笨狼發牢騷

發發牢騷,解解悶,消消愁

正文

大題昨天說了,美國一季經濟幾乎停止不前,美國一季經濟失望:

確實沒麵子。圓場的說,還好了,沒減產,而且,同比還不賴:

有人說中國也就這水平(不是剝去通脹後的,大家常說的增長值),因為一季度中國整個物價貶值(通縮),“名義上”的總產值增長率很低。美國要跟中國比個頭,就看這“名義上”的總產值,所以趕上中國了。

對整天為三頓發愁的人來說,這無異扇了個耳光,整個沒心沒肺,因為工資沒漲,通脹,窮人越窮,而富人的資產者增值了,更有錢了。

什麽撐著本季度的經濟了?廠家的庫存(Inventory):

這說明企業廠家信心十足,開足工廠生產。在美國的“老常態”講到美國去年下半年總產值說,醫保消費是主力(本季還是,見下),這次沒有庫存(Inventory),或“囤積”,總產值增長率非得是負的不可。

昨天聯儲定論,“暫時性的”,皆因一季天氣影響,以後會好的。不信的:

華盛頓郵報博文:Why you should be skeptical of the biggest excuse for the weak economy

專門點批了經濟學家Kellner的意見:Opinion: Second-quarter GDP will tell the tale。

聯儲也有道理,美國就業還是穩健,今早失業報告說,領救濟金的人15年來最低了:

聯儲的話有分量,因為聯儲說什麽,對美元又直接的影響,不但對美國進出口至關重要,還影響著石油(和黃金)。這是美元小時圖,美元開始大跌,聯儲表態後反彈:

最煩的是經濟學家,老說都知道了,老錯,還活的好好的。

出口拖了總產值後腿,什麽幫了忙?消費的項目裏:

醫保、房子維修保暖之類是主力。

但整個消費雖然沒死,也馬馬虎虎,還能撐著嗎?

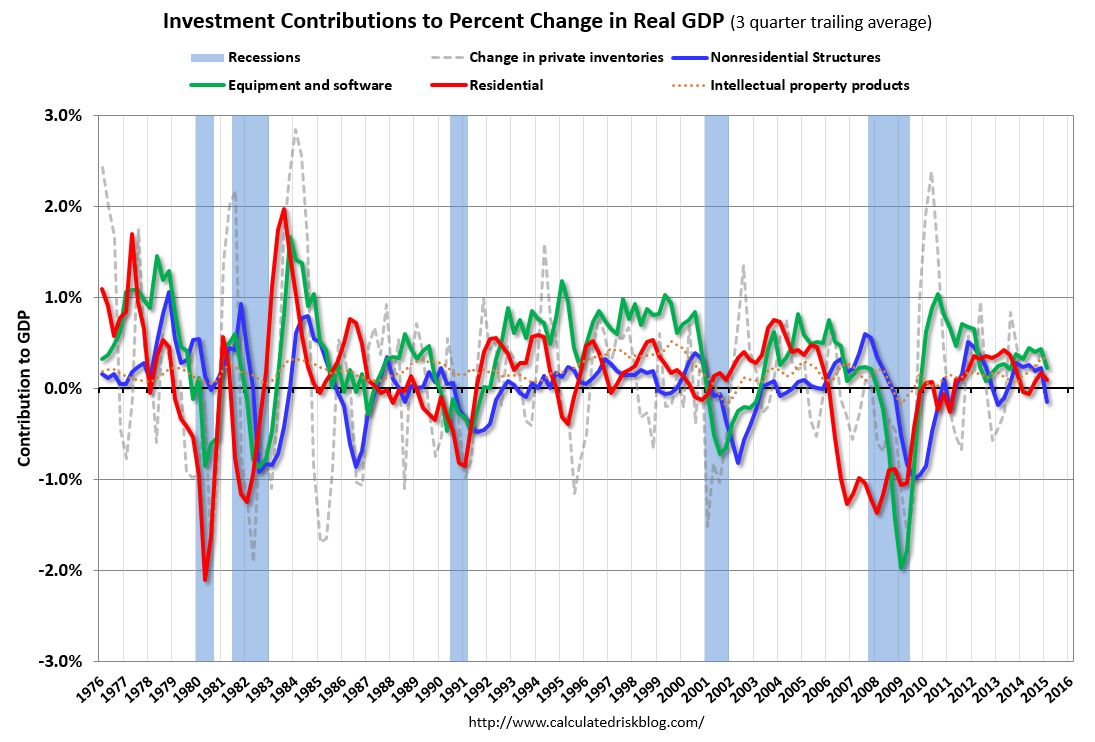

投資低迷,油價、頁岩油業的影響,還是整體經濟?

還是投資圖:

房產業投資:

房產業投資占經濟的比例:

感覺是美國百姓不會有反應,接著花錢。

(點擊放大)

我們不懼!

現實如何呢?一季度預測最準的聯儲亞特蘭特分行如是說:

一季成績:

還是一團糟。美國人得使勁兒。

確實沒麵子。圓場的說,還好了,沒減產,而且,同比還不賴:

有人說中國也就這水平(不是剝去通脹後的,大家常說的增長值),因為一季度中國整個物價貶值(通縮),“名義上”的總產值增長率很低。美國要跟中國比個頭,就看這“名義上”的總產值,所以趕上中國了。

對整天為三頓發愁的人來說,這無異扇了個耳光,整個沒心沒肺,因為工資沒漲,通脹,窮人越窮,而富人的資產者增值了,更有錢了。

什麽撐著本季度的經濟了?廠家的庫存(Inventory):

這說明企業廠家信心十足,開足工廠生產。在美國的“老常態”講到美國去年下半年總產值說,醫保消費是主力(本季還是,見下),這次沒有庫存(Inventory),或“囤積”,總產值增長率非得是負的不可。

昨天聯儲定論,“暫時性的”,皆因一季天氣影響,以後會好的。不信的:

華盛頓郵報博文:Why you should be skeptical of the biggest excuse for the weak economy

專門點批了經濟學家Kellner的意見:Opinion: Second-quarter GDP will tell the tale。

聯儲也有道理,美國就業還是穩健,今早失業報告說,領救濟金的人15年來最低了:

以前多次說過,美國如火如荼的經濟主要體現在就業上,總產值很難見到,資產也增值,窮人未必得到多大的好處。

參見我的其它經濟帖子

聯儲的話有分量,因為聯儲說什麽,對美元又直接的影響,不但對美國進出口至關重要,還影響著石油(和黃金)。這是美元小時圖,美元開始大跌,聯儲表態後反彈:

最煩的是經濟學家,老說都知道了,老錯,還活的好好的。

Deutsche Bank's (德銀) US chief economist Joseph Lavorgna(吹鼓手) — writing before the release — picked up on the uncertainty it creates: "These figures are highly preliminary and prone to massive revisions. Last year, the first reading on Q1 output was reported at 0.1%, only to be revised down to -1.0% one month later and then to -2.9% one month after that."

...

Additionally, there was a much larger inventory build ($110 billion) in Q1 than what we had expected—it added 74 basis points to Q1 real GDP. This was the largest inventory accumulation since the $116.2 billion build in Q3 2010. Given the fact the various regional purchasing manager surveys have been weak in April, it appears that producers will allow inventory positions to run off. This tells us that current-quarter growth is likely to run around 2.5%, not the 4% snapback we had previously been anticipating.

強勁美元對出口的影響

華爾街日報(悲觀居多) “In an entirely unsurprising turn of events, first quarter GDP was weaker than expected, growing just 0.2% as compared to the 1.0% rate expected. To repeat a refrain of ours, weakness in the first-quarter GDP report is not exclusive to 2015; we’ve seen this for the entire recovery….Our working assumption is that this quarter, like previous first quarters, will be the year’s low point and the economy should accelerate from here. Admittedly, the data does not yet support the type of snapback seen in 2014, but more growth is better than less and we expect that to occur this year.” –Dan Greenhaus, BTIG

“You were forewarned. First-quarter economic activity was not pretty. But that was pretty ugly. Real GDP in the first quarter barely registered a gain, rising just 0.2% annualized, the slowest pace since the polar-vortex quarter a year ago. (And before that, the fourth quarter of 2012.) But the positive takeaway is that all of the temporary factors that held activity back were just that–temporary. And the second quarter is widely expected to rebound.” –Jennifer Lee, BMO Capital Markets

WSJ’s Josh Zumbrun joins MoneyBeat and explains whether surprisingly downbeat first-quarter GDP report should be seen as a blip or a trend.

“The U.S. economy all but stagnated in the first quarter, as lower energy prices triggered a big drop in mining investment, but did little to boost consumer spending because of the impact of the unseasonably cold winter in the Northeast. The 0.2% annualized gain will raise fears that the recovery is somehow coming off the rails but, just like last year, we anticipate a marked acceleration in growth over the remaining three quarters of this year. Over the past 12 months the economy has expanded by 3% and we would expect it to continue growing at around that pace this year too.” –Paul Ashworth, Capital Economics

“A quick look at the underlying numbers suggests few surprises. Consumption of +1.9% was okay, not great, and concentrated in weak durables demand. Business investment was very poor, falling 3.4%, which a bit weaker than our numbers, revised in the wake of durables. Exports lower, imports higher. That’s the clearest evidence that the rising dollar is impairing growth, though the number was a bit worse than we’d forecast. Further declines in defense spending were also a decent headwind for the quarter. This is another quarterly number which confirms the long term ‘slo-gro’ thesis, but there are good odds we get a bit of a bounce later in the year from (a) stabilized business spending and (b) the housing markets, which are setting up quite promising.” –Guy Lebas, Janney Montgomery Scott

“In short, even weaker than expected. We believe weakness was grossly exaggerated and there will be significant catchup in the second quarter, but, of course, that remains to be seen. Apart from fundamental slowing and normal volatility, possible factors include harsher-than-usual winter weather, port delays and seasonal adjustment problems relating to the first quarter specifically. More fundamentally, lower oil prices account for the plunge in the mining component of business investment in structures, although we think the positive effects of lower oil prices will ultimately offset the negative effects. Also, not all the weakening in exports appears to be due to port delays. All in all, we believe the underlying trend is still at least 2.5% and we forecast catchup with a 4.0% pace in the second quarter.” –Jim O’Sullivan, High Frequency Economics

“Most of this deceleration is likely transitory—due in part to particularly bad weather in the first quarter. Growth in the rest of 2015 will most likely be faster than previously projected, as the economy bounces back from this weak start to the year. Yet data on GDP in recent years confirms that the U.S. economy has not reached escape velocity—growth rates have not broken past the 2%-2.5% pace that normally is associated with rapid declines in economic slack. Because growth has been steady for years, it might be tempting for some policy makers to shrug their shoulders and declare that this is the ‘new normal’ and the best we can do. The economic evidence clearly suggests otherwise—this economy still needs active measures to boost demand to achieve a full recovery. At a minimum, this means the Federal Reserve should put off interest rate increases for the rest of 2015.” — Josh Bivens, Economic Policy Institute

出口拖了總產值後腿,什麽幫了忙?消費的項目裏:

醫保、房子維修保暖之類是主力。

但整個消費雖然沒死,也馬馬虎虎,還能撐著嗎?

投資低迷,油價、頁岩油業的影響,還是整體經濟?

還是投資圖:

房產業投資:

房產業投資占經濟的比例:

感覺是美國百姓不會有反應,接著花錢。

(點擊放大)

我們不懼!

現實如何呢?一季度預測最準的聯儲亞特蘭特分行如是說:

一季成績:

還是一團糟。美國人得使勁兒。

評論

目前還沒有任何評論

登錄後才可評論.