回 “能不能展開說說最近4-weeks T-Bill 利率下滑,釋放了什麽信號?” JPMorgan 今天的

top market takeaways 是這樣寫的:

We see three scenarios on how this could play out. We think the first is the most likely:

(1) The debt ceiling is increased ahead of the potential default date.

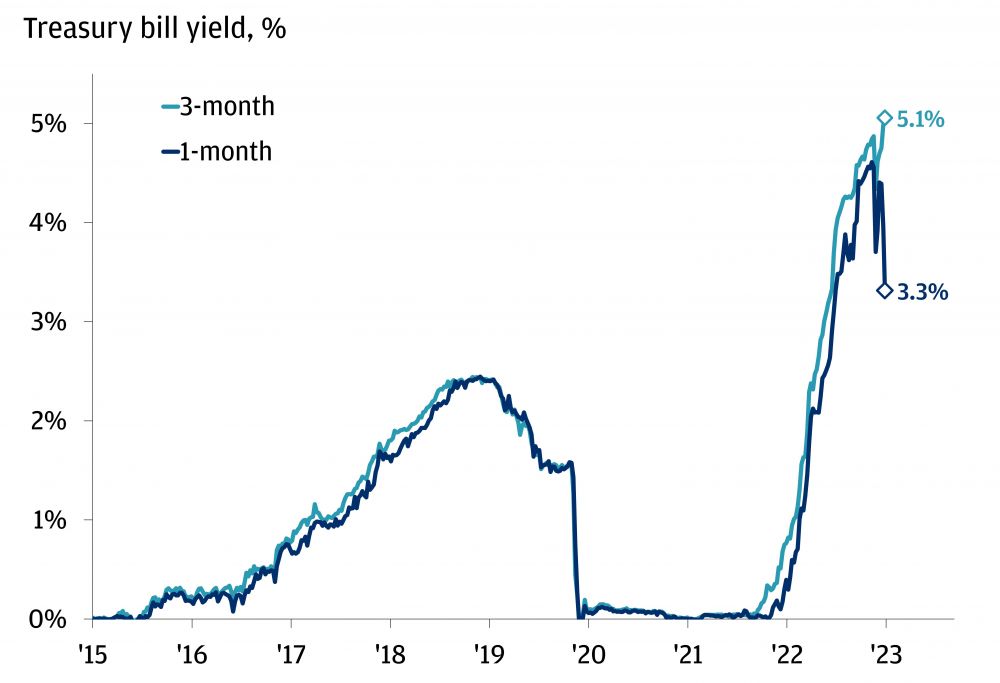

In every instance in history, this has been the eventual outcome, and we expect this year to be no different. As Congress works out a compromise, we’re likely to see investors avoid Treasury bills that mature in the wake of the X-date. This has already started to play out as 3-month Treasury bill yields spike and 1-month bill yields plummet to their lowest level since last October. In fact, the dispersion between the two is the widest in over 20 years. We expect these oddities to continue as policymakers work out the kinks to reassure investors of the soundness of short-term government debt.

The risk of a U.S. default pushed T-bill yields in different directions

(2) We go through the X-date without a ceiling increase, but the Treasury still makes interest payments to avoid a technical default.

In our view, to avoid default, the government would prioritize security payments at the expense of cuts to discretionary, or even mandatory, spending. The consequence of this would likely be a direct hit to economic activity and financial market sentiment. Other ways to avoid default would be to simply ignore the debt limit on grounds that it violates the 14th amendment (which would cause serious legal trouble), or the Treasury could mint a coin and deposit it to the Fed – the latter being, to us, highly far-fetched.

(3) We go through the X-date and delay payments (i.e. default).

This would be the worst case and least likely scenario. It’s hard to say what the full consequences would be, but it’s likely the harsh reaction across financial assets would warrant movement from Congress. But even if the debt limit is subsequently raised, the question remains on whether Treasuries would need to trade with a permanently increased risk premium (i.e. investors would demand to be compensated more for taking on greater risk). The “risk-free” rate would be a term of the past.

WENXUECITY.COM does not represent or guarantee the truthfulness, accuracy, or reliability of any of communications posted by other users.

Copyright ©1998-2025 wenxuecity.com All rights reserved. Privacy Statement & Terms of Use & User Privacy Protection Policy