PC2BUY

股經

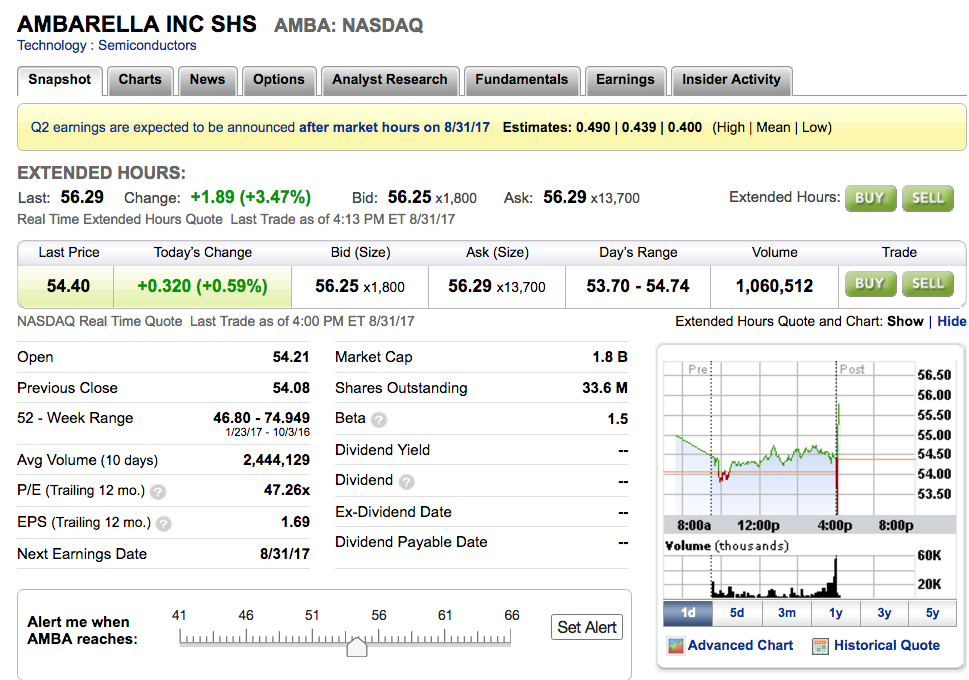

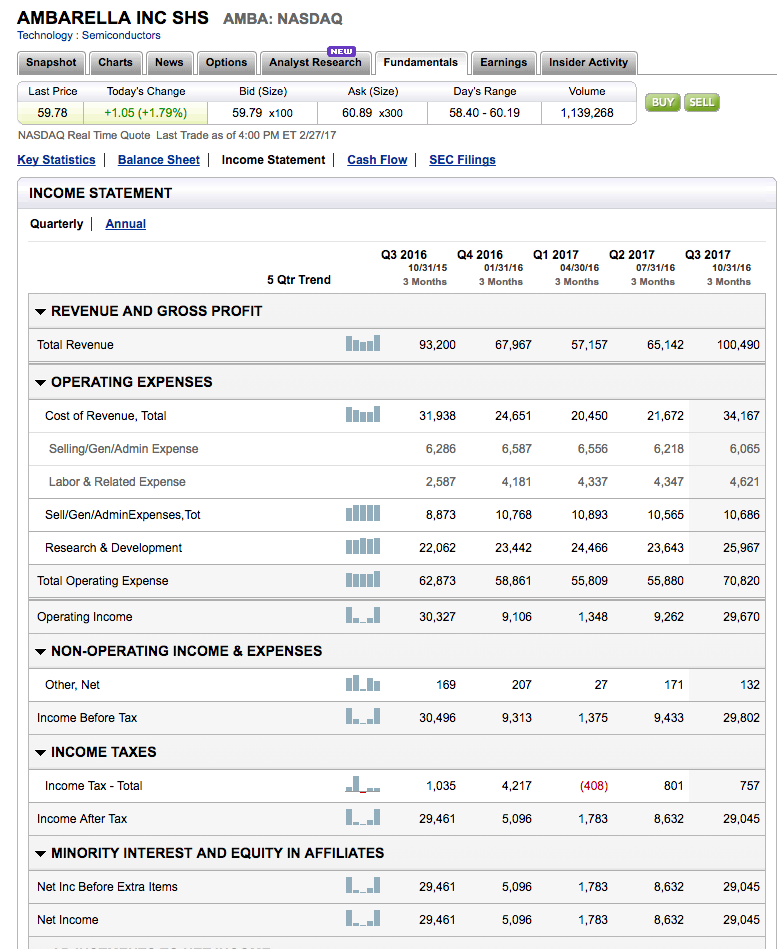

Reports Q2 (Jul) earnings of $0.48 per share, excluding non-recurring items, $0.04 better than the Capital IQ Consensus of $0.44; revenues rose 10.0% year/year to $71.63 mln vs the $70.79 mln Capital IQ Consensus.Gross margin on a non-GAAP basis for the second quarter of fiscal 2018 was 63.0%, compared with 67.1% for the same period in fiscal 2017. For the six months ended July 31, 2017, non-GAAP gross margin was 63.6%, compared with 66.0% for the six months ended July 31, 2016.This compares to guidance for between 62.0% and 63.5%Co issues in-line guidance for Q3, sees Q3 revs of $87.5-90.5 mln vs. $88.95 mln Capital IQ Consensus Estimate; Gross margin on a non-GAAP basis is expected to be between 62.0% and 63.5%"During the second quarter, we had solid growth from IP security, both from professional and home monitoring camera markets. We also continued to see growth in our OEM auto business, with strong design win activity and revenue from OEM auto video recorders," said Fermi Wang, CEO of Ambarella. "We continue to invest in the technologies required to deliver future generations of highly intelligent, HD and Ultra HD cameras with particular emphasis on high performance computer vision functionality. We see computer vision as a key differentiator for us in camera markets, including automotive, IP security, drones and robotics, and it is our key area of focus for the future," he said.

周易第13卦詳解

While it is true that AMBA today does not offer a competitive chip to MBLY, we believe the company is moving in this direction and likely will in the late-2018, early-2019 time-frame. Thus far, AMBA has distinguished itself with the industry's best image signal processor (ISP) technology (endorsed by wins with all the leading camera brands across the wearable, security, drone and after-market auto verticals). What AMBA has lacked in products on the market is the computer vision technology perfected by MBLY for identifying objects on the road. That being said, AMBA has acquired technology along these lines (the mid-2015 acquisition of VisLab, a specialist in self-driving car tech using cameras) and has already taped out its first computer vision chip (designed for drones) last month. Additionally, we note AMBA does have a small automotive business (primarily dashcam camera ISPs) and believe the company has been showing its technology to large automakers for some time. We note that many large automakers have yet to make a decision on Level 4/5 silicon, including Toyota, Honda and Hyundai. Both Ford and General Motors appear to be building their own in-house systems but it is not clear to us what silicon will be used and for what purpose (we understand GM's Cruise Automation system does run on NVDA's silicon). The bottom line is that we see many entry points for AMBA in the coming years and would also expect some automakers and hedge their bets and contract with multiple approaches.

current status : 2017-02-17 $55.47

not looking good !!! still holding..... I am not retreating ..

Current Status : $51.64 ( 01-13-2017 )Falling from $58.18 ( 01-05-2017)

--> $54.62 ( 01-06-2017 )

AMBA reached $58.18 ( 01-05-2017 )

my target price : $98 by JUNE 2017

next target : $57.50 12-31-2016 ( reached 01-05-2017 )

recent low reached $49.58 ( 01-12-2017 )

1y5m 5m 4y

how possible is it for AMBA to hit $98 again ?

tiny hammer with low of $49.58

AMBA status : indecision DOJI 12-23-2015

it was $49.58

好像是

你應是對的 , email me , please , jimmy@yehsir.com

貼不了跟圖啊。。。sorrry