天然氣庫存3月底預期將降低10%。但顯著高於平均數。

美國天然氣價今天$1.8, 歐洲 $5, 亞洲 $ 9.

利潤的反差將驅使美國天然氣生產商積極謀求出口。

美國現在積極 尋求天然氣出口, 許多出口項目正在申請, 在建 和待建, 一周多前剛 批準一個:

The U.S. Energy Department has approved projects that may send abroad as much as 283 million cubic meters per day of U.S. gas, and it is considering applications for another an additional amount.

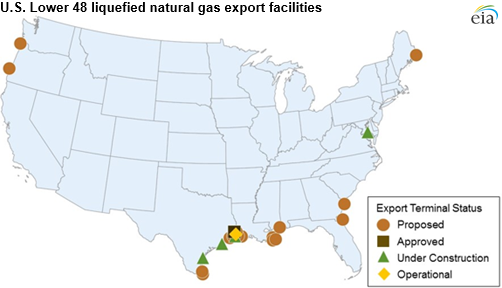

Growth in domestic natural gas production leads to development of LNG export terminals

The first export shipment of liquefied natural gas (LNG) produced in the Lower 48 states on February 24 is a milestone reflecting a decade of natural gas production growth that has put the United States in a new position in worldwide energy trade.

With the rapid growth of supply from shale gas resources over the past decade, U.S. natural gas production has grown each year since 2006. The resulting decline in domestic natural gas prices has led to rising natural gas exports, both via pipeline to Mexico and, since last week, to overseas markets via LNG tankers.

The United States is currently a net importer of natural gas, and gross imports represented nearly 10% of total supply in 2015, based on data through November. The United States imported 7.5 billion cubic feet per day (Bcf/d) of natural gas, mostly from Canada by pipeline, and exported 4.8 Bcf/d, mostly to Mexico by pipeline. For years, Alaska has exported LNG, mostly to Pacific Rim countries, but these volumes have been small. In addition to the Sabine Pass terminal that was the source of last week's LNG shipment, four other LNG export terminals are currently under construction.

When natural gas is cooled to -260 degrees Fahrenheit, it becomes a liquid that is 1/600th of its gaseous volume, making it easier to transport via vessel. The U.S. Gulf Coast has a large existing pipeline network, which makes the area attractive for developing export terminals. Many of the LNG export terminals now under construction or proposed are at sites that have functioned, and may continue to function, as LNG import terminals. Several LNG import terminals were built in the 1970s, and a new wave of terminals was constructed in the mid- to late-2000s. As domestic production increased, LNG imports declined, as many new terminals were barely used and the utilization rates of older terminals declined.

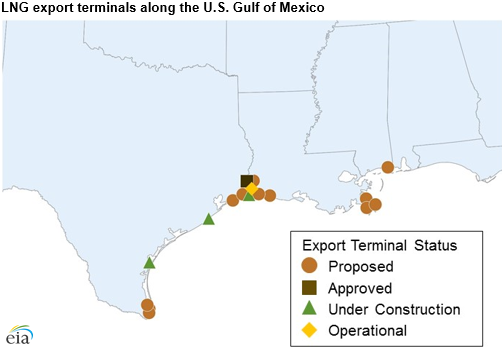

The Federal Energy Regulatory Commission (FERC) is responsible for authorizing siting and construction of LNG export terminals (as well as import terminals) that are onshore or that are close to the shore. FERC prepares environmental impact statements to assess the environmental consequences of the terminals under its jurisdiction. Although most of the LNG terminals fall under FERC jurisdiction, the U.S. Maritime Administration regulates deepwater terminals. Only one deepwater export terminal has been proposed, and if approved, it would be located about 50 miles south of the Texas-Louisiana border in the Gulf of Mexico. In addition to approval for construction from FERC or the Maritime Administration, the U.S. Department of Energy's Office of Fossil Energy issues separate authorizations to export to countries based on whether they have a free trade agreement with the United States.

Cheniere Energy's Sabine Pass Liquefaction Project in Sabine Pass, Louisiana, consists of six different liquefaction units, or trains, the first of which began service in February after many delays. The other trains are in various stages of development and permitting. Total permitted capacity by FERC is 4.16 Bcf/d.

Four LNG export terminals are currently under construction:

- Dominion Energy's Cove Point LNG facility in Cove Point, Maryland, is scheduled to bring one train totaling 0.82 Bcf/d online near the end of 2017.

- Corpus Christi LNG, another Cheniere project, is under construction in Corpus Christi, Texas. The terminal is scheduled to begin service in 2018, with total permitted capacity at 2.14 Bcf/d.

- Sempra Energy's Cameron LNG terminal, located in Hackberry, Louisiana, is under construction and is scheduled to bring three trains online in 2018. A total of 1.7 Bcf/d has been permitted.

- Freeport LNG's terminal planned for Freeport, Texas, has three trains under construction totaling 1.8 Bcf/d. The first two are scheduled to begin service in 2019, and the third in 2020.

Another terminal, Southern Union's Lake Charles (Louisiana) LNG facility, has been approved by FERC but is not yet under construction. Lake Charles also has an LNG import terminal. Several more LNG export terminals, mostly on the Gulf Coast, have been proposed or have pending applications with FERC.

The new terminals are expected to take advantage of natural gas produced in the Appalachian Basin, particularly the Marcellus and Utica regions, the source of much of the nation's production growth over the past several years. The Sabine Pass Liquefaction project has secured 300 million cubic feet per day (MMcf/d) of natural gas from the Texas Gas Transmission Ohio-Louisiana Access Project, which facilitates additional flows of Marcellus and Utica natural gas to the southern United States. Additionally, Cheniere's Corpus Christi Liquefaction project will receive 385 MMcf/d from the Natural Gas Pipeline Company of America's Gulf Coast mainline pipeline system. Dominion's Cove Point (which began operating as an import terminal in 1978) already has a dedicated pipeline with a link to three interstate pipelines that operate in the Marcellus area.

Market conditions have changed since many LNG export projects in the United States were initially proposed. Proposed LNG terminals in the United States face not only increased competition from other domestic and foreign terminals that have been completed, but they also face uncertainty in global LNG demand. Australia, already a major LNG exporter, plans to expand its LNG export capacity in the coming years. In late 2015, two terminals began service in Australia, Gladstone LNG and Australia Pacific LNG, both located on Australia's East Coast. At the same time, LNG imports by countries in Asia declined slightly in 2015.

Natural Gas

Temperatures were warmer than normal in February, which contributed to Henry Hub spot prices declining throughout the month and averaging $1.99/MMBtu. As a result of warmer-than-expected weather, this month's STEO revises upward forecast end-of-March 2016 working inventories to 2,288 Bcf, compared with 2,096 Bcf in last month's forecast.

Natural Gas Consumption

EIA's forecast of U.S. total natural gas consumption averages 76.8 billion cubic feet per day (Bcf/d) in 2016 and 77.3 Bcf/d in 2017, compared with 75.3 Bcf/d in 2015. Total consumption for 2016 in this month's STEO was revised upward by 0.5%, driven by increasing expectations of natural gas use in the electric power sector. Forecast electric power sector use of natural gas increases by 3.0% in 2016, then declines by 1.7% in 2017, as natural gas prices rise. Forecast industrial sector consumption of natural gas increases by 2.9% in 2016 and by 2.2% in 2017, as new projects in the fertilizer and chemicals sectors come online.

Natural Gas Inventories

On February 26, natural gas working inventories were 2,536 Bcf. After withdrawals accelerated in January, they slowed again in February because of warmer-than-normal weather. February 26 inventories were 794 Bcf (46%) above year-ago levels and 666 Bcf (36%) above the five-year average for that week. Inventories are forecast to be 2,288 Bcf at the end of March 2016, an increase of 192 Bcf from last month's STEO, and 666 Bcf above the five-year average for the end of March.

Natural Gas Prices

The Henry Hub natural gas spot price averaged $1.99/MMBtu in February, a decline of 29 cents/MMBtu from the January price. The February price decrease reverses gains in the Henry Hub price in January. Warmer-than-normal temperatures through most of the winter, record inventory levels, and production growth have contributed to sustained low natural gas prices. Monthly average Henry Hub spot prices are forecast to rise slowly beginning in May 2016, but they remain lower than $3/MMBtu through December. Forecast Henry Hub natural gas prices average $2.25/MMBtu in 2016 and $3.02/MMBtu in 2017.

Natural gas futures contracts for June 2016 delivery traded during the five-day period ending March 3 averaged $1.91/MMBtu. Current options and futures prices imply that market participants place the lower and upper bounds for the 95% confidence interval for June 2016 contracts at $1.27/MMBtu and $2.88/MMBtu, respectively. In March 2015, the natural gas futures contract for June 2015 delivery averaged $2.83/MMBtu, and the corresponding lower and upper limits of the 95% confidence interval were $1.92/MMBtu and $4.18/MMBtu.