LP, also have had sizable shorts against the renminbi since last year, people familiar with the matter said.

The wager helped PointState gain about 15% last year, said a person familiar with the firm, and has contributed to gains of more than 5% through mid-January.

Traders who remain bearish now are shorting China’s currency in several ways, say people familiar with the trades. Some are betting that the gap between the currency’s onshore exchange rate and more market-sensitive offshore rate will diverge further. Early in January, the spread hit a record of 0.1367 before government intervention narrowed it sharply.

Two days before China devalued its currency last August, William Ackman’s Pershing Square Capital Management LP began to put on a “large notional short position in the Chinese yuan through the purchase of puts and put spreads” to hedge against “unanticipated weakness in the Chinese economy,” according to Mr. Ackman’s annual investor letter, disclosed this past week.

But, demonstrating how difficult it can be to profit from such bets, Mr. Ackman said in the letter the wager had generated only a modest profit for Pershing Square and had been insufficient to offset the firm’s larger losses, as China continued to defend the exchange rate.

Mr. Ackman wrote that he continued to hold the position because of its importance as a hedge.

Other firms that have profited from shorting China’s currency include the $2 billion Scoggin Capital Management and Carlyle Group LP’s Emerging Sovereign Group, according to people familiar with the matter.

For 2016, ESG’s short-China fund, Nexus, was up more than 20% partway through January, according to people familiar with the fund, thanks in part to a large short position against the yuan. Much of Nexus’s position is made up of options, one of the people said.

It was unclear how much exposure Greenlight and Mr. Tepper’s Appaloosa Management LP have, though Mr. Tepper was outspoken last year in calling the yuan overvalued.

Since August, China has been imposing various rules to stabilize the exchange rate and stem the outflows, including a 20% reserve requirement applied to onshore yuan-derivative trades. That move makes it more expensive for funds to keep shorting the currency through swaps.

Chinese officials have indicated they aren’t seeking to devalue the yuan in order to gain advantage over their trading partners, citing the need to avoid a damaging spiral of competitive devaluations as others follow suit. The country still has room to stimulate its economy through fiscal policies, economists say.