笨狼發牢騷

發發牢騷,解解悶,消消愁

聯儲(美國央行)今年加息已成定局,最後一次年會下月(12月)舉行,肯定會加息0.25%(俗稱25個基點)。原來9月的會議,大家公認會加,但聯儲一中國經濟疲弱(股市動蕩)進而影響世界和美國經濟為理由展緩,大家暗地裏大罵聯儲被(美國)股市綁架,實屬為有錢人效命。

現在中國的動蕩算是壓下去了,美國經濟也還不錯,除了10月就業火紅外,就目前的數據來看,三季消費也很強【4】,所以能有的借口都沒了。

利率改變短期內對股市影響甚大,聯儲明說是為了經濟,暗地裏整天為股市擔心,那地步跟中國政府不相上下,一般的德性,故此,聯儲一直給大家暗暗(又不能公開,因為公開是違法的)做思想工作,唯恐大家不知道,該打的報告,都打了【2】,基本上是連幼兒園的小朋友都明白了。伯克利的一教授研究說聯儲的方式完全是有一套固定的模式:

U.S. central bankers not only regularly leak secret information about monetary policy, but the leaks are so predictably timed that a savvy investor without access to the leaked information could make money just by buying stocks in certain weeks

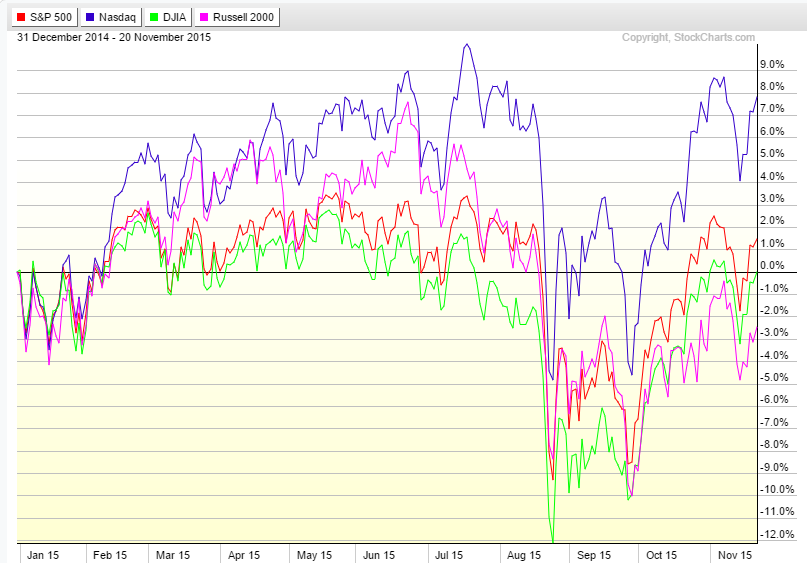

美國主要股指今年表現

美國加息,美元就長:

歐洲巴不得美國加息,出口就更有力了。發展中國家大都反對,有的擔心資金外流,資源國擔心資源貶值,對自己的經濟是個巨大的打擊。不過,美國是不會買大家的賬的。

蹊蹺的是周末聯儲發消息說明天(周一)會開一次特殊的會議,說是“沒什麽特別的”。大家反應不大,不過還是有人揣摩【5】是不是明兒就真的給漲了?

【1】《路透社》Pssst, want to play the market? Count the Fed leak weeks

【2】Fed Watch: Mission Accomplished

【3】Goldman Sachs: Expect FOMC to Raise Fed Funds Rate 100bp in 2016

【4】Analysts: Q3 GDP to be Revised Up

【5】下周一 美聯儲可能就開始“加息”?

【附錄】

《金融時報》2016.01,11

China banks feel the heat of meltdown

Patrick Jenkins

Lenders could require up to $7.7tn of new capital and funding over the next three years

If the US or Europe had experienced the kind of equity market slump that China has suffered of late, its financial institutions would be quaking and leading the list of biggest fallers in Shanghai and Hong Kong trading.

As it is, the big banks have seen their share prices tumble by about 10 per cent over the past two or three weeks, far less than the 15 per cent slump in the Shanghai Composite index. On the face of it, there may be good reason for that. Traditionally China’s large financial institutions are not big stock market players — retail investors make up the bulk of the market.

In reality, the banks are the most exposed to China’s ills.

They are directly bound up in the stock market turmoil and the government’s efforts to shore up sentiment against the flood of selling. Figures relating to the past week or so are not yet available. But during a similar rout in early July last year, 17 banks — including the big five listed but partly state-owned groups — lent more than $200bn to facilitate broker purchases of shares and funds.

Even without the seizure of their balance sheets to prop up the equity market, China’s banks are pretty troubled.

Like banks in the west before the financial crisis, China’s lenders — with government encouragement — have inflated a vast credit bubble, funding the country’s ambitious companies and fast-expanding property market. Chinese banking assets now amount to more than $30tn.

Over the past decade, credit growth has consistently topped 10 per cent a year. (It peaked at close to 35 per cent in 2009.) Even this year, it is expected to be double the 6-7 per cent forecast rate of GDP growth. Last August, JPMorgan estimated China’s non-financial industry private sector debt at 147 per cent, half as much again as in 2007.

The downturn in China’s fortunes — particularly across its heartland heavy industry — is already hitting the banks. Annual non-performing loan rates have been doubling annually since 2012. China Merchants Bank, China Everbright and ICBC are seen as among the most troubled.

China bulls point to the still low level of NPLs — barely 1 per cent at the big lenders, and 1.8 per cent at mid-tier banks this year, according to analyst forecasts. As a gauge, NPLs in Greece have risen to between 30 and 40 per cent amid that country’s crisis.

But China experts at independent research house Autonomous suggest investors are underestimating a spiralling problem. Across the board, loan losses will rise by $845bn this year, Autonomous predicts. That, they think, will be enough to shrink profits by 6 per cent at big banks.

The bearish outlook reflects concern about hidden forbearance policies on outstanding loans and the rapid growth of misleading wealth management products. Some banks have been redefining lending as investments which may not sit on their balance sheets. When a bank loan is turned into an investment product with the assistance of a non-bank — or “shadow bank” — partner, the lender escapes rules on loan loss provisioning and capital. It also swaps a thin lending margin for more highly regarded fee income. Autonomous reckons that in the first half of 2015 alone, this kind of non-loan credit jumped by Rmb1.5tn, or more than a third, across the nine banks it covers.

Some policymakers are privately worried about yet another underestimated issue — whether loan losses, when they materialise, will be recoverable. In western banking markets, so-called loss given default rates can typically range between 30 and 70 per cent. In China, where property accounts for the bulk of collateral used to back loans, LGDs may be far higher. Even if inflated property values do not collapse, collateral values may prove far too optimistic. In China’s nascent property ownership culture, the land on which developments are built is typically state-owned, limiting recovery values.

Investors in China’s banks may well recognise that the lenders cannot be compared with institutions that operate along western lines and will expect hazier disclosures and readier state interference. They are also likely to think that China will not allow its banks to fail. But if analysts, like those at Autonomous are to be believed, China’s banks could require up to $7.7tn of new capital and funding over the next three years. State bailouts could send the government debt to GDP ratio spiralling from 22 per cent to 122 per cent. That kind of shock would be a challenge for any country, even one of China’s vast might.