With the Trump administration's recent hints, a public offering of shares in mortgage guarantors Fannie Mae (OTCQB:FNMA) and Freddie Mac (OTCQB:FMCC) could occur this year, a resolution to the question we've had since last year appears imminent--which is better to own, common stock or various issues of junior preferreds?

The answer mainly depends on two factors--the offering price of the common, and the details of how the preferreds are handled. There are scenarios that favor the common, favor the preferreds, or are good for certain preferreds but bad for others.

For simplicity's sake, this article will focus only on Fannie, the larger and more heavily traded of the two government-sponsored enterprises that have been in conservatorship since 2008. A similar analysis could be made for Freddy.

Let's look at four of the main scenarios:

1) Government's Senior Preferred Stock Purchase Agreements (SPSPAs) are deemed repaid. Junior preferred holders receive a rights offering allowing them to convert to common shares at par.

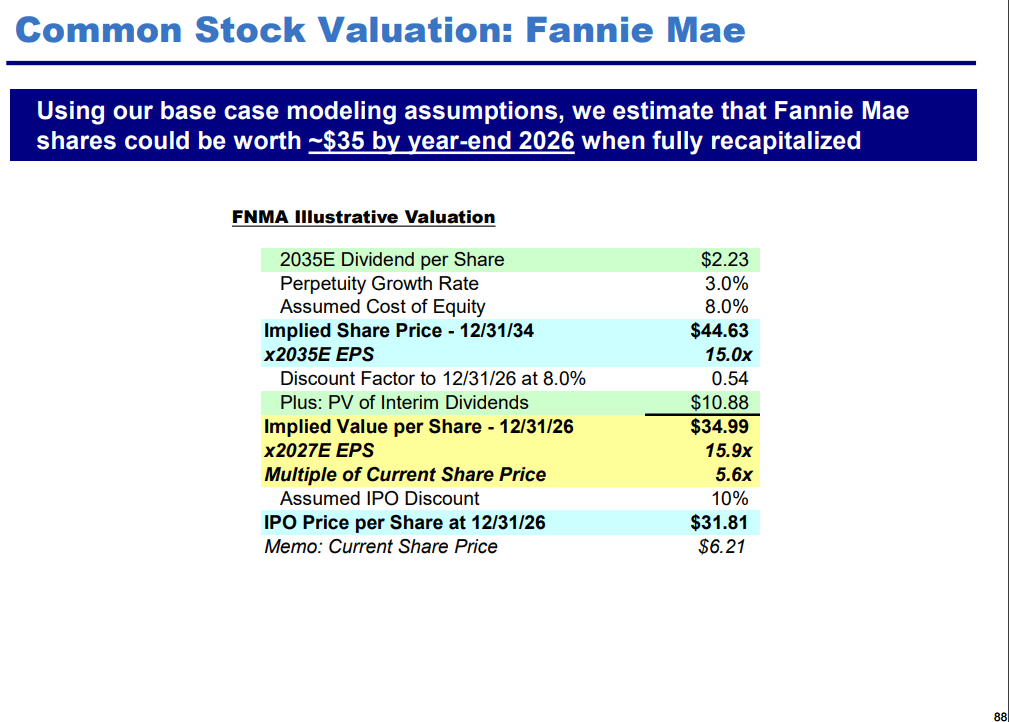

Cancellation of the SPSPAs is the scenario envisioned by hedge fund manager Bill Ackman's Pershing Square Capital Management in their presentation valuing FNMA at $35 by the end of 2026, with an IPO price of $31.81 at that time.

FNMA illustrative valuation (Pershing Square Capital Management)

Common shareholders, including Ackman, argue that the government has been more than repaid with 10% interest for the $121 billion in loans it provided Fannie. If the Trump administration agrees, shareholders could see a double or better from the recent price.

For preferred holders, a rights offering allowing them to convert to common could mean they would get face value in the form of common shares, subject to a cap on the amounts that could be converted.

This is good for the $19 billion in legacy preferreds issued before 2008, especially the ones that are selling at a lower percentage of face value, such as FNMAH, which recently sold at 48% of face.

The high-coupon, liquid preferred issues FNMAS and FNMAT would rise less, since they are already at about 65-67% of face.

To help investors shop for the best buys, this Google spreadsheet lists the preferreds in order of lowest percentage of face value.

Here is a simplified chart of the projected returns with IPO prices of $10 (the B. Riley price target), $20 (the Deutsche Bank price target), and $30 (close to the Pershing Square valuation).

Source: Author's spreadsheet

As you can see, preferreds would be in line for big gains no matter what the offering price for FNMA. The common provides more bounce if the IPO is at $30 or more but falls if it is at $10.

A variant of this scenario would occur if the preferreds were subject to mandatory conversion to common. This would produce similar results, but could be subject to legal challenges that would delay the offering.

2) SPSPs are left intact. Junior preferred holders get conversion rights.

Let's call this the Clint Eastwood scenario, since the senior preferreds would be unforgiven. This is about the same as Scenario 1 for junior preferred holders but much less beneficial for common holders, since they would suffer significantly more dilution from eventual conversion of the SPSPs to common stock in addition to the dilution they already expect from conversion of the government's 79.9% stake in warrants. This scenario is closest to the opinions on Seeking Alpha by Glen Bradford and Noah's Arc Capital Management.

All series of preferreds would likely significantly outperform the common.

I agree with B. Riley's analysis that this scenario is less likely.

Riley identifies two potential paths forward: the government could either maximize its senior position held by the U.S. Treasury and require recapitalization, which would be highly dilutive to current equity holders, or forgive the Treasury’s $121 billion senior preferred position.

The firm interprets recent comments by Treasury Secretary Bessent as aligning with the second scenario, which would minimize up-front dilution and maximize government sale of FNMA shares to investors."

Let's move on to Scenarios 3 and 4, which refer only to the junior preferreds and could be done with either treatment of the SPSPAs.

3) The offering document for common shares indicates dividends will be reinstated immediately for junior preferreds.

Turning the dividends back on after 17 years would scramble the valuation of the junior preferreds. With high coupons, FNMAS (with a dividend at face of 8.5%) and FNMAT (8.25%) likely would shoot up to par by the time of dividend reinstatement and probably a little higher, capped by the fact they are subject to being called at $25 at any time.

Low-paying issues like FNMAP (coupon rate 3.41%) would rise much less since their dividend rate would be well below market for junior preferreds, although it might still rise a bit since the yield at the recent price (7.2%) would be attractive.

I don't see this as too likely, as the government probably would prefer building capital to having to pay out cash immediately to pay high dividends or call FNMAS and FNMAT, which have $9 billion of face value, about half of all of the preferreds.

4) Offering includes no action on junior preferred, which are left in limbo.

This is the worst scenario for the preferreds--dividends might not be reinstated until they legally would have to be so the common dividend could also be reinstated. That could take a few years as the enterprise continues to build capital to meet reserve requirements.

Non-paying, non-cumulative preferreds tend to sell at a significant discount to par until payments are reinstated.

Eventually, what would probably happen is that the high-rate preferreds would be called as soon as dividends were turned back on because Fannie wouldn't want to pay above-market rates, while lower-rate ones would be left to trudge on with prices below face value, disappointing shareholders.

Thus, while the high-rate ones like FNMAS and FNMAT would be the better place to be, none of the preferreds would rise much immediately, and some, like the aforementioned FNMAP might fall significantly.

Risk Factors

A major risk is that for some reason, including lawsuits, the public offering does not occur in a timely manner. One possible source of delay is a merger of two GSEs as suggested by President Trump.

Regulations mandating high capital reserves could prevent the payment of dividends for several years, reducing investor interest in buying both the common and preferreds.

As discussed, the risk of the government's retention of its SPSP rights applies mainly to the common.

Conclusion

My guess is Scenario 1 is most likely based on the Trump administration's desire to drum up enthusiasm for the offering, but wanting to be positioned for any of them.

I hold FNMA common, a high-coupon preferred (OTCQB:FNMAT), and two medium-coupon preferreds (FNMAH and FNMFN). This diversifies risk and opportunity among the various scenarios. I am staying away from low-coupon preferreds like FNMAP because of the risk of Scenarios 3 and 4.

Taken as a whole, I expect the group to do well in any of these cases as long as the offering takes place before the midterm elections in November 2026. Once a registration statement is filed with the Securities and Exchange Commission, I will probably adjust my positions to reflect more certain knowledge.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.