通脹背後企業利潤創曆史新高

https://cupe.ca/record-high-corporate-profits-behind-inflation

2022 年 12 月 8 日

關於企業利潤的公眾爭論越來越多——多少算太多? 在大流行期間,大企業取得了創紀錄的收益,而家庭和小型企業則陷入困境。 隨著通貨膨脹的加劇,企業的逐利行為導致了物價的上漲。

加拿大央行基本上忽視了企業在製定價格方麵所發揮的作用。 相反,它繼續暗示提高工資將導致物價上漲(工資-物價螺旋式上升)。 例如,10月份央行加息時,9次提到工資,卻根本沒有提到企業利潤。

這種做法是不誠實的。 我們可以看到,平均工資漲幅全麵低於通脹,而企業利潤卻在增長。

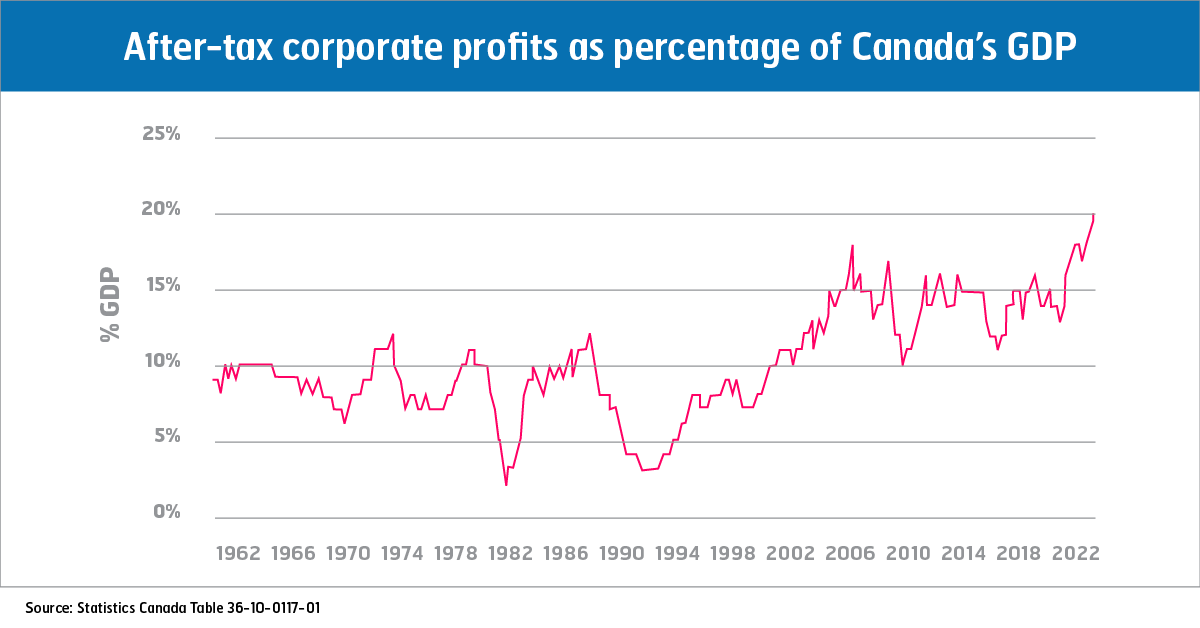

事實上,作為加拿大國內生產總值(GDP)的一部分,企業稅後利潤已達到60年來的最高水平。 GDP 是一個國家在特定時期內製造的所有製成品和服務的貨幣價值。 它通常用於估計經濟規模。 2022年第二季度(4月、5月和6月),企業稅後利潤占加拿大GDP的20%。 這比 2005 年金融危機前 18% 的高點高出兩個百分點,是 1960 年至 2000 年間平均水平的兩倍多。

為什麽加拿大央行忽視企業利潤在物價上漲中的作用? 原因之一是主流經濟理論認為,企業自然會設定盡可能高的價格以實現利潤最大化。 這個想法是,如果企業將價格定得太高,消費者就會轉向更實惠的選擇,從而控製價格。

問題是,這隻有在市場存在良性競爭的情況下才有效,並且新企業可以通過以較低價格提供商品和服務來賺錢。 這在加拿大很困難,因為我們的法律有利於公司合並和壟斷,使新企業更難競爭。

反競爭行為在加拿大並不新鮮,我們對此的擔憂也不是新鮮事。 過去幾年,公眾對一些大型企業合並表示強烈抗議,聯邦政府剛剛於 11 月啟動了期待已久的競爭審查。 在整個過程中,我們需要讓政府承擔責任,以改進我們的競爭法並控製價格。

雖然競爭法的改進會有所幫助,但這並不是全部。 加拿大的一些行業也有多家參與者,例如加拿大的大銀行,它們在競爭激烈的市場中維持的價格高於我們的預期。 這表明競爭並不是經濟學家有時認為的神奇解決方案,尤其是在涉及住房、食物和能源等必需品和服務時。 企業知道消費者會為他們需要的東西支付更多的錢,即使他們真的買不起。 對於真正的必需品,有一個公共選擇是有意義的,這樣可以消除暴利——就像公共能源公司一樣。

最後,值得注意的是,提高企業稅後利潤的主要驅動力之一是聯邦和省級政府自 2000 年以來實施的大幅企業減稅。這導致財富從 政府和公共服務落入私人手中。 我們需要我們的政府認識到這種滴入式方法已經失敗,並在企業稅收方麵實現更好的平衡。

Record-high corporate profits behind inflation

https://cupe.ca/record-high-corporate-profits-behind-inflation

The Bank of Canada has mostly ignored the role that corporations play in setting prices. Instead, it has continued to suggest that raising wages will lead to higher prices (a wage-price spiral). For example, when the Bank increased interest rates in October, they mentioned wages 9 times, and failed to mention corporate profits at all.

Such an approach is disingenuous. We can see that average wage increases are lower than inflation across the board, while corporate profits are increasing.

In fact, as a share of Canada’s gross domestic product (GDP), after-tax corporate profits have reached a 60-year high. GDP is the monetary value of all finished goods and services made within a country during a given period. It’s often used to estimate the size of an economy. In the second quarter of 2022 (the months of April, May, and June), after-tax corporate profits accounted for 20% of Canada’s GDP. This is two percentage points higher than the pre-financial crisis high of 18% that we saw in 2005, and more than double the average we saw between 1960 and 2000.

Why is the Bank of Canada ignoring the role of corporate profits in rising prices? One reason is that mainstream economic theory says it’s natural for corporations to set prices as high as they can to maximize profits. The idea is that if corporations set prices too high, consumers will switch to a more affordable option, keeping prices in check.

The problem is that this only works if there is healthy competition in the market, and new businesses can make money by offering goods and services at lower prices. This is difficult in Canada because our laws favour corporate mergers and monopolies, making it harder for new businesses to compete.

Anti-competitive behaviour isn’t new in Canada, and neither are our concerns about it. There’s been public outcry over a number of large corporate mergers in the past several years, and the federal government just launched a long-awaited competition review in November. Throughout this process, we will need to hold the government to account to improve our competition laws and keep prices in check.

But while improvements to competition law will help, it’s not the whole picture. There are also Canadian industries with several players, such as Canada’s big banks, which maintain higher prices than we would expect in a competitive marketplace. This demonstrates that competition isn’t the magic fix that economists sometimes make it out to be – especially when it comes to goods and services that are necessities, like shelter, food, and energy. Corporations know that consumers will pay more for things that they need, even if they really can’t afford it. For true necessities, it makes sense to have a public option that takes profiteering out of the equation – like public energy companies.

Finally, it’s important to note that one of the primary drivers of higher after-tax corporate profits has been the dramatic corporate tax cuts that governments at both the federal and provincial levels have implemented since 2000. This has resulted in a huge transfer of wealth from governments and public services into private hands. We need our governments to recognize that this trickle-down approach has failed, and to implement a better balance in corporate taxation.