笨狼發牢騷

發發牢騷,解解悶,消消愁

正文

《美國大眾電視台》美國是世界電子垃圾最大的傾倒者

喬姆斯基

Chomsky & Krauss: An Origins Project Dialogue

上

下

Noam Chomsky and Marvin Minsky on the History of Artificial Intelligence

http://www.marketwatch.com/story/some-66-million-americans-have-zero-emergency-savings-2016-06-21

美國社會的權力結構

擁槍的權力,後果和現狀

入獄率,警察和獄監工會的勢力

申辯的權力和現實,金錢與平等的關係;律師協會的勢力

禁毒和種族:兩大淵源;嚴打和憐憫;執法與和諧

《HuffPost》The Vultures’ Vultures: How A New Hedge-Fund Strategy Is Corrupting Washington

Shapiro, it turns out, is but one foot soldier in the hedge fund infantry

Shapiro, it turns out, is but one foot soldier in the hedge fund infantry

“權威人士”是誰?

《華爾街見聞》

一年內刷了三次屏 “權威人士”究竟是誰?

《第一財經與阿裏巴巴旗下的DT財經》

“權威人士”又發話了,黨報署名到底有何玄機?

《環球老虎》

經濟是“L”型,但股市是“”型

《德國之聲》

5月9日,人民日報再次刊登由“權威人士”對中國經濟的采訪。前兩次“權威人士”接受采訪之後,A股都進入了調整,這次“似乎”也不例外。那麽這位“權威人士”究竟是什麽來曆?

"權威人士"再現身 中國鐵心"去杠杆"?

《北京電視台》

媒體揭秘:被人民日報刷屏"權威人士"是誰

《曉帆專欄》權威人士到底是誰?能當反向指標麽?

“權威人士平時喜歡吃慶豐包子鋪的包子”,嗬嗬,習近平,跟我一個想法

《人民日報》

開局首季問大勢——權威人士談當前中國經濟

本報記者 龔雯 許誌峰 吳秋餘

一年內刷了三次屏 “權威人士”究竟是誰?

《第一財經與阿裏巴巴旗下的DT財經》

“權威人士”又發話了,黨報署名到底有何玄機?

《環球老虎》

經濟是“L”型,但股市是“”型

《德國之聲》

5月9日,人民日報再次刊登由“權威人士”對中國經濟的采訪。前兩次“權威人士”接受采訪之後,A股都進入了調整,這次“似乎”也不例外。那麽這位“權威人士”究竟是什麽來曆?

"權威人士"再現身 中國鐵心"去杠杆"?

《北京電視台》

媒體揭秘:被人民日報刷屏"權威人士"是誰

《曉帆專欄》權威人士到底是誰?能當反向指標麽?

“權威人士平時喜歡吃慶豐包子鋪的包子”,嗬嗬,習近平,跟我一個想法

《人民日報》

開局首季問大勢——權威人士談當前中國經濟

本報記者 龔雯 許誌峰 吳秋餘

解讀(華爾街見聞):

最全解讀:關於權威人士的談話 你隻需要明白這七點

權威人士解讀“股市、匯市、樓市”政策取向:不能加杠杆硬推經濟增長

管清友解讀“權威人士談話”:股市匯市樓市各歸其位

最全解讀:關於權威人士的談話 你隻需要明白這七點

1、確認經濟L型,供給側改革回歸政策重心

2、反對高杠杆硬推經濟

3、嚴防金融高杠杆

4、股市匯市漲跌不再是政策目標

5、否定用房地產加杠杆來去庫存

6、強調預期管理

7、去產能:保人不保企

權威人士解讀“股市、匯市、樓市”政策取向:不能加杠杆硬推經濟增長

管清友解讀“權威人士談話”:股市匯市樓市各歸其位

最全解讀:關於權威人士的談話 你隻需要明白這七點

1、確認經濟L型,供給側改革回歸政策重心

2、反對高杠杆硬推經濟

3、嚴防金融高杠杆

4、股市匯市漲跌不再是政策目標

5、否定用房地產加杠杆來去庫存

6、強調預期管理

7、去產能:保人不保企

1,“新動力還挑不起大梁。”

2,資源大省要丟掉幻想,不要做夢

3,政策“重點、節奏、力度”出了問題,方向沒有問題

4,一季度增長付出了很大代價

5,行政手段還是要用

6,對問題不能視而不見,甚至文過飾非,否則會挫傷信心、破壞預期。

7,密切關注價格變化。

2,資源大省要丟掉幻想,不要做夢

3,政策“重點、節奏、力度”出了問題,方向沒有問題

4,一季度增長付出了很大代價

5,行政手段還是要用

6,對問題不能視而不見,甚至文過飾非,否則會挫傷信心、破壞預期。

7,密切關注價格變化。

第一, 專訪代表著中央高層對於經濟形勢的權威定調。

第二, 為什麽專訪大段強調 L 型?因為 L 型意味著刺激一沒空間,二沒必要。

第三, 專訪將目前企穩界定為“老辦法”,這意味著當前引擎不可持續,還是要回歸結構調整,供給側改革還是要挑大梁。

第四, 通脹還是通縮也不要爭了,專訪認為目前難以定論; 但對於貨幣寬鬆的幻想,專訪明確標了休止符。

第五,專訪將應對經濟下行壓力和避免實體高杠杆界定為“兩難”,且暗示如果不可兼得,那麽要選擇後者。

第六, 八大風險點+高杠杆是原罪,後續可能會有一係列排雷措施。

第七, 明確否定樓市“通過加杠杆去庫存”的做法,如果後續經濟能繼續企穩,樓市政策可能會進一步收緊。

第八, 市場可能部分誤讀了“429”政治局會議,關於股市提法的大背景是各回各位。

第二, 為什麽專訪大段強調 L 型?因為 L 型意味著刺激一沒空間,二沒必要。

第三, 專訪將目前企穩界定為“老辦法”,這意味著當前引擎不可持續,還是要回歸結構調整,供給側改革還是要挑大梁。

第四, 通脹還是通縮也不要爭了,專訪認為目前難以定論; 但對於貨幣寬鬆的幻想,專訪明確標了休止符。

第五,專訪將應對經濟下行壓力和避免實體高杠杆界定為“兩難”,且暗示如果不可兼得,那麽要選擇後者。

第六, 八大風險點+高杠杆是原罪,後續可能會有一係列排雷措施。

第七, 明確否定樓市“通過加杠杆去庫存”的做法,如果後續經濟能繼續企穩,樓市政策可能會進一步收緊。

第八, 市場可能部分誤讀了“429”政治局會議,關於股市提法的大背景是各回各位。

《南華早報》誰是人民日報的權威人士?

“在許多方麵,該人士的意見都與李克強總理領導下的國務院政策相違,對許多中國官員此前發表的意見也進行了反駁”,這內幕,

“在許多方麵,該人士的意見都與李克強總理領導下的國務院政策相違,對許多中國官員此前發表的意見也進行了反駁”,這內幕,

【法廣RFI】

“昨天,本台記者從熟悉北京政情人士得知,此文是習近平辦公室和中央財經領導小組辦公室共同撰寫,代表了中南海南院(黨中央)觀點。”

《多維綜合》反駁李克強 中共黨報的權威人士是他?

“國家主席習近平的首席經濟智囊劉鶴或符合“權威人士"身份。劉鶴現為中共中央財經領導小組辦公室主任,也是發改委副主任。”

《彭博》

China's 'Authoritative' Warning on Debt: People's Daily Excerpts

Even China's Party Mouthpiece Is Warning About Debt

China's Anonymous Economic Oracle Signals Shift From Debt

Even China's Party Mouthpiece Is Warning About Debt

China's Anonymous Economic Oracle Signals Shift From Debt

中金在線: “謀殺”A股的真凶找到了!原來是“他”↓

《英國衛報》Offshore finance: more than $12tn siphoned out of emerging countries

《獸色日報Daily Beast》How the Kleptocrats’ $12 Trillion Heist Helps Keep Most of the World Impoverished

作者網博:More than $12 trillion stuffed offshore, from developing countries alone

《獸色日報Daily Beast》How the Kleptocrats’ $12 Trillion Heist Helps Keep Most of the World Impoverished

作者網博:More than $12 trillion stuffed offshore, from developing countries alone

美國就業

《華爾街日報》

美國小業主行會叫NFIB(National Federation of Small Business)

《聯儲論文》

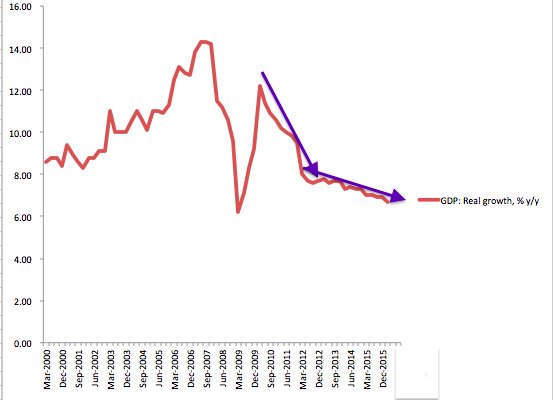

《環球老虎》2015.11.23

2016全球經濟投資報告

本報告中參照IMF、OECD、WB等機構年度展望報告的行文範式,以國別來分章節,對資本市場最為關注的經濟和政策變量進行分析,並以專欄形式對若幹比較有意思的話題進行單獨探討。涉及到的關鍵點包括:經濟增長、投資、消費、貿易、通脹、大宗商品、貨幣政策與貨幣政策8個方麵。既包括2015年全球經濟的全景式回顧,也包括2016年全球經濟的前瞻。

本報告中參照IMF、OECD、WB等機構年度展望報告的行文範式,以國別來分章節,對資本市場最為關注的經濟和政策變量進行分析,並以專欄形式對若幹比較有意思的話題進行單獨探討。涉及到的關鍵點包括:經濟增長、投資、消費、貿易、通脹、大宗商品、貨幣政策與貨幣政策8個方麵。既包括2015年全球經濟的全景式回顧,也包括2016年全球經濟的前瞻。

難怪“權威人士”要出來清場

普通人的理財越來越活躍,以前較為激進的半年期保本理財產品(年化6%)現在已經是最低配置了,連大媽都不存定期了。過去非法的地下錢莊,如今搖身一變成了P2P網絡基金,往往給出三個月年化率12%的產品更凶惡的有三個月15%+的,雖然誰都知道有風險,但是80後們趨之若鶩,利滾利真的很爽。當然這次股災後兩三個月,估計有人會哭昏在廁所。再往上就是基金和股市,各個銀行網點每天的基金理財業務比窗口現金業務火爆的多,我辦個網銀簽個手續1個小時,見到三個大媽和經理研究股指期貨的衍生品,最少的一個投了30萬。普通股民裏麵,敢用杠杆的越來越多,所以這回跳樓的多。但是現在,大家的思路就是大賭大贏。股票再往上一級,就是合作投資,適用於有幾十萬閑錢的家庭,一人牽頭幾家入股,各種兒童項目,老人項目是投資最火的領域,在大城市裏收益很穩定。

番外帶一句,江浙小城市或農村地區的人膽子更大,做生意的無論大小都是一身的三角債,而且是相對於他們本身十分驚人的數額。給外人的感覺是一旦一人資金斷鏈幾十人都得遭殃,然而他們本地人的邏輯是如果掛不進這跟鏈條,莫說是喝湯就連骨頭渣滓都沒機會揀。

肯定有人會問,實體經濟這麽不景氣,國人到底怎麽支撐諸如就業,收入,消費這樣的問題,答案就是創業!一股國家意誌的創業潮。李克強經濟學的標簽。思路就是,既然無法解決就業市場崗位嚴重不足的矛盾,就把大學生和年輕人推向創業,讓社會去吸納他們,然後你敗了你認栽。到處都是孵化器,甚至每所大學幾乎都有自己的孵化器,融資可大可小,門檻越來越低,好一點的項目不愁天使投資人,極普通的項目拿下幾百萬的也不在話下,而那些看起來讓人覺得無厘頭的垃圾項目也可以簡簡單單從那些P2P裏搞來高利貸,甚至都不用實名抵押。反正就是有錢,真有錢,不知道從哪來的這麽多錢。舉個例子,什麽叫‘好項目’,某腫瘤醫院院長的孫子大學畢業了,和幾個同學合夥搞個app,用他爺爺的內部關係來給病患排隊掛號,這個公司隨便就能找人融資個百萬,然後沒幾天被阿裏健康用翻倍的價格收走。一個中等項目,幾個平頭百姓畢業生,找幾家小飯館,開發個app給人送外賣,也就成功創業了,過不了幾天那個幾十萬的融資,也足夠他們自行車換電驢再開個小門麵的了。北美華人看了估計直接氣吐血。當然很多人認為這樣早晚會出事,將來會有問題,但是將來是將來,關鍵是今天拿到錢,用溫家寶的名言就是我們相信下一代領導集體的智慧。

最後說說股市,A股從上半年的人氣爆棚,到過去兩周的股災,其實是各種社會問題的縮影。為什麽這次國家得救市,因為不救真的可能出事。實體經濟已經完蛋操了,房地產除了北京深圳回光返照,再吹泡泡就是徹底的sb,依托IT的創業風潮,雖然能解決一些問題,但是還有大量其他行業的人擠不進去,而這些人目前維持就是靠理財,p2p和眾籌投資,這三個管道不管是哪個都是打著激活民間資本鼓勵創業和資金利用率的旗號來招搖的,但是最後都有相當的比例還是流進股市,因為這是唯一的快錢渠道。更差的則是連環旁氏。A股這樣的暴法,三四個月後隱性的民間借貸危機就會爆發,今天哪怕沒有在股市損失,幾個月後自己投在p2p上的也可能血本無歸。習李王這次絕壁是被玩了,而且前期的被動反應全是昏招。這回不用真金白銀老老實實的托盤5天,過後矛盾一旦爆發很難收場。為什麽會有今天?就是所謂的反腐,四風,始終沒敢燒到銀行業,金融業和保險業。這些大Boss沒打才要命。再舉實例,天津市商務委過去一年三個正處級出事被免職交法辦,最高的涉案金額才30萬,最少的一個倒黴蛋3萬塊丟了官。而一個普通城市銀行支行的行長一年自己造成個1億壞賬跟玩一樣。但是至今金融係統的人仍然在以不可思議的方式作。(黃昏網友轉載網傳)

不知習李能不能睡著覺?

股手凱維埃爾

熱羅姆·凱維埃爾(Jérôme Kerviel)是法興銀行(Société Générale)的一名普通股市抄手。然而他卻導致法興大虧€4.9 billion($73 billion)。這是他的故事。

This is how the world’s most “successful” rogue trader operated

《紐約時報》Kerviel: Bosses Never Said a Thing

熱羅姆·凱維埃爾(Jérôme Kerviel)是法興銀行(Société Générale)的一名普通股市抄手。然而他卻導致法興大虧€4.9 billion($73 billion)。這是他的故事。

This is how the world’s most “successful” rogue trader operated

《紐約時報》Kerviel: Bosses Never Said a Thing

【金融時報】

US tax havens: The new Switzerland

Kara Scannell and Vanessa Houlder

The US is a magnet for offshore wealth, notably South Dakota, which has guaranteed secrecy for family trusts

US tax havens: The new Switzerland

Kara Scannell and Vanessa Houlder

The US is a magnet for offshore wealth, notably South Dakota, which has guaranteed secrecy for family trusts

In an old discount store hugging a corner in downtown Sioux Falls, South Dakota, the heirs to the William Wrigley chewing gum fortune have an office for their family trust. So do the Carlson family, owners of the Radisson hotel chain, and the family of John Nash, the late hedge fund giant.

They are among the 40 trust companies sharing an address at 201 South Phillips Avenue, a modest, two-storey white-brick building. Inside, $80bn worth of trust assets are administered.

South Dakota is best known for its vast stretches of flat land and the Mount Rushmore monument, where the heads of four presidents are carved into the Black Hill Mountains. Its population of 858,469 ranks 46th in the country. Locals joke that it has more pheasants — about 1.5m — than people.

Yet despite its small town feel, Sioux Falls has become a magnet for the ultra-wealthy who set up trusts to protect their fortunes from taxes and future ex-spouses. Assets held in South Dakotan trusts have grown from $32.8bn in 2006 to more than $226bn in 2014, according to the state’s division of banking. The number of trust companies has jumped from 20 in 2006 to 86 this year.

The state’s role as a prairie tax haven has gained unwanted attention since the release of the Panama Papers, an investigation by the International Consortium of Investigative Journalists. The leak of more than 11m documents from a Panamanian law firm — some of which will be put on to a public database today — has drawn attention to the anonymity that is available in the US.

After years of threatening Swiss and other foreign banks that helped Americans hide their money, the US stands accused of providing similar services for the rest of the world. “America is the new Switzerland,” says David Wilson, partner of Schellenberg Wittmer, a Swiss law firm. “In the industry we have known this for several years.”

The US has a long history of attracting funds from undisclosed foreign sources. In 2011, The Florida Bankers Association told Congress there were hundreds of billions of foreign deposits in US banks because “for more than 90 years the US government has encouraged foreigners to put their money in US banks by exempting these deposits from taxes and reporting”.

The Boston Consulting Group estimates that there is $800bn of offshore wealth in the US, nearly half of which comes from Latin America. That puts it well behind Switzerland’s $2.7tn, but it is expected to grow at nearly 6 per cent a year — faster than any rival except Hong Kong and Singapore.

Bruce Zagaris, a Washington-based lawyer at Berliner, Corcoran & Rowe, says the US offshore industry is even bigger than people realise. “I think the US is already the world’s largest offshore centre. It has done a real good job disabling competition from Swiss banks.”

The growth has been fuelled by international disclosure rules introduced in 2014 to crack down on tax havens — and adopted almost everywhere except the US, which had introduced its own regulations. But these rules have gaps that preserved the advantages of trusts such as the ones on offer in South Dakota. Rules proposed by the White House last week to force companies to disclose more information about their owners are unlikely to erode those advantages.

Trusts are able to avoid scrutiny under both US and international rules as long as the owner appoints a local trustee and a foreign “protector” to direct the trustees. South Dakotan companies actively promote the secrecy offered by opening a trust in the state.

“Many of the offshore jurisdictions are becoming less appealing for international families looking for secrecy”, says the website of the South Dakota Trust Company, one of the most prominent. “Consequently, the stability of the US combined with its modern trust laws . . . may be more appealing to many international families than an offshore trust based in a less powerful country.”

Trust leader

Even before the flurry of international interest, South Dakota’s trust industry was booming. With no personal or corporate income tax, no limit on “dynasty trusts” and strong asset protection laws — shielding assets from soon-to-be ex-spouses — South Dakota has leapt to the top of annual rankings for the trust industry. Nevada, Delaware and Alaska also compete for accounts.

South Dakota’s inviting legal environment can be traced to the ground floor of the old discount store on Phillips Avenue. Upstairs is the corner office of Pierce McDowell III, the man largely responsible for the state’s renaissance.

Mr McDowell is 58 with a mop of curly hair and a knack for storytelling. (His grandfather, Pierce, whom the family refers to as “P1”, was working at a small South Dakota bank when it was stuck up by John Dillinger’s gang during their crime spree in the 1930s.) He cycles to his office on a fat-tyred bike, even in the snow, when he isn’t flying to New York or California to see clients and advisers.

The SDTC president stresses the importance of relationships to his business’s success and says the families he serves want to protect future generations — not avoid paying taxes.

Mr McDowell has been an evangelist for South Dakota for almost 25 years. In 1993 he wrote an article for Trusts and Estates magazine. In South Dakota, he said, families could employ “the same strategy used by the Rockefellers and the Vanderbilts for generations to avoid estate tax”.

The article caught the eye of Al King, then director of Citibank’s trust division in New York, and he recruited Mr McDowell to run the bank’s South Dakota office. The combination of Mr King’s legal contacts and Mr McDowell’s local knowledge catapulted the business. In 2002 the pair struck out on their own, forming SDTC with Mr McDowell in Sioux Falls and Mr King in New York.

The firm does not manage money. They help private trusts meet state requirements, such as having someone in the state serve as a director, establishing office space and carrying out administrative work within state lines. Trust companies are required to have two board meetings a year in the state. Annual fees start at $35,000 “on the low end” and go up.

Aspects of the trust industry attracted criticism. States like New York complained about the loss of billions of dollars in business to trust-friendly states as well as the leakage of income tax, which it estimated at $150m in 2013.

Lawrence Waggoner, a law professor at the University of Michigan, condemns the dynasty trusts pioneered by states like South Dakota as a “folly”. He argues that over time they would be riven by disputes and very difficult to manage. After a few hundred years there would be tens of thousands of beneficiaries. Arranging a meeting would be impossible: even the Rose Bowl football stadium in California would not be large enough to hold them all.

Some analysts question whether the state receives enough from the benefits it provides. In the 2015 fiscal year, South Dakota collected $1.79m from trust companies. The legislature passed a $4.3bn state budget last year.

Bernie Hunhoff, a Democratic state senator, has proposed imposing a corporate income tax. “We’ve had a lot of trust legislation and a lot of money is moving into South Dakota and they’re benefiting from our tax law,” he says. “That’s one reason I thought we needed a corporate income tax.”

Taking advantage

Andy Holmes relocated from Kansas City last year to help his firm, the Great Plains Trust Company, increase its presence in South Dakota after clients, including celebrities and famous athletes, asked about the state’s benefits.

Great Plains worked with SDTC to learn the ropes, but last year leased a windowless office in a brick and glass building for its two employees. Down the hall is Maroon Trust, which manages the money of Chicago’s Pritzker family. Elsewhere on the floor is a roofing company. They share a receptionist.

Mr Holmes estimates that 90 per cent of the registered trusts in the state “are what I call shell companies where you basically have a PO box or an office and somebody will come here twice a year to have board meetings and meet regulatory requirements. But there’s nobody here with feet on the ground to serve Sioux Falls. We’re trying to take advantage of that.”

For now, the biggest challenge for the industry, Mr McDowell says, is criticism of the secrecy it can offer. “So much that has been written about this stuff appears to be so sinister,” he says. “All of these tax laws are there for a reason. It’s not about tax dodging, it’s planning.”

Bret Afdahl, director of the state’s banking division, says the requirements to qualify for a trust have increased, such as having more of a physical presence. Applicants are often turned away. “We’re the chartering authority so if we approve it and something goes wrong we own it,” he says. “From a reputational standpoint no one benefits from having something bad happen.”

There are legitimate reasons to seek secrecy, according to Roderick Balfour, founder of Virtus, a Guernsey-based trust company that opened in South Dakota in 2009. He says people have a right to privacy, especially if corruption in their home countries means their data would not be secure. Concerns are overblown, he says: “America is never going to be a Panama.”

France and other countries have introduced tough disclosure rules on trusts. In many others there are suspicions that trusts are illegally used to evade tax. Gabriel Zucman, a French economist, estimates that governments lose at least $200bn a year in evaded taxes from the $7.6tn of the world’s financial wealth that is held offshore.

The respite from new reporting rules gained by moving to the US could prove temporary. On Thursday the White House called on Congress to act on “long overdue” proposals to ensure the US is in line with international standards. This Thursday, David Cameron, the British prime minister, is hosting a summit where world leaders will be asked to sign a global declaration promising to expose corruption.

There might be big risks in using the US to hide money for illegitimate reasons. Mr Wilson likens it to “sitting in the dragon’s mouth”. One law firm that used to promote the benefits of “hiding in plain sight” says its clients are now convinced the US will adopt international standards and do not wish to be “tarnished by association”.

The appeal of moving structures to the US is that it buys time, says Peter Cotorceanu, counsel for Anaford, a Zurich law firm. Any change in US law would depend on the Republicans losing control of the House, he says. He predicts that hundreds of billions of dollars will move to the US. “Most of the money will move this year”, he says, noting that individuals in Switzerland, Hong Kong and Singapore have until the end of the year to “yank their money out”.

In South Dakota, there is a mixed reaction to the trust industry’s appeal to foreigners. “In a world where it’s very hard to hide ownership or hide assets sometimes the easiest place [is one] no one would normally think of, which is the US,” says Christopher Holtby, co-founder of the Wealth Advisors Trust Company, in Pierre, the state capital.

Since establishing an office in South Dakota in 2009, he has seen signs of change. In 2014 Trident, a Swiss trust company, opened an office in Sioux Falls, he notes. “Why is an international firm setting up in South Dakota?,” says Mr Holtby. “I don’t like that international lawyers want to come to South Dakota. Generally international lawyers never bring anything that’s simple.

“And we like simple.”

裴惕斯《華爾街日報》專欄

Michael Pettis

Given its surplus economy, a weak currency could undermine growth and incite a trade war

China’s central-bank governor, Zhou Xiaochuan, consistently denies that the country can devalue its way to faster growth, arguing that a falling yuan would harm the economy. From a purely economic point of view, Mr. Zhou is right. But that hasn’t stopped a growing number of analysts from calling for a substantially weaker currency.

The arguments in favor of devaluation are straightforward. China’s economy is slowing sharply, in part because of declining exports. After many years of current- and capital-account surpluses, the past two years have seen a large balance-of-payments deficit, and China’s central bank had to intervene heavily to support the yuan.

Developing economies usually respond in such situations by devaluing their currencies. Supporters of devaluation claim that China should do the same to regain export competitiveness and reverse capital outflows.

This comparison is mistaken. China is the world’s second-largest economy and runs the second-largest trade surplus in history. Developing economies that devalued successfully were much smaller, which made it easier for the world to absorb their export surge. They also devalued only after their overvalued currencies had caused persistently large deficits.

In contrast, the yuan is not overvalued. In fact it is undervalued, as Governor Zhou all but acknowledged in an interview with China’s financial magazine Caixin three months ago.

The current account shows why: China enjoys low unemployment and brisk wage growth. Economic activity is growing 6% to 7% while debt is growing two to three times faster. China’s trade partners, on the other hand, suffer high unemployment and can barely eke out 1% or 2% growth.

Normally China would import far more than it exports. But rather than running large deficits, China has large surpluses. While its exports declined last year, global exports declined even more. China is gaining export market share and its trade surplus is growing, neither of which suggests an overvalued currency.

To keep the yuan from falling the central bank has spent about $1 trillion of its $4 trillion in reserves. But China’s shrinking reserves are driven by net capital outflows. If money went abroad mainly because Chinese investors think foreign assets are relatively cheap, a weaker yuan would reduce capital leaving China by making foreign assets more expensive. But this isn’t the reason for the capital outflows.

Money leaves China partly to buy strategic assets, partly to hedge against rising political and financial uncertainty, and partly to reverse the notorious “arbitrage” of earlier years. From 2012 to 2014, some $1 trillion poured into China to speculate on an appreciating, higher-yielding yuan.

Chinese investors don’t care about the relative value of the yuan. Rather than restrain them, a devalued yuan might actually speed up their exit. This is what happened immediately after the change in the currency regime in August. Capital restrictions had to be tightened significantly to prevent even more money from leaving.

The main reason to oppose devaluation is that rather than boost growth, a weaker currency makes a surplus economy more precarious. Instead of changing relative prices, devaluation shifts income from consumption to savings.

In deficit countries—where savings are insufficient to fund investment—slowing growth scares off foreign inflows, causing investment to decline, which slows the economy further. By redirecting income from consumption toward savings, devaluation reduces dependence on foreign capital and keeps investment from dropping.

Surplus countries, however, don’t suffer from insufficient savings, and China’s savings are excessive. Yuan devaluation would simply reduce already-low domestic consumption and increase China’s reliance on investment and exports. This happened in Japan, where a substantially weaker yen further diminished consumption without kick-starting growth. For surplus countries, devaluation replaces sustainable demand—namely consumption—with the unsustainable demand of investment and trade surpluses.

In a global economy with growing trade tensions and weak demand, a devaluation that substantially boosts China’s trade surplus may ignite a trade war. If weak currencies only benefit much smaller economies with overvalued currencies and large current account deficits, it is hard to imagine why Beijing would risk devaluation.

The past three years have been terrible for international trade. China isn’t the only major economy suffering from weak domestic demand, but it has behaved far more responsibly than Europe and Japan, which have forced their adjustment costs onto the rest of the world. Maintaining the yuan’s value has been good for both China and the world. It wouldn’t help for Beijing to change strategy.

評論

目前還沒有任何評論

登錄後才可評論.