子夜讀書心筆

寫日記的另一層妙用,就是一天辛苦下來,夜深人靜,借境調心,景與心會。有了這種時時靜悟的簡靜心態, 才有了對生活的敬重。

The penny that dropped and smashed over the past year was the almost blind belief that markets can value assets reliably. That’s something that George Soros figured out years ago, his idea of “Reflexivity” is based around the notion that markets frequently misprice assets; housing did not fall off a cliff for any other reason, except that it was on top of a cliff in the first place, the same goes for the stock market in 1929 and Dot.com.

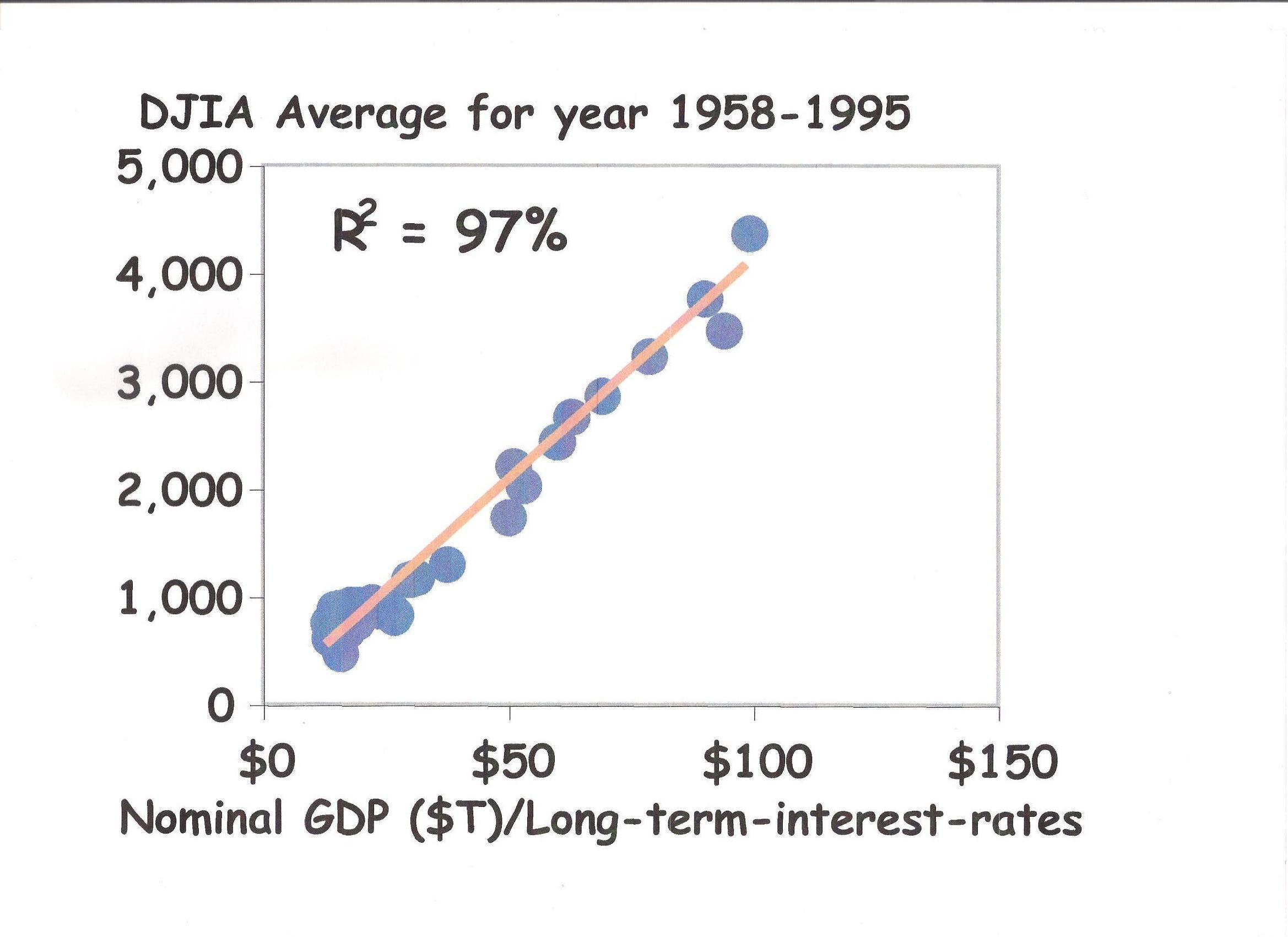

But leaving that to one side, historically whenever the stock market was not grossly mispriced the impact of long-term-interest rates on prices is pretty clear.1 1958 to 1995 represents a period in time when there were not any extreme dislocations from reality (in the stock market - and it’s not hard to know when those occur, because at some point there is a dramatic reversal).

You won’t find that in any economic text-book, because economists are obsessed with “real” GDP, as if their calculations of inflation are somehow “real”. Nominal is real, it’s a measurement of the amount of money sloshing from one pocket to another, measured three ways, it’s just counting, everything else is politics.

The reason for the correlation is (probably) because nominal GDP (today) is a good proxy for "real" future earnings (apparently better than trailing earnings, and with the advantage that benchmark is more independent of manipulation under US GAAP which allows for actual losses to be hidden for years (you don’t think the banks lost all that money in Q2 and Q3 2008 do you?))2.

And long-term interest rates are historically a proxy for the discount rate for an income capitalization valuation.

That affects the base-line around which markets get mispriced, which if history is any guide suggests that the US stock markets have to be 42% under-priced about now to follow the inevitable oscillation. That's not hard to figure out, what's hard is figuring out where the base line goes.

I have previously argued that if long term interest rates average 3.5% in 2009, and assuming nominal GDP doesn't drop by more than it did in Q1 (3.5% annualized), the average for the DJIA "ought" to be about 10,000 "ought" to be about 10,000; so far the average was about 8,000 so if that's right, that means the only way is up.

Granted, perhaps all the debt that USA is piling on will push up long-term interest rates (it's either that or let the dollar tank against Asian currencies, which Secretary Geither thinks should have happened by now anyway), but even at 4.5% the Dow "ought" not to end up less than 9,000 average in 2009.

But there is a catch:

For as long as anyone can remember the cost of corporate debt has pretty much tracked Treasuries of a similar maturity plus 100 to 200 basis points; so the correlation in the past could equally have been driven by the cost of corporate debt.

Over the past nine months the link between Treasuries and corporate debt changed, and radically; nowadays corporate bonds are trading at as much as 600 basis points above Treasuries.

That's similar to what happened in Japan after their real estate boom and bust; the rates that banks paid were cut to almost zero, but ordinary businesses found themselves paying as much as 25% for debt.

That kills new business ideas and projects, because the investor IRR you achieve on a new venture depends on gearing; (so long as you can find debt at a cost lower than the project IRR, and that's not happening). It also punishes anyone who is leveraged up, and needs to roll over.

That might explain the stagnation in Japan after their experiment with the joys of a real estate boom-bust; so in spite of the fact that they did everything "right" that the US is doing or aiming to do now with it’s cocktail of weapons - (dropping interest rates to zero (Friedman), QE and building bridges to nowhere (Keynes), and propping up zombie banks (Mugabe)), basically their economy went nowhere. The difference is that they ran a current account surplus and they had a strong manufacturing base.

Put 8% into that equation and the "right" average price for the Dow in 2009 is 7,500; put 10% in and it's 7,000; that’s down from now.

Reality is probably somewhere in-between which suggests that until corporate bond yields start to get back in line with Treasuries, the stock markets might well just shuffle sideways.

Perhaps the US government might profitably be doing more to help its non-financial industries to raise debt at a price that makes sense, after all that's where the jobs and the "real" green shoots will come from.

And now that the great "industry" of suckering US homeowners into unsustainable debt, packaging up financial instruments built on that and selling "the product" around the world has proven to be about as robust long-term as the industry of producing Melanin-tainted milk, it's hard to see the financial sector creating many new jobs, regardless of how much money the government throws at it.

Which makes one wonder, why is the government throwing money at an industry that was (apparently) great once but has now failed and will probably never be the same, and starving the industries that have traditionally been what makes America tick.

That reminds me of the Brits attempting to prop up their ship-building industry long after its time had passed, or its unions had destroyed it (same difference). Perhaps it's time to let some big banks die, and focus on helping out what it was that made America work in the first place?

Like ordinary workers and the (private sector) enterprises that employ them, rather than the state-owned fat-cats on Wall Street.

Notes:

1There are basically two ways to value an income-generating asset like a stock, either (a) what "the market" will pay (today) or (b) the present value of future cash flows, which depends on the discount rate you use, and that depends on long-term-interest-rates (LTIR).

(The "third" way to do a valuation is depreciated replacement costs which is the time-adjusted cost of re-creating the asset; this is generally not practicable to work out for a stock (although some people try)).

Of course there are drawbacks with both approaches (1) it is well known that markets can sometimes misprice assets quite badly (examples include the sub-prime, toxic assets, Dot.com, 1929, Tulips...etc), and (2) you don't know for sure what the future revenues will be, so you could be completely wrong about that too.

What that means is, as George Soros explained so eloquently in a recent interview on Bloomberg, in the end you make a guess. The gyrations of stock market prices are the random walk of collective guesses.

2If an idiot (or crooked) banker lends $100 to someone who has no intention of paying it back (and then books the fees and the spread on the interest that is paid in the first few years as "profit" and pays himself a huge bonus for his "divine genius"), and then in three or four years time the penny drops that the principle won't get paid back and that the collateral underwriting the loan is worthless... when did he actually lose the money?

According to current accountancy rules, he lost it when he realized it wasn't going to be paid back, but the reality is that he lost it when he handed the $100 over.