insight

工程技術,地產投資,信仰家園,時尚生活

![]()

![]() Photo by Nolita

Photo by Nolita

RETAIL SECTOR:

Rents on that stretch of Upper Fifth Avenue range from $1,800 a square foot to $2,500 a square foot.Manhattan retail rents vary wildly amid recession

The economy may have slowed, but Manhattan is still home to several hot neighbourhoods, some of which fetch more than $2,000 a square foot in ground-floor retail space, according to the Real Estate Board of New York's fall retail report.

Asking rents on the gilded strip of Fifth Avenue above 49th Street, home to such luxury tenants as Saks Fifth Avenue and Armani, rose to $2,050 a square foot, up 46% compared to the same time last fall. Meanwhile, rents in the trendy Meatpacking District were up 23% over last year to $375 a square foot. Times Square rents also increased. Rents rose 6% to $821 a square foot as the neighborhood continues to attract big-name tenants, including Disney which is in negotiation for space there.

Meanwhile, SoHo rents increased by 12% to $483 a square foot as the promise of proximity to popular retailers such as Topshop and Uniqlo on Broadway whetted demand for space.

“Our advisory committee reports solid activity and deal flow despite the economic downturn,” said Steven Spinola, president of REBNY, in a statement.

Not all neighborhoods saw rents rise, which helped businesses find affordable space. “Retailers that were formerly priced out of the market now have an entry point for the first time in years,” Mr. Spinola said.

Retailers such as Kohl's, discounter TJ Maxx, and CB2, Crate and Barrel's less expensive line, are searching the city for first-time or additional locations.

The West 34th Street shopping corridor between Fifth and Seventh Avenues saw asking rent decline 35% over last fall to around $421 a square foot. Such low prices enabled teen retailer Aéropostale to sign on for 5,700 square feet at 15 W. 34th St., its first street-front flagship here. The store opened Tuesday.

The luxury strip on Madison Avenue between East 57nd and East 72nd streets saw a decline in asking rents of about 20% to $919 a square foot. Prices also plummeted in the Financial District and on East 86th Street. - 2009 November 18 CRAINS NEW YORK

OFFICE MARKET

Largest Landlord

SL Green has been on an acquisition binge. In the last month, it has reached agreements to buy 600 Lexington Ave. for $193 million and 125 Park Ave. for $330 million. To raise cash for even more purchasers, SL Green announced last week it would sell its 45% stake in 1221 Sixth Ave. in a deal that would net about $500 million. 2010 May 17 CRAINS

Office rents: Biggest plunge in 25 years

- CPPIB buys Manhattan

- Downtown

- Midtown

- 200 West St - GS's new digs

- Vacancy in Downtown Towers soar

- Downtown is hot again!

Enormous growth in sublease space pushed Manhattan office rents to their biggest quarterly decline in 25 years as they fell 6% in the first three months of this year, according to a report released Tuesday by Cushman & Wakefield Inc.

Rents fell to an average of $65.01 a square foot in the first quarter, and the $4.43 drop from the end of 2008 was the largest quarterly descent since Cushman began keeping records in 1984.

Rents have slid 11% since hitting a high of $72.97 a square foot in the third quarter of 2008. By the end of the year, rents are likely to plunge 30% from their peak, according to Joseph Harbert, chief operating officer of Cushman & Wakefield’s New York Metro region.

“Sublease space is on the rise, tenant demand has decreased and landlords are becoming more competitive to attract new tenants and retain current ones,” Mr. Harbert said. “The net result is rents falling faster than they did in the last two recessions.”

The rent slump comes as the amount of sublease space on the market nears a five-year high. Sublease space more than doubled to 10.3 million square feet at the end of the first quarter, up from 4.4 million square feet a year earlier.

Sublease space places downward pressure on rents because the companies looking to shed their excess space offer it at deep discounts to what the building’s owner is asking for leases.

Mr. Harbert cited an average 15% to 20% difference between a rent asked by a sublessor and a landlord. But in some neighborhoods the difference is much higher, especially when struggling financial firms (which lease about a third of Manhattan’s office) enter the equation.

On Park Avenue, which is awash is sublease space from struggling financial firms, landlords are asking an average of $107 a square foot compared to subleases of $72.30 a square foot—a difference of 48%.

“You can do a deal on Park Avenue in the 50s [dollar a square foot range],” he said.

The rise in sublease space was a major factor in pushing the overall vacancy rate for Manhattan to 9.6% in the first quarter, up from 6.1% at this time last year and the highest level since the third quarter of 2005.Midtown, home for many banks and brokerages, had the highest vacancy rate, at 10.5%. Rents in that neighborhood fell 8% from the fourth quarter of last year through the first three months of this year. They have tumbled 13% since the third quarter of 2008, when they peaked at $84.48.

A dearth of tenants has also helped push up vacancy rates throughout Manhattan. Leasing activity totaled only 3 million square feet in the first quarter, making it the least active first quarter on record. Overall leasing activity tumbled 39% from the year-ago period.

The dismal state of the leasing market certainly won’t help bolster the moribund investment-sales market. During the first quarter, transactions valued at $10 million or more totaled $1.1 billion, down 31% from the year-ago period. Fifteen deals closed during the first quarter, compared with 25 in the first three months of last year.

“The larger issue is the inability to get debt financing,” Mr. Harbert said. “It is going to take a while for the situation to work itself out.”

The outlook seems grim. There are only $100 million worth of properties under contract now, down from $3.5 billion a year earlier. - 2009 April 07 CRAINS

Vacancies in prime office buildings soar 66%

Vacancy rates for Class A office space in the city have soared 66% over the last 12 months according to a new report from Jones Lang LaSalle, hitting 11.9% as the first quarter draws to a close.

The preliminary first-quarter results revealed that midtown fared even worse, with Class A office vacancies soaring to 13.5%—the highest rate recorded since Jones Lang LaSalle began tracking vacancies in 1995.

The broader picture was not quiet as bleak. Citywide, there was a 55% increase in vacancy rates across all types of office buildings, according to the report.

“We are likely to see vacancy rates rise across the entire city as companies continue to merge, downsize or file for bankruptcy,” said James Delmonte, vice president and director of research at Jones Lang LaSalle.

According to Mr. Delmonte, there have been just four signed leases for space larger than 100,000 square feet so far this year, compared with more than 17 during the first quarter of 2008. What’s more, all of this year’s top three deals were renewals rather than new leases. The largest lease renewal was the one signed by Polo Ralph Lauren for 193,000 square feet at 25 W. 39th St. earlier this year.

As more office space comes onto the market, asking rents are beginning to plummet. Overall, asking rents in the city fell about 10% over the last 12 months, dropping to $64.43 per square foot in the first quarter. Class A rents fell 11% to $74.88 per square foot for the quarter. Meanwhile, Class B rents fell more than 12% to $49 per square foot.

Meanwhile, the gap between rents that landlords are asking for and those that tenants end up agreeing to pay, is ballooning. Deals have been getting done at a discount of as much as 30% once concession like months of free rent are included, notes Mr. Delmonte.

“Rents are tied to employment projections,” he says. “Job cuts are expected through at least the first quarter of 2010 and we can expect asking rents to continue to fall.” - 2009 March 26 CRAINS

INVESTMENT PROPERTY

Someone forgot to tell the Canada Pension Plan Investment Board that the Manhattan office market is unappealing.

The pension fund said Monday it has taken minority stakes in two office towers, including a 50-storey giant in the Rockefeller Center complex in the heart of midtown Manhattan, arguing the New York office market is turning the corner after being walloped during the economic downturn.

The purchases will see CPPIB acquire 45-per-cent ownership stakes in 1221 Avenue of the Americas and 600 Lexington Ave. from SL Green Realty – Manhattan’s largest office landlord – for a total consideration of $663-million (U.S.), including debt. The properties have a combined value of $1.45-billion including stakes held by other owners.

“It’s a function of looking at a market that is strengthening, and being able to find the opportunities that work for us,” said Graham Eadie, senior vice-president of investment for CPPIB.

“We have been looking for real estate opportunities, and the market has obviously been very weak over the last year or two. We’re starting to see the opportunities now and want to execute against those.”

The fund has been searching for U.S. properties to add to its $7.1-billion (Canadian) real estate portfolio, and announced another deal in April to partner with Kimco Realty Corp., North America’s largest operator of community shopping centres, in a joint venture to acquire prime neighbourhood shopping centres across the U.S. market.

Mr. Eadie said CPPIB plans to boost its real estate portfolio in future from 6 per cent of the fund’s total holdings, but would not reveal a target for growth.

He said the fund is in talks to acquire more U.S. properties, because “it’s an area where we’ve been able to find the quality of asset we’re looking for at the prices we want right now.”

The 2.5-million-square-foot McGraw-Hill building in Rockefeller Center has the publishing firm as a key tenant, along with Société Générale SA and Morgan Stanley. It will be managed by Rockefeller Group International Inc., which owns the other 55 per cent of the building.

The smaller 600 Lexington Ave. property, which is 300,000 square feet and 36 storeys, is a “boutique” office space with smaller tenants and no major anchor. SL Green will be the majority owner and manager of the building.

“We think the leasing market is starting to improve and stabilize in that market, so we think it is a good time to enter,” Mr. Eadie said. “And these are our first deals in the Manhattan market.”

Shant Poladian, a real estate analyst at Canaccord Adams Inc., says the office market in Manhattan has strengthened significantly in recent months and companies operating in the sector are reporting better financial results. He said Brookfield Properties Corp., another major New York office property owner, reported leasing volume in Manhattan has bounced back to its five-year average rate.

A key factor for growth in Manhattan’s depressed office market has been the rapid recovery of major players in the financial services sector, such as Citigroup Inc., Bank of America Corp., and JPMorgan Chase & Co. With growing profitability, the firms have been hiring and their office space requirements are growing.

“The market’s already turning,” Mr. Poladian said. “Barring some contagion coming out of the European debt situation, things have actually been improving quite a lot.”

SL Green is “a strong player in the Manhattan market” but has fairly high debt levels, Mr. Poladian said, so selling minority stakes in two buildings is a logical move to raise financing without tapping the public market. - 2010 May 11 GLOBE & MAIL

Meanwhile Shorenstein sells to SL Green

San Francisco-based Shorenstein Properties LLC has sold 125 Park Ave. in Manhattan to SL Green Realty Corp. for $330 million.

The 26-story, 651,000-square-foot office tower, across from them entrance to Grand Central Terminal, is known as the “Pershing Square Building.” Major tenants include FGIC Holdings, Meredith Corp., Newmark Knight Frank, Reed Elsevier and Canon Business Solutions. It is 99 percent leased.

Shorenstein purchased 125 Park Ave. in 2004 for $225 million, according to press accounts at the time. Shorenstein made a number of improvements to the property, including a $4.5 million lobby renovation.

The ornate pre-war office tower, with a terracotta brick exterior, was designed by York & Sawyer and completed in 1923.

“As Manhattan’s largest commercial landlord, with a commanding presence in the Grand Central submarket, we see 125 Park Ave. as a perfect fit with our other area properties,” said Andrew Mathias, president and chief investment officer at SL Green. - 2010 May 12 BUSINESS JOURNAL

Deals Difficult to Find as Banks extend Payouts

Some eal-estate funds, which raised billions of dollars hoping to pounce on bargain properties, are returning money to investors after finding slim pickings, as many banks avoid dumping property by extending and restructuring loans.

The private equity refunds highlight a supply-demand imbalance in the commercial real-estate industry. Investors have accumulated billions of dollars to look for returns in the down-on-its-luck market for office, retail stores, hotels and other commercial property. But not too many properties are for sale, as many real-estate owners are holding onto assets in hopes of a stronger rebound. Property owners have benefited from low interest rates, which keep loan payments low, and banks' reluctance to sell troubled loans.

"Funds are fighting over a slim group of available deals," - 2010 May 26 - WALL ST JOURNAL

Macklowe's Split! - 2010 May

Are Deals Financable?

Fillmore, Deutsche Bank Pact Hit a SnagCB Richard Ellis Investors is back in the bidding for the office portion of 1540 Broadway, a skyscraper in New York's Times Square connected to landlord Harry Macklowe.

A deal hasn't closed, but a person familiar with the matter said CBRE Investors, the asset-management unit of CB Richard Ellis Group Inc., would pay as little as $355 million, a major drop in value.

"That's a harsh price for a very well located building," said Dan Fasulo, managing director of property-tracking firm Real Capital Analytics.

According to city records and loan-marketing documents, Mr. Macklowe attributed the value of the office building to over $950 million when he bought it in February 2007 as part of a $7 billion skyscraper spending spree. The tower's 880,000 square feet of office space had sold in 2006 for $525 million.

In early 2008, unable to refinance short-term debt, Macklowe Properties handed back control of the seven skyscrapers to lenders led by Deutsche Bank AG. Deutsche has been trying to sell 1540 Broadway along with the nearby Worldwide Plaza, also part of the Macklowe portfolio. Eastdil Secured is the sales broker. CBRE was in the mix early for 1540 Broadway, then hedge fund Fillmore Capital Partners LLC was close to securing both towers. The Fillmore deal died last week, putting CBRE's deal back in the saddle, according to several people familiar with the matter. - 2009 February 18 WALL ST. JOURNAL

An effort by real-estate hedge fund Fillmore Capital Partners and Deutsche Bank AG to salvage a troubled debt investment in two prominent Manhattan skyscrapers has hit the rocks.

A contract was expected to be signed Monday in which Fillmore would acquire Worldwide Plaza and 1540 Broadway, office properties once worth a total of more than $2 billion. New York landlord Harry Macklowe had purchased the towers as part of his ill-fated acquisition of seven skyscrapers in 2007. Unable to refinance the buildings' debt, Mr. Macklowe turned control of the towers back to Deutsche Bank, the holder of the $1.2 billion first mortgage, in early 2008.

Last-minute talks late Sunday for Fillmore -- a junior "mezzanine" lender on the properties -- to buy the towers using Deutsche Bank financing fell apart, according to people familiar with the matter. It was unclear what caused the snag. One person familiar with the matter says there is still a small hope a deal could happen. The deal was so close to getting done the current buildings' management had been instructed to turn over the property Monday. That decision was reversed late Sunday.

Deutsche Bank, Fillmore and the other lenders involved had been trying to sell the properties since early 2008. And Deutsche Bank had agreed to provide financing to prospective buyers -- an incentive given the dreadful state of the credit markets. Early bids came in above $2 billion. But a tentative deal for General Electric Co.'s NBC Universal to take space in the pyramid-topped Worldwide Plaza, at 825 Eighth Ave., never materialized. That discouraged potential buyers who calculate returns on investment based on how much cash buildings generate from rent collections.

Executives from all parties involved either didn't return calls or declined to comment. - 2009 February 9 WALL ST JOURNAL

The travails of New York developers Harry Macklowe and his son, William Macklowe, continue. A mezzanine lender on 1330 Sixth Ave., an office tower Macklowe Properties purchased in 2006, has moved to auction off its interest in the tower after its loan matured.

The mezzanine lender is Cadim, the real-estate arm of Canadian pension manager Caisse de Dépôt et Placement du Québec. Cadim lent $130 million to the building and holds the most senior portion of several mezzanine slots. The loan matured Jan. 9. Other more junior mezzanine holders include Deutsche Bank AG, which also originated the $240 million senior mortgage. That loan was securitized.

The Macklowes, who have $100 million of equity in the project, purchased the 42-story tower in late 2006 for nearly $500 million, more than three times what it sold for six years earlier. The tower has a substantial amount of vacant space.

Mr. Macklowe, who last year had to hand back control of seven skyscrapers and sell four others because of debt problems, hired Carlton Group to find new investors to replace Cadim at 1330 Sixth Ave. Cadim then hired Eastdil Secured to run the auction. The auction is scheduled for April 22. Talks continue among the various parties. A Macklowe spokesman declined to comment. A Cadim spokesman declined to comment. - 2009 March 17 WALL ST. JOURNAL

- GM tower space fetches $130-plus

- 60 Fifth Avenue - Forbes Bldg

- 1 Madison Ave - Standard Charter's Lease

- "Unable to Renogiate Lease"

- HSBC Sale Leaseback

- NY Times Building

- Benchmark: 1540 Broadway : $392 per sq ft

- Manhatten's 20 largest distressed properties

- Harry Macklowe's buildings

- Korean bank buyer of AIG's offices >> REUTERS >> MORE >> Aiming for $2,000 psf on residential at 70 Pine

- Caisse seizes 1330 Avenue of America's

- Re-think Ground Zero

- Office Rents: Biggest Plunge in 25 years

- Vacancies in prime office soar

- AIG Building to sell at fraction of cost

- Banks & securities firms give back 8 million sq ft

- Manhattan Office Vacancy

- Tenants move out in record numbers

- Surge in Subleasing driving rents down

- Central Park

- Corporate Mobility

Manhattan Won't Avoid Property Crunch

Manhattan prices fall most in 5 years

Number of 2008 sales falls 23%; units put up for sale jump 41%Manhattan apartment sellers cut prices by the most in five years last year and unsold inventory rose to the highest since 1999 as the economy retreated.

The average listing discount climbed to 4.1 per cent, the highest since 2003, as buyers negotiated for reductions off the asking price. The number of condominiums and co-ops for sale jumped 41 per cent last year to 9,081 even as the median price reached a record US$995,000, appraiser Miller Samuel Inc and broker Prudential Douglas Elliman Real Estate said on Tuesday.

New York City is bracing for a drop in property values after three of the five largest investment banks collapsed. In the Hamptons, on the eastern end of Long Island, prices are already falling. Banks and securities firms have cut more than 180,000 jobs in the past year, according to Bloomberg data, as the recession entered its second year and the global credit crisis forced writedowns and mortgage-related losses of US$1.18 trillion.

'There clearly was long-running irrational exuberance out here in real estate,' said Diane Saatchi, senior vice-president for broker Corcoran Group Inc, in East Hampton. 'It's gone full circle from people who would pay any price because they had to have the house, to people who pick a price and take any house at that price as long as they think it's discounted.'

The median price in the Hamptons, New York's summer playground for the rich and famous, fell almost 13 per cent last year to US$850,000, the first decline since 2000. Discounts on Hamptons homes rose to 11.1 per cent in 2008, according to Miller Samuel-Prudential data.

Wall Street firms are expected to lose US$47.2 billion in 2008 and further shortfalls are expected in 2009, Mayor Michael Bloomberg said last week.

Budget officials assume the city will lose 294,000 jobs from mid-2008 through 2010, including 46,000 in financial industries. The mayor is founder and majority owner of Bloomberg News parent Bloomberg LP.

The firings mirror the national recession that has driven unemployment in January to the highest since 1992 and pushed home prices down the most since the Great Depression.

The securities industry accounted for 51 per cent of the growth in wages in Manhattan's private sector from 2003 to 2007, according to the US Bureau of Labor Statistics. 'Prices have to drop,' Dottie Herman, chief executive officer of Prudential Douglas Elliman, said in an interview. 'They have to, have to, have to - and they have.'

In Manhattan, the number of sales declined 23 per cent last year from 2007, Miller Samuel and Prudential said. Falling sales and rising inventory preceded lower home prices nationwide.

The increase in inventory in Manhattan was largely driven by a slowdown in transactions in the second half, said Jonathan Miller president of Miller Samuel.

The median sales price for the entire year rose 11 per cent to a record US$955,000, according to the report. The gain mostly reflects deals from the first half of the year, before the collapse of Lehman Brothers Holdings Inc, and closings from new condominium developments.

The Miller Samuel-Prudential report also shows the heights that Manhattan's real estate market achieved over the last decade, a period of easy credit.

In 1999, the median sales price of all Manhattan apartments was just US$310,000.

By 2004, it almost doubled to US$605,000. The average price per square foot rose from about US$400 in 1999 to US$1,251 last year, the report said.

The median price of two-bedroom apartments rose 178 per cent since 1999 to US$1.6 million last year. One bedrooms rose by 200 per cent over that time, to a median of US$750,000 last year. Three-bedrooms sold at a median price of US$3.79 million, a 161 per cent increase from 1999.

Prices have also skyrocketed for Manhattan townhouses. In the past decade, the median has risen 156 per cent to US$4.995 million.

They jumped even higher for the category known as 'luxury townhouses', which Mr Miller defines as the top 10 per cent of all sales. The median jumped last year to US$31.8 million, up from US$6.5 million a decade ago.

Now the market is making an about face. Prices for luxury apartments in Manhattan, defined by Ms Herman as units selling at US$3.5 million and above, are now selling at discounts of about 25 per cent off the asking price, she said.

A three-bedroom, three-bathroom condominium on Tribeca's Hudson Street is now selling for US$4.6 million after being lowered almost US$1.3 million since August, according to Streeteasy.com, a property data service. A condo in Trump Tower on Fifth Avenue in midtown was cut 16 per cent to US$4.95 million since it was first listed in November.

The Financial District, which saw the largest year over year price increase for co-ops in 2007, was the neighbourhood with the largest price per square foot decline in 2008, according the report.

The price per square foot for co-ops there declined by almost 19 per cent to US$857 in 2008, the result of lowered demand spurred by Wall Street layoffs, the report said.

'You're going to see stronger, less attractive numbers' in the first quarter, said Ms Herman.

The reported available inventory tally does not include new developments where units have yet to go on sale, Mr Miller said. 'That is definitely an undercount,' he said. 'There's a lot of shadow inventory in the background.'

The trend is likely to continue, said Damon Liss, an interior designer who is now trying to sell a three-bedroom cottage in East Hampton with a swimming pool for more than US$1 million.

'There's a big disconnect between buyers and sellers,' Mr Liss said. 'Buyers want 50 per cent discounts and sellers don't want to reduce the price at all. That's why transactions are down. Both buyers and sellers are being equally unrealistic.' - 2009 March 5 Bloomberg

When it comes to property prices, that strip of rock just south of the Bronx is often perceived as invincible.

Across the U.S., house prices have fallen 19% from their peak, according to the S&P/Case-Shiller Home Price index. New York City, as a whole, is down 10%.

Meanwhile, on planet Manhattan, the median price of an apartment rose above $1 million for the first time in the second quarter of 2008, according to Miller Samuel, a real-estate appraiser.

Even in Gotham, reality bites eventually. Three big problems are likely to hit in 2009.

First up: Job losses on Wall Street. In 2006, the most recent full year of New York State Department of Labor data, finance and insurance companies employed 15.7% of Manhattan's workers. They earned an average of $269,000, more than 2.5 times the average private-sector wage. Property prices will suffer from slashed bonuses and submarine stock options, not to mention the pink slips.

Wall Street's woes also mean tighter credit. The Federal Reserve's latest "beige book" survey of financial conditions says this of a softening Manhattan condominium and co-op market: "A growing number of deals are said to be falling through, due to difficulty in getting financing -- largely at the middle of the market."

The third headwind is a stronger dollar. Jonathan Miller, Miller Samuel's president, estimates one in three new apartments are sold to foreigners, primarily Western Europeans. - 2008 September 22 WALL ST JOURNAL

Real estate market girds for Lehman fallout

Manhattan vacancy rates to rise as building prices fallThe fallout from Lehman Brothers’ bankruptcy could push Manhattan’s commercial real estate vacancy rate up to nearly 10% by the first quarter of next year, according to a report Monday from real estate brokers Jones Lang LaSalle.

The impact will likely fall hardest on Class A midtown buildings, where the vacancy rate could skyrocket to 12% if the bank disposes all of its space, according to the report, based on its estimate of Lehman holding 2.7 million square feet of space. Currently, vacancy rates for midtown Class A properties as well as in Manhattan overall are running at 8%.

Lehman Brothers owns its 1 million square foot headquarters at 745 7th Ave. while leasing acres of space at other locations including 399 Park Ave.

“The effect is going to be pretty dramatic,” says Peter Riguardi, president of Jones Lang LaSalle’s New York Market.

Those estimates don’t include the fallout from Bank of America’s sudden acquisition of Merrill Lynch or American International Group’s enormous problems. Bank of America executives on Monday said they aim to cut $7 billion in costs from Merrill, which will almost surely mean shedding staff and space. Merrill leases 4.2 million square feet at the World Financial Center but only occupies about 2.6 million feet of it. It also leases an additional 850,000 square feet in various locations in Manhattan.

Mr. Riguardi notes that AIG occupies about 3 million square feet of space downtown. AIG owns its 775,000 square foot headquarters at 70 Pine Street and in June signed a lease for 800,000 square feet nearby at 180 Maiden Lane, where it planned to consolidate office it has scattered around downtown.

Real estate executives say the turmoil could drive rents down between 15% and 20% by next year. Until now, asking rents have remained strong, jumping 21% to $71.59 per square foot in the second quarter from the same period in 2007, according to Cushman & Wakefield.

The tumult on Wall Street was already hurting Manhattan's office market. The vacancy rate climbed to 7.1% in the second quarter, up nearly 2 percentage points from the year-ago period, according to Cushman & Wakefield Inc. In addition, brokers say that tenants are taking longer to sign leases. That sluggishness comes at a time when troubled financial firms are retrenching, adding more space to a market that now has 20 million square feet available—up 35% from a year ago.

The problems will also further depress the market for commercial office towers. ast year, Manhattan office buildings fetched an average of $972 per square foot, according to Cushman & Wakefield. At that rate Lehman’s HQ would fetch nearly $1 billion. Experts say that sum is now highly unlikely.

AIG’s headquarters would be considered less attractive than Lehman’s because it is older and located downtown. Typically, midtown towers fetch higher prices than their counterparts in the financial district. - 2008 September 15 CRAINS NYWho Needs a Mortgage Anyway?

While the mortgage markets have been convulsing, Wall Streeters have been completing one big-ticket deal after another, buying condos, co-ops and town houses at some of New York's most prestigious addresses.

In January, Lloyd C. Blankfein, chief executive of Goldman Sachs, closed on a $26 million duplex at 15 Central Park West, one of Manhattan’s hottest new buildings. Scott A. Bommer, a hedge fund manager, bought a Fifth Avenue co-op for $46 million. And Edgar Bronfman Jr., part of a private equity consortium that owns the Warner Music Group, spent $19.5 million for his own Fifth Avenue co-op.

As the mortgage mess deepened, the deals rolled on. In February, Raymond C. Mikulich, until recently the head of the real estate private equity group at Lehman Brothers, paid $17.9 million for a four-bedroom apartment at 15 Central Park West. Then Philip A. Falcone, a senior managing director at Harbinger Capital Partners, a hedge fund, closed on a deal to buy the Upper East Side mansion that once belonged to Robert C. Guccione, founder of Penthouse magazine, for $49 million.

James E. Cayne’s $28 million purchase of two units in the Plaza was not the biggest deal, but it was among the most awkwardly timed. A few weeks after the second deal closed, the Wall Street firm where he is chairman, Bear Stearns, collapsed. - 2008 April 2 NEW YORK TIMES

NEWS

In a sign of how commercial real estate values in Manhattan have deteriorated, a 21-story building there, one of the last to sell before the credit crisis, is under contract to sell again at a loss of $41 million. - 2008 July The New York Times

US retail malls' Q2 results worst in 30 years

Strip malls seeing average vacancy rates spike sharplyUS store closings and cutbacks turned the second quarter into the worst for strip mall owners in 30 years, as increasingly budget-conscious consumers flocked to low-cost warehouse-style grocery centres, according to a report by real estate research firm Reis.

Strip malls, which are usually anchored by grocery or drug stores, saw average vacancies spike 0.5 percentage points to 8.2 per cent, a level unseen since 1995, according to the report released yesterday.

Vacancies at regional malls rose 0.4 percentage points to 6.3 per cent, the highest level since the first quarter of 2002, according to the preliminary results.

'They definitely came up weaker than our expectations and we've been pretty bearish on our outlook for retail for some time,' Reis chief economist Sam Chandan said.

'In the market in general there have been a lot of store closings.'

A growing list of retailers shuttered stores ahead of lease expirations or chose not to renew leases, and as newly completed space hit the market without signed tenants.

Starbucks Corp recently said it would close 600 stores by March.

GAP Inc is looking to give up some of the 40 million square feet of retail space its leases.

That's in addition to the growing list of retailers, such as Linen 'n Things and Goody's Family Clothing, which filed for bankruptcy protection.

Consumers are constrained by increases in food and energy costs, as well as the cost of servicing debt run up during the housing boom.

In addition to cutting back on clothing, jewellery and non-essentials, they have turned to lower-price grocers such as Wal-Mart at the expense of the upper end usually found at strip malls, such as Whole Foods Market Inc, Reis said.

For the first time since 1980, more space became available to rent at strip malls than was rented out - about 3.2 million square feet more.

Part of the available space came in the form of 5.7 million square feet of new development that came on the market during the quarter.

The extra space translated into falling rents at strip malls, down 0.1 per cent to an average of US$17.60 per square foot.

'The downward pressure on rent is coming from landlords being very nervous about the idea of losing a tenant when they know that there's a paucity of replacements for that tenant in the current market environment,' Mr Chandan said.

Preliminary figures show that regional malls were barely able to raise rents, with just an anaemic 0.2 per cent rise excluding concessions, its weakest gain since the second quarter. - 2008 July 8 REUTERS

Taking Manhattan

A new record price for an office building defies the recession talkIt is said that nobody ever made money by owning the General Motors building, only by selling it. And yet again the Manhattan landmark building by the south-eastern corner of Central Park is about to change hands for a price that seems justified only by the greater-fool theory that one day someone will be willing to pay even more. In the first round of bidding, there were several offers of $3 billion, which would be a new record for a single building in America beating the $1.8 billion paid last year for nearby 666 Fifth Avenue. Hopes are high that the final price will be well above that.

No one hopes so more fervently than the owner, Harry Macklowe, who needs it to fetch at least $3.4 billion in order to repay a loan, for which the building is collateral, from the publicly traded hedge-fund group, Fortress. Mr Macklowe is in trouble because he paid too much for properties offloaded by the private-equity giant, Blackstone, from the portfolio of Equity Office Properties, a property firm it bought for a record last year, in the final gung-ho days before credit dried up. Reportedly, the rents on the GM building barely cover the interest on the mortgage.

Mr Macklowe bought the skyscraper for $1.4 billion in 2003, from owners such as Donald Trump, who regrets selling. One of the defeated bidders then, Sheldon Solow, is still contesting in court the decision to sell to Mr Macklowe, whose improvements to the building include introducing a super cool Apple Store in front of the famous FAO Schwarz toy shop.

At the very least, this high-priced bidding war suggests that New York's commercial real-estate business is in better shape than some of the city's banks. Yet, as a trophy property, the price offered for the GM building may say more about the continuing robust financial health of wealthy buyers than incremental changes in demand for office space in New York.

There is also the falling dollar. A report from Cushman & Wakefield, a property adviser, reckons that with average rents of $100 a square foot, New York ranks only the tenth-most-expensive among global cities in which companies like to put their headquarters. One bidder reportedly has strong backing from Arab investors. This is a sign that the weak dollar is making American assets attractive to foreign shoppers with cash to splash. - 2008 February 21 THE ECONOMIST

- Condos continue to increase 2008 July

- 230 Park trades for $1.15 billion

- Back to Office again; no condo conversion

- $135 million in '95; Sold in 2007 for $751 million

- Ten Most Expensive Office Buildings in New York

- Two trophy buildings worth $1 billion

- Credit Crunch affecting Manhattan leasing market

- Hudson Yards

- Manhattan cheap compared to other world-class cities

- Classic residences set the standard

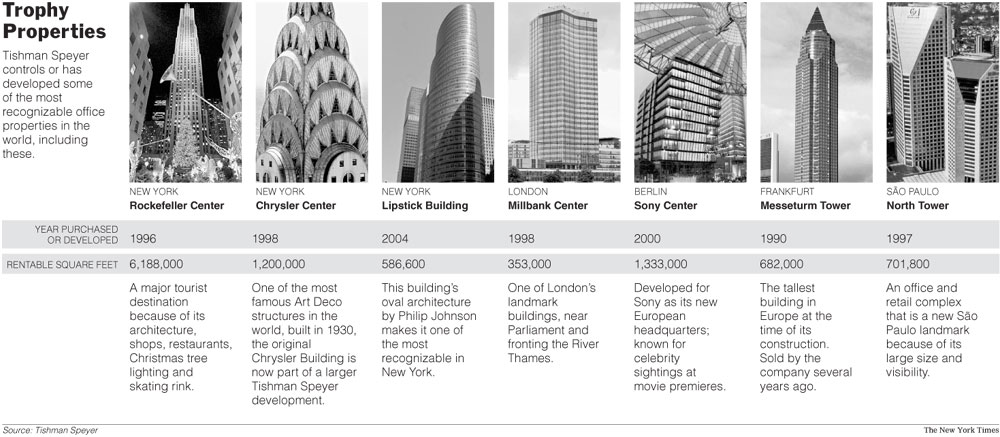

- New York's megadeal - Tishman Speyer's purchase of Peter Stuyvesant Town >> Snags encountered >> Haemorrhaging Money! >> Tishman Tanking! >> Pension Fund invited to try again

Office rents drop as space hits market

Manhattan's once red-hot commercial real estate market is developing a chillVacancy rates are edging higher. The pace of new lease signings is flagging, and the volume of sublease space hitting the market is soaring.

More important, for the first time in six years, effective rents have begun to fall.

"There's no question that rents are lower than they were last year," says David Falk, an executive vice president and principal at Newmark Knight Frank.

That trend is all but certain to accelerate as financial firms, which account for roughly a third of Manhattan's rented space, shed staff and space amid the credit crisis.

GVA Williams Vice Chairman Mark Friedman reckons that effective rents, which include the cost of concessions offered by landlords, have already fallen by about 7%. GVA found that in the first quarter of the year, midtown landlords typically gave tenants three to six months of free rent, up from zero to six months in the year-ago period. Similarly, they upped the amount they were willing to give to tenants for improvements to $40 to $50 a square foot, from $35 to $45 a square foot.

Mr. Friedman predicts rents will eventually drop 15%.

The downward pressure stems from two factors: sagging demand for space caused by the weakening economy and an avalanche of sublease space expected to hit the market in coming months.

Just starting

Financial firms, battered by billions of dollars of losses from write-downs of the value of subprime mortgages and a growing list of other products, are just beginning to shed space. In the last year they've laid off 22,000 people, according to a Crain's estimate. Experts forecast that 33,300 Wall Street jobs will disappear by next year.Mr. Falk estimates that 4 million square feet of sublease space will be unleashed in midtown alone as financial firms and others unload space amid a slowing economy. Just last week, drug giant Pfizer quietly laid plans to unload 750,000 square feet of space in midtown.

J.P. Morgan Chase is expected to be one of the largest space shedders. It could eventually unload 1 million square feet of space as it digests its purchase of Bear Stearns. Sources say Lehman Brothers is looking to unload roughly 600,000 square feet of space, while Citibank is believed to be freeing up nearly 240,000 feet at two locations.

In the last five months, 5.3 million square feet of sublease space has landed on the market, a jump of 51%. That space now accounts for 19% of the 27.5 million square feet available. Experts say that when sublease space reaches 35% to 40% of the total, it begins to pull all prices down. If Mr. Falk is correct, that tipping point could be reached in just a few months.

The problem is that sublease space is typically less expensive than space rented directly from a landlord. In May, Cushman & Wakefield Inc. reported that sublease space was nearly $14 a square foot—or about 15%—cheaper than direct space.

Bleak outlook

With oil prices rising and the economy softening, the outlook on the demand side is also bleak."The bottom line is that I don't think that corporate America is about to come in and gobble up space," says Mr. Friedman.

As a result, brokers expect that the gap between landlords' posted prices for space and what tenants actually pay will continue to widen. Mr. Falk says that, on average, tenants are signing leases that are $5 to $10 a square foot below the asking rent, up from $3 to $5 a square foot last year. The average asking rent in Manhattan is $85 a square foot.

The good news is that even with all the space that has been added to the market in recent months, the vacancy rate in Manhattan stands at a puny 6.8%, which is low by historical standards and gives landlords the edge. The question is, for how long? The vacancy rate has already risen 1.3 percentage points this year.

"It's clearly a more balanced market," says Brian Gell, a vice chairman at CB Richard Ellis Inc. "Tenants are more cautious, but those who are prepared to act will benefit."

SALES HARDER TO FINANCE

The good news for buyers of Manhattan office buildings is that prices are down. The bad news is that financing such deals remains dicey.

Two weeks ago, three properties that lenders had taken back from Harry Macklowe for failing to repay a loan were sold at prices 20% to 30% lower than what he had paid a year earlier.

But with lenders now demanding that buyers lay out 30% to 50% of the deal value in cash-up from 10% to 30% a year ago-volume has shriveled. In the first five months of this year, 33 office towers were sold, a drop of 63% from a year ago, according to Real Capital Analytics.

Scott Latham, an executive vice president at Cushman & Wakefield Inc., notes that worries about a weakening economy have put buyers on the sidelines.

"They are waiting to see what happens," he says. - 2008 June 21 CRAINSManhattan office demand strong

Demand for Manhattan office space remains strong and will dip only slightly in the new year, according to a third quarter report by Marcus & Millichap Real Estate Investment Services. By year's end, Manhattan employers were expected to have created 36,000 jobs for a 1.5 percent gain, the report said. A limit of new supply and strong demand were expected to lower the vacancy rate in 2007 by 100 basis points to 6.3 percent. But turbulence in the global financial markets' could lead to job cuts in the Manhattan financial services sector, which could tamp down demand for office space.

A total of 708,000 square feet of for-lease office space was expected to be built in Manhattan in 2007. Asking rents jumped by 18 percent this year to $60.71 per square foot, the report said, while effective rents were expected to increase 20.8 percent to $54.15 per square foot. - 2007 December 12Midtown Manhattan Office Rents Exceeds Dot-Com Peak

Average effective rental rates for Class-A office space in Midtown Manhattan have surpassed the all-time high rental rates reached during the dot-com peak at the end of 2000. According to the Studley Effective Rent Index (SERI) covering Midtown and Downtown, Midtown's spike in rental rates is due to a number of real estate components impacting pricing, namely higher real estate taxes, operating expenses, and electricity costs, not to mention supply and demand.

The national SERI report indicates rental rates are steadily increasing in markets throughout the United States, and Midtown Manhattan follows suit, although its effective rental rates are markedly higher than in most other major tier-one markets.

Midtown New York's average rent of $75.42 per sq. ft. is 1.2% higher than 2001's peak rate. Downtown New York's average effective rent of $40.95 per sq. ft., however, is 18.2% lower than the peak value, not even close to the levels achieved during the dot-com heyday.

"The entire business landscape has changed since 2000," says Steven Coutts, senior vice president of Studley's National Research Services. "Prime office buildings have been trading for amazingly high prices for several years with landlords garnering higher rents as a result of the dearth of product in Midtown. It's a domino effect ? the increase in building revenue escalates the building's value leading to higher property taxes thereby increasing the total rent even more."

Operating expenses have also increased over the last five years, says Coutts, who attributes some of this to the added security in buildings post 9/11. From 1995 to 2000, average operating expenses increased from $6.75 per sq. ft. to $7.82 per sq. ft., a 16% increase, but operating expenses increased by 30% in the succeeding five-year period between 2000 and 2005.

"Interestingly, average increases in electricity costs over the past 10 years have been moderate, averaging 3.1% annually," adds Coutts. "But in the last year, average costs jumped by 13.5% as the nation grapples with the current energy crisis." - 29 June 2006RESIDENTIAL

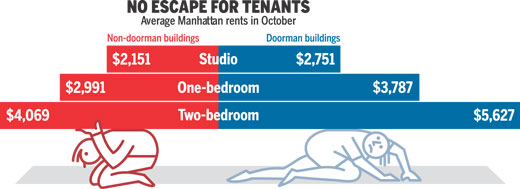

- Manhattan rentals now average $3,310 per month ( 2008 April 8)

In a Hot Market, All the City Is a Condominium

East Side, West Side, all around town, every form of real estate, no matter the tenancy, is being sold to investors for conversion into residential condominiums. They range from four-story buildings in TriBeCa that are selling for more than $550 a developable square foot to tennis facilities in Queens to factories in Long Island City to parking garages and vacant lots.Over the last decade, a number of office buildings in Lower Manhattan have been converted into residential towers. Last week, Kent Swig, president of Swig Equities, signed a contract to buy a 103-year-old, landmarked, 21-story, 540,000-square-foot building at 25 Broad St. It was bought in 1994 for $5 million by Crescent Heights. Crescent spent $55 million in 1997 to redevelop it into 347 apartments, 21,400 square feet of retail and commercial space, and 6,800 square feet of office space. Industry sources said the property sold for $260 million. Also last week, a joint venture of Worldwide Holdings and Lubert-Adler entered into a contract to sell an office building at 88 Greenwich St. to Thorwood Real Estate, a partnership of Joseph Sitt and Andrew Heiberger, for $195 million. The 365,000-square-foot, 72-year-old building was converted into 458 apartments in 2000.

Thorwood is also buying a building at 158 Madison Ave. and will convert it into a 22-story loft condominium.A 95-year-old, 185,000-square-foot office building at 485 Fifth Ave. will be sold next month to a joint venture of Michael Belfonti, Adam Hochfelder, and the Carlyle Group. The partnership will pay $88 million to a group of investors including Jack Forgash, which purchased the former Rogers Peet building for $54 million earlier this year. The buyers plan to convert the property into condominiums.

Last month, Monday Properties entered into a contract to buy a 20-story, 210,000-square-foot office building at 386 Park Avenue South from Park South Control for $71 million. Industry insiders think it will be converted to condos.

The 143,000-square-foot Stuart Dean Building at 355-366 Tenth Ave. will be sold and converted into a residential tower. Insiders said Gary Barnett's Extell Development will pay $25 million for the site. Extell recently bought the one-story Ritz Furs shop on 57th Street between Sixth and Seventh avenues, as well as the transferable air rights. It plans to demolish the building and construct a 37-story condominium tower.

New York City is losing tennis courts. Two years ago, a tennis center atop a parking garage on 31st between Fifth Avenue and Broadway was sold and converted into a Con Ed substation. The 6-acre East River Tennis Club on the waterfront at 44-02 Vernon Blvd. in Long Island City has closed to make way for a major residential development: two condominium towers with a total of 1,080 units and two rental buildings with 1,100 units.

A few years ago, Eagle Electric moved its manufacturing operations to Mexico. Earlier this year, the Andalex Group bought one of its buildings at 45-31 Court Sq., near the 48-story Citigroup tower in Long Island City. It plans to renovate the property into 238 luxury condominiums. Another facility in Astoria at 21st Street and 24th Avenue is being converted into 188 condominiums.

A 12-story, 147,000-square-foot office building with possible air rights at 63 W. 38th St. is on the market for redevelopment as residential condominiums or a hotel. A few blocks away, a 14-story office and showroom building at 215 W. 40th St. is being marketed for $22.5 mil lion as a residential conversion. A zoning variance may be required.

In May, the City Council approved a zoning plan for Williamsburg and Greenpoint. Sites there are now selling for more than $175 a developable square foot. There are two developable Gabila's Knish Factory properties at 111-113 S. Eighth St. and 110-120 S. Eighth St. and Bedford Avenue, less than 10 blocks from the subway station at Hewes Street and Broadway. The sites are under contract for sale, and were listed for $7.5 million.

At least six other sites in Williamsburg and Greenpoint are on sale for residential conversion, with prices ranging from $100 to $225 a developable foot.

A five-story office building at 530-540 Atlantic Ave. in downtown Brooklyn is being marketed for $18.5 million as a residential conversion prospect. A 190,000-square-foot development site occupying the entire block of Myrtle Avenue between Gold and Prince streets, blocks from MetroTech and the Atlantic Terminal, is being marketed for $21 million.

A new stadium for the Mets and the Olympics is planned in Flushing. Muss Development plans a mixed-use complex on the corner of College Point Boulevard and Roosevelt Avenue on a site formerly occupied by Con Ed. It will have over 1,200 apartments, a Target, and a Home Depot. Shaya Boymelgreen is converting the former RKO Keith at 129-43 Northern Blvd. into a mixed-use facility that will have 250 condominiums, 25,000 square feet of retail, and a parking garage.

Everyone wants a piece of the real estate market. A prominent developer told me that a physician friend called him and told him he wants to join him and become a developer. The developer asked the physician if he would like him to assist him while he is performing surgery. Real estate prices have risen to records, and today is not the time for amateurs to try their luck as developers.

"I am astonished by the lack of differentiation in underwriting by the financial community when it comes to quality of sponsorship, capital structure, and location of a development," a vice president of real estate finance at HSH-Nordbank, James Fitzgerald, said. "We remain vigilant and cautiously optimistic on select developments. It is no longer the domain for amateurs." - by Michael Stohler NEW YORK SUN Real Estate, p. 12 23 June 2005

![[Manhattan condo prices]](http://s.wsj.net/public/resources/images/MI-AS493A_REALH_NS_20080921190427.gif)

- Rent in the Hamptons

- Expensive housing

- Most expensive Coop - $46 million

- 2007 Year of 'Iron Bubble'

- Less Residential turnover in 2007

- Luxury Residential

DISTRICTS

Upper East Side

The Upper East Side is home to many of New York's best co-ops and condos and covers the area of the City north of 59th Street and east of Fifth Avenue. The apartment buildings that line Fifth and Park Avenues house some of the most expensive properties in the City. This is a wonderful family area; however, it is still a comfortable place to live for many singles and young professionals. One will find many elegant shops and boutiques, excellent private and public schools, access to Central Park as well as museums such as The Metropolitan, The Guggenheim, The Frick, and The Whitney. Within the boundaries of the Upper East Side are areas such as Carnegie Hill, East End Avenue, and Yorkville. It is a safe, popular and predictable area in which to live

Upper West Side

The area from 59th Street to 125th Street and Central Park West to Riverside Park is considered by many to be the quintessential Manhattan neighbuorhood. Parks, theatres, historic buildings, world famous museums, fine restaurants and prestigious Uuniversities call the area home. Naturally, so does an eclectic mix of New Yorkers, ranging from stroller-pushing house moms and sharp-dressed executives to bespeckled intellectuals and paint-splattered artists. Economically, these upwardly mobile residents range from the professional to the prolific. Many are drawn to the area to be around like-minded New Yorkers who are, historically, politically and spiritually liberal—yet who harken to the sensibilities of suburbia. But all who inhabit this vast stretch of Manhattan would agree that the satisfying jumble of chic spots and local haunts, glamorous concert halls and humble community forums—the irresistible fusion of town and country—render the Upper West Side its own little Big Apple.

Residents aren’t the only ones clamoring for a bite of this locality. Big corporations have caught on to its appeal, too. AOL Time Warner, for example, has built its headquarters at Columbus Circle. Just a stone’s throw away is the impossible-to-overlook Trump International Hotel and Towers, home to the rich, famous and delicious (four-star restaurant Jean Georges is located in the lobby). Trump is also responsible for Riverside South, another condominium high rise at 70th Street and Riverside Drive, and the loft condominiums across from Lincoln Center at 43 West 64th Street, formerly the Liberty Warehouse, promise to attract even more people to the area. But flashy skyscrapers are nothing new to this part of town. When Central Park saw its final days of construction, the real estate to its west saw its beginning. Some of the more notable addresses are The Dakota at 72nd Street and San Remo Apartments at 74th Street, exclusive buildings that have seen their share of celebrity residents.

With generations of high profile tenants putting down roots on the Upper West Side, it’s no wonder rents and real estate values continue to soar. Still, it’s easy to justify when you consider the benefits of the vicinity: Lincoln Center, Central and Riverside Parks, the American Museum of Natural History, Columbia University, Zabar’s, Riverside Church, Sony’s I-Max Theater, Grant’s Tomb and of course, the newly expanded 72nd Street Subway Station. Best of all, within one wonderful section of town there exists a number of distinct communities, each boasting unique character and neighbourhood charm.

Downtown

Though visitors to New York often think Times Square captures Manhattan’s raw energy, people who actually live here know that Downtown is where it’s at! Many of the city’s best restaurants, lounges, dance clubs and clothing stores are located below 14th Street. Add to that a huge number of art galleries, city landmarks, cultural institutions and breathtaking vistas, and it’s easy to see why people scramble to live here. Not surprisingly, the area is expensive, and with the sprawl of gentrification now leaking over into the near reaches of Brooklyn, it’s safe to say everyone knows the value of a downtown zip code.

Still, this section of Manhattan remains ethnically diverse and socially tolerant, even if the gentrifying trend of Soho and Tribeca is slowly spreading to other neighborhoods. Parts of the Lower East Side, for example, continue to hum to the sounds of Latin music and Spanish conversation, but college kids, artists, musicians and numerous nightspots have turned this historically Puerto Rican neighborhood into prime real estate for those whose tastes and finances run between the East Village and Soho. Significantly less gentrified (but certainly not immune) is Chinatown, an awe-inspiring neighborhood rife with dim-sum restaurants, Asian produce and seafood markets, designer knock-offs and more Chinese immigrants than anywhere else outside of Asia. It’s truly phenomenal! Especially when you consider that Canal Street once stood as a boundary, of sorts, between Chinatown and the incredibly shrinking Little Italy. Nevertheless, these two extraordinarily different cultures live side by side, retaining (to some degree, in the case of Little Italy) their old-world essence and unique character.

Other neighborhoods below 14th Street possess a different kind of personality. Greenwich Village, popular in the 1960’s with visionaries such as Alan Ginsberg and Jack Kerouac, is less bohemian these days, now that students from nearby NYU have christened the area their personal cocktail lounge. Bar after bar line the leafy blocks along Bleecker Street, with plenty of restaurants, novelty shops and cramped cafes thrown in for good measure. Even so, there are countless reasons (Washington Square Park, Salmagundi Club, Jefferson Market Library, Babbo!) why buyers pay top dollar for the area’s quaint, townhouse apartments.

The crowds diminish as you move toward the Hudson or East Rivers, but unfortunately, property values don’t—particularly in the West Village. New buildings, like Richard Meier’s tower at 173-176 Perry Street, house a number of high profile personalities. Horatio House and The Greenwich are a couple of other luxury buildings to go up in recent months. Needless to say, this is one area of Manhattan where supply will probably never outpace demand.

Over to the east, cute cafes and college book stores give way to body-piercing palaces, tattoo parlors, second-hand clothing stores and all things punk rock. But don’t let the East Village fool you. Like every other neighborhood in Manhattan, its edges have been softened by the “A,B,C’s”: Artists, business and college students. What was once a playground for immigrants, poets, vagabonds, and musicians has become a hotbed of slacker sophistication, thanks to the large number of graduate students and young professionals who have taken over the area. And alphabet city, long-known for its large Spanish population and sketchy sidewalks, is looking more and more like the rest of the streets to the west of Tompkins Square Park.

Neighborhoods currently undergoing the “it” phenomenon include Nolita (hipster headquarters), Tribeca (cinemaphile central) and the Meatpacking District (style station), all of which are seeing their share of swanky boutiques, sceney lounges and restaurants of the chic variety. It’s hard to say which pockets below 14th Street will boom next—mainly because there’s nothing left to emerge—but New Yorkers and all who wish to be New Yorkers have a way of sussing out life in the most unexpected places.

Midtown

When people think of Midtown, most probably conjure images of Times Square’s bright lights, soaring buildings, famous venues, taxi-clogged streets and world-class hotels. But this section of Manhattan isn’t nearly that one-dimensional. Midtown covers a vast stretch of land, roughly from 14th to 59th Streets, between the Hudson and East Rivers. As anyone who has wandered these blocks knows, that covers a lot of personality.

No two neighborhoods within the Midtown bubble are alike. The area of Chelsea, known for its white-hot galleries, fierce nightlife and pre-war co-ops, is vastly different from Gramercy Park, with its manicured streets, refined restaurants and ornate townhouses. As to be expected, the residents in these areas are also quite different from one another, but in the end, they all complete one large picture of diversity. And that’s the key to understanding—and embracing—Midtown. An area that can boast varied landmarks such as Rockefeller Center, Grand Central Station, the Four Seasons, the Empire State Building, the Javits Center, Macy’s and Madison Square Garden among other sights, must appeal to myriad individuals. These residents have seen to it that their Midtown nooks generate some of the best theater (Broadway/Theater District), the latest fashion (Fashion District), the finest restaurants (Gramercy/Flat Iron) and the most notable hospital facilities in the world (Murray Hill/Kips Bay).

Beyond its cultural benefits, Midtown Manhattan has a logistical allure for many residents. Most neighborhoods are well serviced by subway and bus lines and, if they’re not, they’re usually traversed by a stream of yellow cabs. This means that Central Park and Uptown museums are just as accessible as Battery Park and Soho Shopping. But when you think about it, who really needs Uptown or Downtown, when all you could ever want is thriving within this wonderful stretch of real estate? - Douglas Elliman

Condo-Maximum - Prices Way Up for Manhattan Apts

The New York Post July 13, 2004

Manhattan - average sale prices:Nothing can slow down the soaring market for Manhattan apartments - not even the soaring interest rates.

Leading the way, by a large margin, is the condo market, which posted a remarkable 60 percent increase for East Side condos, with an average sale price of $1.4 million.

The average price for condos around the borough jumped 38 percent - and Manhattan co-ops went up 19 percent, according to a report released by the Corcoran Group real-estate firm.

Co-op studios around Manhattan jumped 20 percent to an average $277,000 and a typical condo studio will set you back $396,000. "Just to live in one room . . . will cost you just under $400,000," said Corcoran CEO.

"And that doesn't even mean you'll get a view out that one window."

People who could afford apartments with lots of bedrooms were in a "buying frenzy" the report said.

Condos with three or more bedrooms sold for an average of close to $3 million - a 32 percent hike from the first half of 2003.

Co-ops with three or more bedrooms went for an average of $2.5 million - an 8 percent increase.

Co-ops generally sell for less than condos because of the hassles of getting approved by persnickety boards and have to give up highly personal financial and other information.

Townhouses, once considered undesirable and expensive to maintain, are now practically worth their weight in gold.

"Buying a townhouse on the Upper East Side is going to cost an average $5.8 million." That's an increase of 23 percent over last year.

West Side townhouses posted a 17 percent gain in the last six months to $2.41 million.

Corcoran says the superheated market is being propelled by "record Wall Street earnings."

In another report, Jeffrey Jackson, the chief economist for appraisal firm Mitchell, Maxwell & Jackson, said, "At the current rate, within five years [no Manhattan apartment or condo] will go for under a half a million dollars."

According to MMJ, the increase in the 30-year fixed mortgage rate from 5.74 percent to 6.26 percent did nothing to affect sales.

The Corcoran report also showed that Brooklyn sales and prices continue to surge.

In the first half of 2004, the average price of all residences went up 16 percent. Sales of single-family homes were up 18 percent over the same period last year.

Sales were especially good in Fort Greene and Boerum Hill, where prices increased 30 percent from a year ago.

One of the fastest growing Brooklyn neighborhoods is DUMBO, where the average price of condos jumped a startling 42 percent to $1.1 million. - by Braden Kiel NEW YORK POST 13 July 2004

Real-estate prices remain high in first half of 2004:

- Condos $1.23 million Up 38%

- Co-ops $900,000 Up 19%

- East Side condos $1.406 million Up 60%

- West Side condos $1.282 million Up 42%

- East Side townhouses $5.8 million Up 23%

- West Side townhouses $2.41 million Up 17%

- Studio condos $396,000 Up 11%

- Studio co-ops $277,000 Up 20%

- Three-plus bedroom condos $3 million Up 32%

- Three-plus bedroom co-ops $2.5 million Up 8%

- Brooklyn - average sale prices

- Marketwide Up 16%

- Single-family homes $1.5 million Up 18%

- Boerum Hill and Fort Greene areas Up 30%

Source: Corcoran Group July 13, 2004

Sales of luxury residential properties continued to hold steady on the Upper East Side and Upper West Side after a slight decrease in 2002 prices. Fifty-one cooperative apartments were closed in the over $4 million range in the first half of 2002, in contrast to 44 in the first half of the peak market in 2000.

- New York Service Flats

- Development activity around Columbus Square NYC

- Manhattan Facts at a Glance

- New York's building boom slides after 9-11

- Trophy Towers like Empire State Building a liability in NYC

- Offshoring will affect Office market

- Impact at Ground Zero real estate

- Diane Sawyer at home in Robert Redford's digs

- Top 29 Families of New York

- The cooperative market has held its own in the $4 to $10 million range although there was a decrease in the average sale price in 2002.

- Cooperatives of over $10 million had the greatest price decrease -- some by 20% to 30% -- due to the absence of the global buyer. Nevertheless there was a resurgence in the $10 million-plus market with seven accepted offers in the last quarter of 2002 and into 2003.

- Townhouses were the strongest sector with total volume soaring 45% to $282,837,400. Thirteen townhouses were sold in the first quarter of 2002 in the $10 million range, three more than in 2001 and the market seems to be holding steady in 2003.

- The condominium market, similar to the cooperative market, has seen brisk sales in the under $10 million range, while the $10 million market languished until the last half of the year. At least eight condominiums in the $10 million to $18.5 million range were sold in 2002, six sales occurring in the last half of the year.

- Downtown townhouse sales and condominium resales lagged in 2002 with much competition from new projects but seem to be rebounding now. - Stribling 1 April 2003

325 Fifth Ave.

325 Fifth Ave. A $37.4-million bridge loan closed for 325 Fifth Ave., a 250-unit, 390,000-sf residential condominium project with an estimated development cost of $190 million.

Richard Bassuk, president of the Singer and Bassuk Organization, tells GlobeSt.com that the developers--a joint venture between Continental Properties, owned by the Fisch family, and Jeffrey Levine’s Douglaston Development--feel this project will “change the face of this Midtown area.” The site is between 32nd and 33rd streets. Work will begin shortly and the building is expected to be completed some time in early 2006.

“This should really stimulate development in this area,” says Bassuk, who has long-established relationships with both JV partners. In fact, he introduced them. He says the 40-story tower in the shadow of the Empire State Building is at the intersection of a number of Manhattan's prominent neighborhoods: Chelsea, Grammercy and and the Flatiron District. "It will really change the character of the neigborhood."

HSBC Bank provided the bridge loan to facilitate the acquisition and start of development. “The substantial interest shown by HSBC is testimony to the project and its owners," Bassuk points out. Levine says Bassuk was “instrumental in obtaining the bridge loan we required to acquire the property and related development rights on highly advantageous terms.” Steven Fisch says it took SBO's "special expertise in coordinating the financing of a project with its development and construction requirements.”

SBO has obtained a $130-million construction loan and a $42-million mezzanine loan for the project. The 325 Fifth Ave. bridge loan transaction is the latest bridge-loan financing arranged recently for SBO clients. Recent SBO bridge loans have totaled more than $250 million in seven transactions. - by Barbara Jarvie GLOBE ST 9 Sept 2004

OFFICE

Vacancy rate up for top Manhattan buildings

Manhattan's strongest and weakest office markets flipped direction in July, as the vacancy rate for top-quality Midtown buildings shot up while a similar rate Downtown fell, according a monthly report from Colliers ABR. The spike in Midtown's Class A vacancy rate - to 9.3 per cent from 8.8 per cent - was blamed on two large blocks of space totalling about 891,000 square feet coming onto the market in the Grand Central area.

Those two spaces seeking tenants brought the vacancy rate for Class A buildings - those that are new or renovated with up-to-date amenities - in the Grand Central area to 11.8 per cent, the highest rate since December 2003 and up from 9.2 per cent in June.

Average asking rents for Midtown Class A buildings dropped for the second month in a row, to US$60.26 per square foot from US$60.57 per square foot in June.

'I honestly don't think this is very serious for a couple of reasons,' Robert Sammons, director of research, told Reuters. 'Citigroup is very close to inking a deal at 485 Lexington, which will help decrease this number.

'It certainly will be going up the next few months,' he said. 'This is typically a time when many brokers are on vacation. Not a lot of wheeling and dealing gets done in the summertime in New York.'

Meanwhile, the vacancy rate for Downtown Class A buildings fell to 11.3 per cent in July from 12 per cent in June. However, that trend may not last, as the 1.7 million square feet of space at the newly constructed 7 World Trade Center comes on the market at the end of the year.

Rents for Downtown Class A buildings rose to US$33.97 in July from US$33.92 in June. - Reuters 11 August 2005

$355M Price Tag for 180 Maiden Lane

Investor Joseph Moinian made a big move into Class-A office land with an approximately $355 million purchase of 180 Maiden Lane, also known as Continental Center.

The somewhat octagonal, 1.09 million-square-foot building, located on the East River waterfront, is nearly fully leased to Goldman Sachs and the law firm Stroock, Stroock & Lavan.

Real Estate Finance & Investment reported that the German-funded Paramount Group is selling the building to a Moinian-led investor group for about $323 a foot.

Paramount bought it from CNA Financial for $290 million, or $263 a foot, in early 2001.

Wayne Maggin of Eastdil is marketing the property, but neither he nor Moinian returned calls for comment.

Moinian developed the residential Marc, at 800 Eighth Ave. This year alone he (with partners) has bought 530 Fifth Ave. and 1450 Broadway; he is in contract for 95 Wall St.

He is also part of the New York investor group that purchased the Sears Tower in Chicago. - by Lois Weiss NEW YORK POST 9 July 2004

Donald Trump and his Japanese investors sold the Empire State Building to master leaseholder Peter Malkin for $57.5 million

Max Capital Management Corp. acquired a five million square foot class A office portfolio from Credit Suisse First Boston, including two Manhattan office towers as well major properties in Chicago and Detroit for $777 million. The New York additions to Max Capital’s 7 million square foot holdings include 350 Madison Ave. and 1440 Broadway, both of which the firm currently owns in partnership with CSFB. Other trophy properties in the portfolio include One North LaSalle in Chicago, a 49-story landmark office tower, and 150 W. Jefferson in Detroit, a 25-story, glass-and- steel office tower.

1515 Broadway sale - first significant sale since 9-11 to Canada's Caisse Depot

The 40 storey office tower at 450 Lexington Ave., sold to Beverly Hills oil baron Marvin Davis, according to published reports in November 2001. Owned by Royal Dutch/Shell Group's Pension Fund, Eastdil Realty is arranging what is said to be a sale in the neighborhood of $325 million for the building, which is located at Lexington Avenue and 45th Street, immediately north of Grand Central Station's Graybar building. The facility has 900,000 square foot of office space sitting atop a United States Postal Service Office facility.

Lehman Brothers Holdings Inc. purchased the one million square foot tower that Morgan Stanley has been building in New York City at Broadway and 49th Street. Located a stone's throw from Morgan Stanley's 1.4 million square foot Times Square headquarters at 1585 Broadway, the new building, 745 Seventh Ave., has been under construction since 1999 and is scheduled for occupancy later this year. The firm recently leased Manhattan office space on Third Avenue and Morgan Stanley states it will continue to accumulate additional space at 750 Seventh Ave., 1633 Broadway, Pierrepont Plaza in Brooklyn and in retail branches throughout the city.

The class B office building at 469 7th Ave fetched $222 per sf for the seller, a JV of SL Green and MSREF when it sold for $53 million. The deal was considered an indicator of renewed interest in bread-and-butter assets with solid long-term potential.

The New York office market was hugely affected by the events of WTC on 11 September 2001. The total immediate loss is roughly 15 million sq. ft. of property in lower Manhattan (approximately 12.7 million square feet was destroyed and another 2.3million square feet has been damaged or declared structurally unsound as a result of fires, falling debris and building collapses. More than 10.7 million sq. ft. of property sustained damage (5 million sq. ft. that will be taken out of the market for at least one year to complete extensive repairs and reconstruction and 5.7 million square feet that should be ready for occupancy in less than 12 months)

Rockefeller Centre sold to Chicago billionaire Lester Crown family with NY's Speyer for $1.85 billion for the 22-acre complex comprising 12 historic Rockefeller Center buildings. Vacancy in the complex was just 1%.

One of the office towers of Rockefeller Centre in midtown Manhattan at 1211 Avenue of the Americas was acquired by a German group for $561 million. The 45 storey Class A office building comprising 1.9 million square foot was built in 1973 by the Rockefeller group. The vacancy for Class A office space in the area known commonly as the Plaza District was 1.84 per cent, down from 4.16 percent at the same time last year. The purchaser already owns 620 Avenue of the Americas and 1475 Broadway.

German real estate developer RFR acquired the 38th storey Seagram Building at 52nd Street and Park Avenue from Teachers Insurance and Annuity for $375 million for the 42 year old property.

Houston based Hines acquired the 36 storey, 592,000 sq ft office tower at 750 Seventh Avenue in partnership with General Motors Asset Management. The building completed in 1990 is 100% tenanted and anchored by Morgan Stanley Dean Whitter who occupy approximately 60 per cent of the building.

Bids were accepted for the 1.47 million sq ft, 42 storey building on the western side of Sixth Avenue between West 51st and 52nd Street. Paine Webber Group occupies approximately one-third of the property where rents average ~ $65 per sq ft.

AT&T Corp sold its Manhattan based headquarter building to members of prominent New York real estate family for ~ $150 million. Plans for the 85 year old property at 32 Avenue of the Americas, include technological upgrades, as well as traditional renovation. While AT&T plan to maintain a significant presence in the building, an AT&T spokesman said the company no longer wanted to be in the real estate business.

Vornado Trust who owns the former Alexander's site between 58th and 59th streets and Third and Lexington avenues has plans for a redevelopment which includes stores on the first two floors, office on three floors, 20 floors of hotel suites and 47 floors of luxury condo. Vornado who have owned the site for 20 years have been in talks with Bloomberg, the financial services company, about a deal for the office space and has signed Swedish retailer H&M as tenant. Apparently number of tenants are rumored to have signed.

Reckson Associates Realty purchased the 35 storey, 540,000 square feet Class A office tower in Manhattan at 1350 Avenue of the Americas for $126 million. The property, 1350 Avenue of the Americas, is located midtown, at the corner of 55th Street in the Sixth Avenue/Rockefeller Centre sub market. This is Reckson's second acquisition in New York City since its May merger with Tower Realty Trust. The group now has more than 3.5 million square feet of Class-A office space in the city. Reckson also purchased 919 Third Avenue.

The Government of Singapore Investment Corp. backed out of a preliminary agreement to buy 1211 Sixth Avenue for about $570 million from Heitman Financial earlier in 2001. The seller is in discussion with finalists in the bidding to buy the 1.9 million square foot trophy tower between West 47th And West 48th Streets. GSIC emerged from a pack of a dozen bidders tot make the preliminary agreement for $300 per square foot.

Chinese firm eyes big site for NY center

One of China's largest real estate companies is seeking up to 1 million square feet of office space in Manhattan to create a center for Chinese companies establishing operations in the United States.

Beijing Ventone Real Estate gave formal approval earlier this month to seek suitable office space in the city, according to New York businesspeople who have been working with the company. It would lease the space, and then sublease offices to Chinese companies that want a headquarters in the West. Ventone would provide those companies with support services such as conference facilities and translators.

Ventone is considering both midtown and downtown for the new venture, but city leaders are pushing hard for a downtown location.

"We are hopeful that they'll go to 7 World Trade Center," says Kathryn Wylde, president of the Partnership for New York City. A meager 20,000 square feet of the 1.7 million-square-foot World Trade Center tower is leased, not including an office for the developer and World Trade Center leaseholder, Larry Silverstein.

City officials agree that a downtown location is best. The plan "dovetails nicely with what we are trying to accomplish downtown," says Josh Sirefman, assistant to Deputy Mayor Daniel Doctoroff. "Ventone's preference is for lower Manhattan, from what I understand." A number of Chinese companies were located at the original World Trade Center.