子夜讀書心筆

寫日記的另一層妙用,就是一天辛苦下來,夜深人靜,借境調心,景與心會。有了這種時時靜悟的簡靜心態, 才有了對生活的敬重。

A constant theme for any value investor is "price always meets value". They just do. It is the "when" that we cannot predict but we know eventually it does. For that reason we buy when the value is above the current price and sell when it reaches or exceeds it. Easy, right? Well, not really, it is the determination of what that value is that trips folks up and causes mistakes.

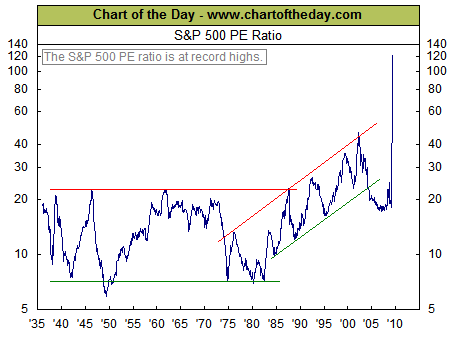

Thus is the dilemma of the current market. By any valuation it is way overvalued. The S&P 500 last Friday (5/15) after another quarter of reduced earnings (most are in now) sat at an stratospheric 122 times earnings. For those who are not sure what "normal" is, it is about 20 times earnings.

Here is the whole thing visually: So, that must mean the market is headed for a big fall, right? Well, there are two parts to the equation. The "P" or price and the "E", earnings. In order to get the ratio down to a normal level, the "P" must fall and the "E" must rise. Q1 earnings numbers were smacked by a -6% Q1 GDP. We know Q2 will be better and Q3 ought to show even more improvement (both may still be negative but less so). That means we can expect the "E" part of the equation to increase.

So, that must mean the market is headed for a big fall, right? Well, there are two parts to the equation. The "P" or price and the "E", earnings. In order to get the ratio down to a normal level, the "P" must fall and the "E" must rise. Q1 earnings numbers were smacked by a -6% Q1 GDP. We know Q2 will be better and Q3 ought to show even more improvement (both may still be negative but less so). That means we can expect the "E" part of the equation to increase.

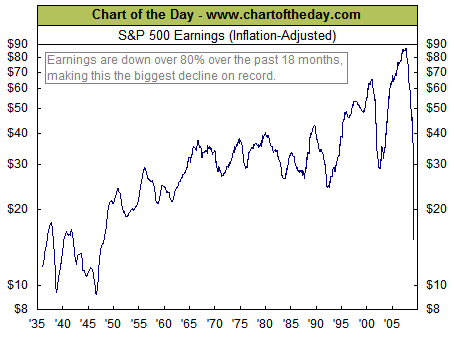

With S&P earnings as of last Friday at $7.21, it will not take much improvement for the PE ratio of the market to be brought down by even a modest earnings improvement. For reference, last year at this time the S&P had earnings of $62 and sat at 1400 vs. 888 today. For the market to sit where it is and have its PE fall to around a more "normal" 20 times earnings, they must increase 485% to $45.

Again, visually, this is what has happened to earnings:

So, what happened to Q1? Companies wrote off billions in Q1 and used it as a "kitchen sink" quarter. We all expected it to be bad so they wrote down everything that had or might deteriorate in value. Q2 ought to show improvement if for no other reason, the massive Q1 write-downs ought to be just about over. Even if operating earnings stay flat, we will see overall earnings improve.

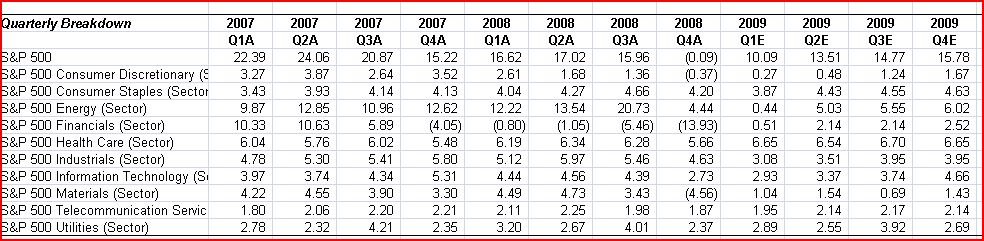

Again, visually (click to enlarge): This is the S&P operating earnings.

Notice Q4 was the worst operationally and improvement is expect through the year. This is what to watch going forward. As long as this continues upward, the rest will wash out in the end.

It is fairly safe to say that the decline in earnings is over, or nearly over and we ought to begin to see improvement. Note: this does not mean the overall economy improves immediately or dramatically, just that the decimation in earnings is done. Because of that, there is a very real scenario where the market just pauses and waits for earnings to catch up. Then, depending on the Q2 results as they come in, the next move in the market is defined. If they are as expected or better than expected, the market will feel justified at its current level. Should they begin to come in worse, the high levels it currently sits at will indeed appear irrational and we could see a decent sized sell off.

Please be aware that I am not predicting what the market is going to do over the next two months, none of us know that. What I do know is that the current PE of the market is unsustainable and has to come down to more normal levels. The only way for that to happen is a rapid rise in earnings and / or a fall from the current levels of the S&P.

It also means the risk to current levels is downward. If we do not get increasing earnings, the market has to fall to regain valuation balance. If we do get modestly increasing earnings, it could sit here while the earnings take down the valuation disparity. Either way, the markets upside is limited to down.

One then has to extrapolate from this that the market could continue its upward march if we get a large increase in earnings in Q2. That would justify the

recovery theme currently "en vogue" and reduce the market valuation in one step. All eyes then turn to continued improvement in Q3 for continued market appreciation.

In talking with one of my readers about the subject yesterday he said:

That is the way it happens. Markets that move ahead of earnings are always called “speculative”. It is a question that value players would answer that they buy on P/Assets or P/BV but sell on earnings expectation or P/E when the earnings come in.

A quote from Ian Cumming from the Leucadia (LUK) annual meeting I went to. “The science is in the “In”. The poetry is in the “Out”. The value buyer assesses the potential earnings power of the assets, but buys when there are no or at least very low earnings and the market not having the sense to do the same type of work is lost in the pricing and giving stocks away. But, when the earnings are at full potential and have recovered, the market believes that some new earnings trend has begun and priced the stock at “poetry levels”-“so beautiful” and it is this is where one should sell.

So what to do? Be careful. Something has to happen either way and two of the three scenarios have the market doing nothing to falling.